Joint Accounts and Liability: What Most Couples Don't Know

Managing a joint account may seem simple, but it comes with risks that many couples overlook. Here’s what you need to know:

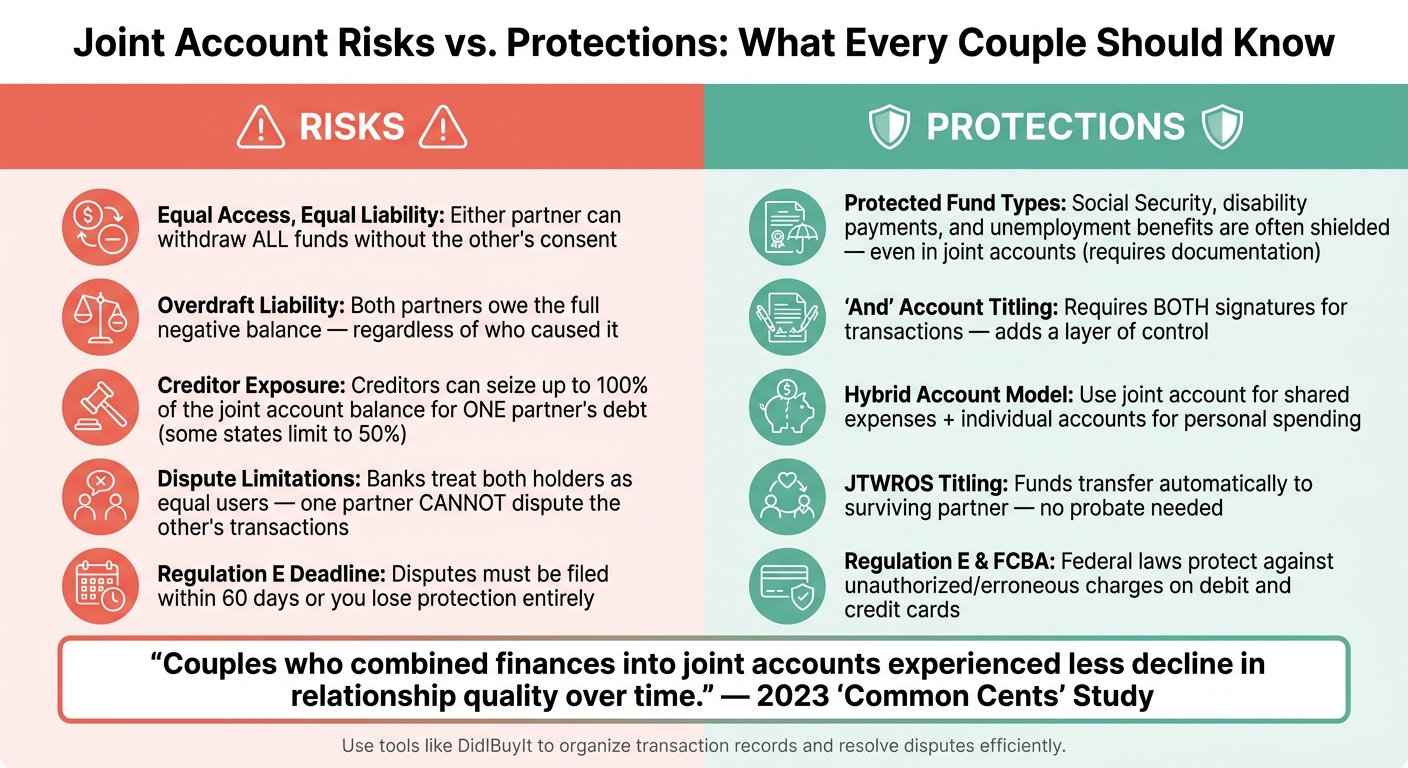

- Equal Access, Equal Liability: Both account holders can access all funds and are equally responsible for overdrafts, fees, or negative balances - regardless of who caused them.

- Exposure to Debt: Creditors can seize money from a joint account to cover one partner’s debts, even if the other partner contributed all the funds.

- Disputes and Protections: Disputing transactions is tricky because banks treat both account holders as equals. U.S. banking rules provide limited protection, and strict deadlines apply for filing disputes.

- Practical Solutions: Use a mix of joint and individual accounts, set clear financial rules, and keep detailed records. Tools like DidIBuyIt can simplify resolving disputes by organizing transaction data.

Joint accounts can streamline finances, but they require clear communication and planning to avoid financial stress. Understand the risks, set boundaries, and use tools to protect your shared money.

Joint Account Risks vs. Protections: What Every Couple Should Know

Hidden Risks of Joint Accounts

How Joint Ownership Actually Works

When you open a joint account, most banks treat all account holders as equal co-owners. This means that in a standard "or" account, either person can withdraw all the money, transfer funds, or even close the account without needing the other person's approval or even informing them [1]. It doesn’t matter who contributed what - both parties have full access to the account. This setup can easily lead to financial disagreements, especially if one person feels their contributions are being misused. On top of that, both account holders share financial responsibilities equally.

Shared Liability for Overdrafts and Fees

If one account holder overspends and the account goes into the red, both individuals are on the hook for the negative balance - not just the person who caused it.

"If your joint checking account goes into overdraft, you are liable for a negative balance." - Investopedia [1]

The bank has the right to demand repayment from either account holder, regardless of who overdrew the funds. This shared liability doesn’t just mean covering the immediate loss; repeated overdrafts can lead to consequences like being reported to ChexSystems. Such reports can make it harder for either party to open new bank accounts in the future.

Exposure to Each Partner's Creditors

Joint accounts also expose both parties to each other's financial obligations. If one account holder has unpaid debts - like taxes, court judgments, or child support - creditors can garnish the funds in the shared account, even if the other partner contributed all the money [3].

"A creditor can take money from your joint savings or checking account even if you don't owe the debt." - Stephanie Lane, Attorney [3]

Creditors don’t need to determine who deposited what. Depending on state laws, they may be able to seize up to 100% of the account balance to cover one partner’s debt. In some states, garnishment limits this to 50%, but the risk remains significant.

One way to partially shield yourself is by understanding protections for certain types of funds. For example, Social Security benefits, disability payments, and unemployment benefits are often protected - even in a joint account. However, you’ll need clear documentation, such as paystubs or deposit records, to prove the source of these funds. Keeping detailed records can help safeguard your money when disputes arise or creditors come calling. Being aware of these risks is essential for couples looking to protect their shared finances.

sbb-itb-5d40823

Managing Payment Disputes on Joint Accounts

Disputed Transactions and U.S. Banking Rules

When dealing with unauthorized or erroneous transactions on a joint account, U.S. banking laws - specifically Regulation E for debit cards and the Fair Credit Billing Act (FCBA) for credit cards - provide some protection. However, these protections come with strict time limits. For instance, Regulation E requires disputes to be filed within 60 days. Missing this deadline can leave you on the hook for the entire loss. These time-sensitive rules underscore the risks that come with sharing a joint account.

Banks view both account holders as equal users, meaning one person cannot dispute a transaction solely because it was made by the other.

"The frugal spouse cannot challenge the withdrawals or transactions of the other spouse with the bank because they are listed as a joint account holder." - Investopedia [1]

This equal treatment by banks creates complications, particularly when compared to how disputes with merchants are typically handled.

Chargebacks and Merchant Disputes

When a merchant error occurs - such as an incorrect charge, a damaged product, or a failure to deliver - chargebacks provide a way to address the issue. If you are filing a chargeback, having a clear strategy is essential to winning the case. Either account holder can initiate a chargeback through their bank, as payment networks like Visa, Mastercard, and Amex allow this process.

However, if one partner makes a purchase without the other's consent and the transaction later turns out to be fraudulent, both account holders are held accountable. To strengthen a chargeback claim, it’s critical to have detailed documentation, such as receipts, emails, or shipping confirmations. Without clear records of who made the purchase and when, proving your case can become an uphill battle.

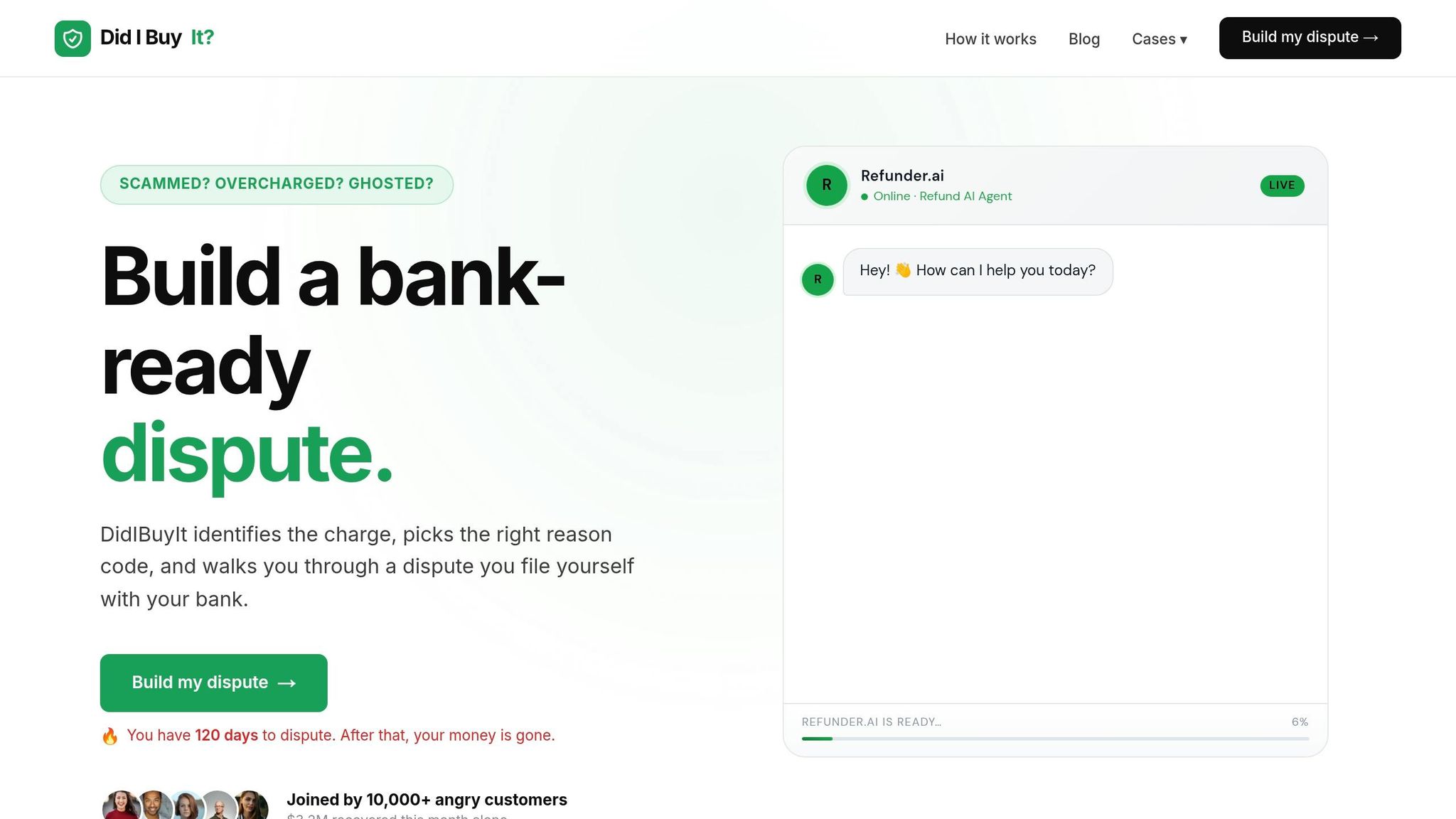

Using DidIBuyIt to Resolve Disputes

For couples managing joint accounts, staying organized is key - especially since banks won’t step in to resolve disagreements between account holders. That’s where DidIBuyIt comes in.

This AI-powered platform is designed to streamline dispute resolution for joint accounts. By analyzing disputed transactions, it quickly identifies key details and eliminates much of the confusion that shared accounts can create. The platform also generates the necessary bank-ready documentation for claims, making the process smoother. Plus, real-time updates keep both account holders informed, reducing potential conflicts.

For couples, having a tool like DidIBuyIt ensures disputes are handled efficiently and provides a clear record of transactions, helping to close the gaps left by U.S. banking regulations.

Practical Steps to Protect Joint Finances

Choosing the Right Account Setup

One effective way to manage financial risk is by diversifying your funds. A hybrid model - using a joint account for shared expenses like rent, utilities, and groceries, alongside individual accounts for personal spending - can strike a balance between transparency and independence.

Pay attention to account titling: an "And" account requires both parties' signatures for transactions, offering added protection, while an "Or" account allows either partner to act independently, which carries more risk. Once your accounts are set up, it’s crucial to establish clear financial rules to ensure smooth management.

Setting Clear Financial Rules

Many couples overlook the importance of putting financial agreements in writing. Start by deciding how shared expenses will be divided. A percentage-based approach often works well - for example, if one partner earns 60% of the household income, they can contribute 60% of shared costs [5].

Set a spending limit for significant purchases that require joint approval. Regularly review account activity, and enable mobile alerts for large transactions or low balances. These steps can help catch errors and keep spending aligned [7][8].

"A joint bank account is associated with greater financial goal alignment. It promotes a more communal view of your marriage." - Jenny Olson, Ph.D., Assistant Professor of Marketing, Indiana University [6]

This kind of structure lays the groundwork for managing joint finances securely and collaboratively.

Planning for Major Life Changes

The way your account is legally titled becomes especially important during life’s unexpected events. With Joint Tenants with Rights of Survivorship (JTWROS), funds automatically transfer to the surviving partner without probate - an option often suitable for married couples. On the other hand, Tenants in Common (TIC) allows each partner to assign their share to a different beneficiary, which can work well for blended families or specific estate plans [4][1].

In cases of separation or divorce, remember that either partner can typically close a joint account, but removing one party often requires mutual consent [2][4]. Consulting a financial advisor or attorney before a major life event occurs can provide better options and greater control over your financial future.

Should Couples Share Bank Accounts? - Joint Accounts Explained

Conclusion: Making Joint Accounts Work for You

Joint accounts simplify financial management but come with shared control and responsibility. Each account holder has full access to the funds, is equally liable for overdrafts and fees, and the account balance may be used to settle individual debts. Without a clear understanding of these dynamics, couples can face unexpected challenges that affect their daily lives.

However, understanding these risks can make a big difference. According to a 2023 study titled "Common Cents", couples who combined their finances into joint accounts experienced less of the typical decline in relationship quality over time [6]. The key? Both partners need to be intentional about how the account is used and agree on its purpose.

Dispute resolution is another critical factor in managing a joint account with fintech. Whether it’s an unauthorized charge or a disagreement with a merchant, having a clear record of transactions is essential. In these cases, tools like DidIBuyIt can be game-changers. Its AI-powered dispute analysis and ability to generate bank-ready documents simplify the process, reducing frustration and helping couples resolve payment disputes efficiently.

Ultimately, the success of a joint account depends on strong communication. Make sure both partners understand their responsibilities, agree on clear rules, and use reliable tools when problems arise. With open dialogue and defined financial boundaries, a joint account can serve as a valuable tool rather than a source of stress.

FAQs

Can my partner’s creditors take money from our joint account?

Yes, creditors targeting your partner may have the ability to garnish funds from your joint account. Whether this happens depends on several factors, including state laws, whether the account is classified as community property, and if the debt is legally enforceable against your partner. To get a clear picture of your situation, it’s essential to examine local laws and review your account agreements.

What happens if my partner overdrafts our joint account?

If your partner overdrafts your joint account, both of you are on the hook for repaying the overdraft. The bank has the right to hold either one of you - or both - responsible for the full amount owed. This applies no matter who caused the overdraft, making it crucial to keep a close eye on the account and maintain open communication about spending habits.

How can we prove who made a disputed charge on a joint account?

To figure out who made a disputed charge on a joint account, start by examining the account's transaction history and bank records. These records usually include details like the date, amount, and recipient of each transaction, which can point to the person responsible. If the details remain unclear, reach out to your bank for further assistance in resolving the issue.