Open Banking Explained: Benefits for Consumers and Fintech Startups

Open banking is transforming how financial data is shared and used, giving you control over who can access your financial details. By using secure APIs, it allows apps and services to access specific data - like your transaction history - without sharing your login credentials. This system enhances security, simplifies financial management, and opens opportunities for personalized tools.

Key highlights:

- Consumer Control: You decide which apps can access your data and can revoke access anytime.

- Security: Tokenized API connections replace outdated methods like screen scraping, keeping your credentials private.

- Convenience: View all your accounts in one place, automate savings, or apply for loans based on real-time cash flow.

- Fintech Growth: Startups can build better financial tools using real-time data, reducing costs and development time.

As of April 2026, open banking is growing rapidly, with over 76 million U.S. accounts sharing data securely through APIs. The CFPB’s new rule requires large banks to offer API access, ensuring broader adoption and innovation. Whether you’re a consumer or a fintech entrepreneur, open banking is reshaping financial services for the better.

How is Open Banking transforming finance - and who stands to benefit?

sbb-itb-5d40823

How Open Banking Works

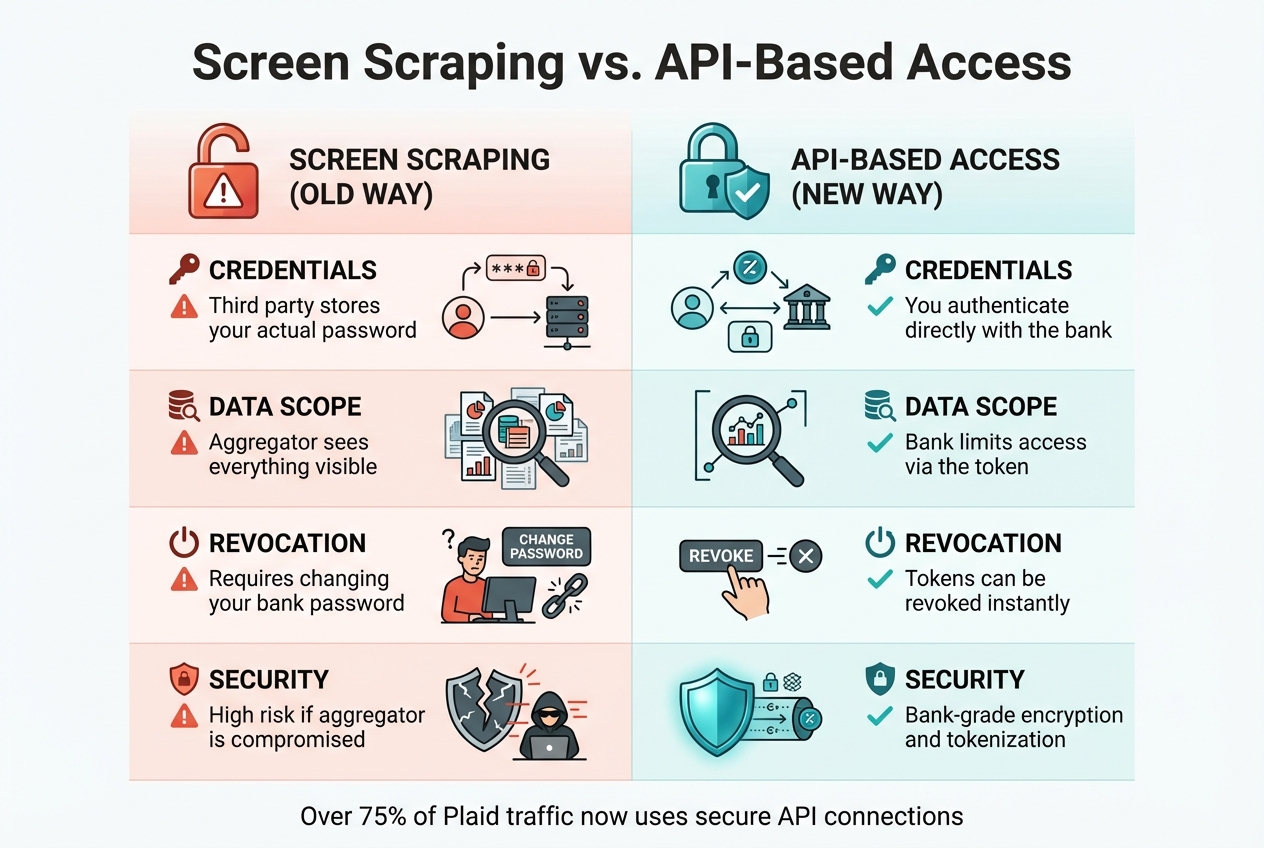

Screen Scraping vs API-Based Open Banking: Security and Access Comparison

APIs and Data Sharing

APIs are the backbone of open banking, enabling secure data sharing between your bank and the apps you choose. For example, if you link a budgeting app to your checking account, the API ensures only the approved data - like your current balance or recent transactions - is shared, all without exposing your login credentials.

This is made possible through tokenization. Instead of sharing your actual bank password, your bank issues a temporary, encrypted token. This token can be revoked at any time, adding an extra layer of security. Take Plaid, for instance - a major player in the U.S. financial data space. Plaid connects over 12,000 financial institutions with 7,000 apps, and more than 75% of its traffic now uses these secure API connections.

Organizations like the Financial Data Exchange (FDX) have created standardized API specifications, ensuring seamless compatibility across banks. This means a single app can connect to thousands of institutions without needing custom setups. The result? Real-time updates. Your budgeting app reflects your current balance instantly, eliminating delays caused by outdated data. This efficient system not only improves security but also simplifies consumer consent.

| Factor | Screen Scraping (Old Way) | API-Based Access (New Way) |

|---|---|---|

| Credentials | Third party stores your actual password | You authenticate directly with the bank |

| Data Scope | Aggregator sees everything visible | Bank limits access via the token |

| Revocation | Requires changing your bank password | Tokens can be revoked instantly |

| Security | High risk if aggregator is compromised | Bank-grade encryption and tokenization |

Consumer Consent and Security

While secure data sharing is key, consumer control is at the heart of open banking. You get to decide what information is shared and for what purpose. By logging into your bank's portal, you can approve specific data access - like your account balance or transaction history - for a particular app.

Under the CFPB's Personal Financial Data Rights rule finalized in October 2024, your consent typically lasts for one year before reauthorization is needed. At any time, you can revoke access through your bank's app or the third-party service. Once access is revoked, the token is immediately invalidated, halting any further data sharing.

Strong Customer Authentication (SCA) adds another layer of security. Two-factor verification is required for every API connection, whether that's entering a code sent to your phone or confirming through your banking app. This shift from screen scraping to token-based authentication has significantly reduced security risks. For example, in 2021, the FTC settled with Plaid for $58 million over allegations of collecting unnecessary data using login screens designed to look like bank interfaces.

"Open banking is built on the concept that consumers own their financial data and can choose to share it with third-party providers." – Stripe

Banks now provide permissions dashboards, where you can see all active connections, review what data each app can access, and revoke tokens for services you no longer use. This transparency ensures your financial data is working for you, not against you. Open banking aims to empower both consumers and fintech companies by combining security with clear, user-friendly innovation.

Benefits for Consumers

Better Transparency and Control

Open banking puts you in charge of your financial data. Instead of juggling multiple apps to track your checking account, credit cards, savings, and investments, you can view everything in one place. This consolidated view gives you a real-time look at your net worth and cash flow, making financial management much easier.

You also decide who gets access to your data, what they can see, and for how long. For example, if you want a budgeting app to analyze your spending but don’t want it to access your account numbers, you can grant that specific permission. Changed your mind? No problem - you can revoke access instantly through your bank’s portal, keeping you in full control.

Real-time data also helps you catch spending habits early. Budgeting tools can flag recurring payments that might lead to overdrafts. In fact, over 76 million U.S. consumer accounts already use FDX APIs for secure and efficient data sharing.

Beyond control, open banking tailors your financial experience to fit your needs.

Personalized Financial Services

With greater transparency and control, open banking enables services that make managing your money easier. Apps can automatically categorize your transactions - labeling purchases as "Groceries", "Gas", or "Entertainment" - so you don’t have to track everything manually. This automation is a game changer, especially since 88% of people struggle to stick with daily manual transaction tracking.

These tools don’t just save time; they can save you money too. Many users report saving an extra $50 a month simply by using cash flow analysis tools. Some apps even go a step further, scanning your accounts to recommend higher-interest savings accounts or better credit options.

Lending also becomes more accessible. For example, in April 2025, Affirm used Plaid’s open banking integration to assess real-time cash flow and account balances during checkout. This allowed them to offer credit to customers who had limited credit histories but enough liquidity to repay loans. Using cash flow underwriting, banks can approve 20% to 40% of applications that traditional credit scoring might reject. For those with thin credit files, this approach opens up opportunities that were previously out of reach.

Fraud Prevention and Financial Access

Open banking doesn’t just make financial management easier - it also enhances security and expands access to essential services. API-based tokenization replaces outdated methods, keeping your credentials private. Even if a fintech app is breached, hackers can’t access your bank account because they never had your password in the first place.

Identity verification becomes more robust too. By using bank-verified data, modern systems can detect suspicious activity, like attempts to link an account through a privacy browser or virtual machine, and flag potential fraud in real time.

For underserved communities, open banking offers new ways to access financial services. Those living in areas without banks or with limited credit histories can use alternative data, like utility payments or consistent cash flow, to prove financial responsibility when applying for loans or housing. This cash flow underwriting approach prioritizes steady income and responsible spending over traditional credit scores. Already, 91% of Americans have used some form of open banking service, from budgeting apps to peer-to-peer payment platforms. By improving security and broadening access, open banking helps level the playing field, making financial tools available to more people than ever before.

Benefits for Fintech Startups

While consumers gain greater control and security, fintech startups leverage these advancements to boost efficiency and fuel growth.

Access to Real-Time Consumer Data

Open banking provides startups with instant access to up-to-date financial data. Instead of relying on outdated credit bureau reports, fintech companies can now analyze live transaction histories, account balances, and income patterns. By using data aggregators like Plaid and Finicity, startups can connect to thousands of banks with a single integration, avoiding the complexity of building individual connections. Through secure, read-only APIs for Account Information Services (AIS), startups can create tools like budget planners, personal finance apps, and lending platforms - all without handling sensitive login details. Real-time cash flow analysis also replaces traditional credit scores, making credit underwriting more inclusive. This immediate data access not only drives financial product innovation but also shortens the time to market for new offerings.

Lower Costs and Faster Development

Open banking significantly cuts costs and speeds up development for fintechs. Account-to-Account (A2A) payments, for instance, cost just a few cents per transaction compared to the 1.5% to 2.5% fees charged by traditional card networks. Automated processes for payment reconciliation, income verification, and KYC checks reduce manual workloads during onboarding and credit assessments. These efficiencies enable instant credit decisions and faster customer onboarding. Additionally, startups can use Banking-as-a-Service (BaaS) platforms to launch financial products without needing a full banking license. These cost-saving measures and streamlined operations allow startups to scale more efficiently.

Scaling and Market Growth

Standardized API frameworks make it easier for startups to integrate with multiple major banks at once, bypassing the need for individual partnerships and accelerating their market reach. Beyond payments, fintechs are embedding financial services into platforms like accounting software, online marketplaces, and ERP systems. This "embedded finance" approach integrates financial tools into users' everyday workflows. Brazil’s open finance framework, which recorded over 800 million data-sharing consents by 2024, demonstrates the vast potential when supported by effective regulations. For startups with global ambitions, working with data aggregators that operate across multiple jurisdictions simplifies access to banks in different countries, opening doors to rapid international growth.

Open Banking and Transaction Dispute Recovery

Open banking isn't just about simplifying payments or helping you budget better - it’s also reshaping how transaction disputes are handled. By leveraging detailed transaction data through open banking APIs, platforms like DidIBuyIt can analyze disputes more thoroughly and build stronger cases for consumers seeking refunds. This highlights one of open banking's key advantages: giving people greater control over their financial lives.

AI-Powered Dispute Analysis

When you spot a charge on your statement that doesn’t look right, acting fast is crucial. Banks typically have 10 business days to conduct an initial investigation, but full resolution can stretch anywhere from 45 to 90 days. Open banking APIs, particularly those under Account Information Services (AIS), provide immediate access to critical transaction details like account balances, transaction histories, and metadata - cutting out the delays that used to slow things down.

"Open Banking can provide a more detailed transaction history, making it easier to investigate and resolve chargeback disputes accurately." - Rebecca Gilpin

AI tools now take this data and work in real time to spot patterns, compare merchant records, and flag inconsistencies. This automated process not only speeds things up but also ensures disputes are handled impartially, often without needing human intervention. Additionally, Strong Customer Authentication (SCA), which uses multi-factor verification, helps reduce fraudulent claims of unauthorized transactions by making it harder for bad actors to initiate payments. Together, these advancements are paving the way for even more efficient dispute resolution.

Tools for Chargeback Management

Platforms like DidIBuyIt are taking these capabilities a step further with automated tools designed specifically for managing chargebacks. Using AIS, the platform can pull receipts, order confirmations, and cancellation emails directly from your bank accounts. It then generates bank-compliant documentation to support your chargeback claim.

The platform’s AI dives into your transaction data to pinpoint issues like duplicate charges, canceled subscriptions that continue to bill you, or purchases that never arrived. With access to data from multiple financial institutions, DidIBuyIt can monitor your transactions in real time and alert you to suspicious activity right away. When a dispute does arise, open banking frameworks enable seamless communication between you, your bank, and third-party providers to strengthen your case. This streamlined process replaces the old, clunky system where consumers had to juggle communication between merchants and banks themselves, giving you more clarity and control over the resolution process.

Examples and Future of Open Banking

Open Banking in Practice

Open banking has evolved into a driving force behind many of the financial tools we use daily. Apps like YNAB, Monarch Money, and Rocket Money rely on aggregators such as Plaid and Finicity to link directly to users' bank accounts, automatically importing transaction data. This feature is critical - 88% of users report that manually entering transactions is simply not sustainable.

Payment platforms like Venmo and PayPal also benefit from open banking. They allow users to link bank accounts instantly, skipping the tedious process of manually entering routing and account numbers. For businesses, open banking simplifies operations in transformative ways. For example, in 2025, Affirm used Plaid’s real-time cash flow data to offer Buy Now, Pay Later services tailored to users with limited credit histories. DoorDash uses similar tools to verify gig workers’ earnings in real time, eliminating the hassle of uploading pay stubs. That same year, Moneybox launched "Payday Boost", a service powered by Variable Recurring Payments (VRPs). This feature lets users instantly transfer funds into retirement or investment accounts on payday, bypassing the typical five-day wait for direct debits.

These examples highlight how open banking is shaping the financial landscape and paving the way for even more advancements.

What's Next for Open Banking

The future of open banking is poised to go far beyond its current scope. The next step, often referred to as "Open Finance", will incorporate data from a wider range of financial products, including investments, insurance, pensions, and mortgages. By 2030, the global open banking market is expected to grow to $135.2 billion, with the Asia-Pacific region leading the charge, growing at nearly 30% annually. Brazil is already showing what’s possible - by 2024, its open finance system had recorded over 800 million data-sharing consents.

Another emerging trend is account-to-account (A2A) payments. These direct transfers bypass traditional credit card networks, offering merchants lower fees and instant settlements while providing consumers with faster checkout experiences. Artificial intelligence is also becoming a game-changer in this space. Financial platforms are using AI to identify recurring subscriptions, predict potential cash flow issues, and even offer pre-approved credit based on transaction histories.

The horizon for open banking is vast, with innovation and integration set to redefine how we interact with our finances.

Conclusion

Open banking is revolutionizing how we engage with financial services. By breaking down data silos and enabling secure, consumer-directed data sharing, it offers a clearer picture of your finances. This means you can view all your accounts in one place, gain insights tailored to your spending habits, and even access improved loan terms or interest rates that traditional assessments might miss.

But it’s not just consumers who benefit - fintech startups are reaping rewards too. With real-time access to transaction data, these companies can innovate faster, reduce development costs, and provide financial solutions to underserved communities.

"Open banking is the foundational infrastructure layer of a new financial data economy"

The numbers back it up: over 76 million consumer accounts now use FDX APIs, highlighting open banking’s rapid adoption and its impact on personal finance and fintech growth.

The future looks even more promising as the industry shifts toward Open Finance, which will integrate investments, insurance, pensions, and mortgages into one ecosystem. Combined with AI-driven insights and account-to-account payments, open banking is reshaping how money flows and financial decisions are made.

Whether you're managing your own finances or driving the next big fintech idea, open banking provides the tools to take charge, innovate, and achieve better financial outcomes. The days of fragmented financial data are fading, paving the way for a more transparent and connected financial landscape.

FAQs

Is open banking safe to use?

Open banking can be considered safe when implemented with secure, standardized APIs and built around user consent. It relies on encrypted communication channels to protect your sensitive information. Additionally, it adheres to strict regulatory frameworks designed to safeguard your data.

Key protections include robust security measures, such as encryption and multi-factor authentication, as well as compliance with industry standards that prioritize privacy and security. These safeguards work together to create a secure environment for sharing financial data.

How do I revoke an app’s access to my bank data?

To remove an app's access to your bank data, start by logging into your bank’s online banking platform or mobile app. Most banks offer an option to manage third-party app permissions directly from there. If the app connects through a service like Plaid, you can also manage these connections via your Plaid Portal account. Need help? Reach out to your bank’s customer service team. It’s a good idea to regularly review these connections to keep your financial information secure.

Will open banking affect my credit approval or loan offers?

Open banking changes the way lenders evaluate your creditworthiness by providing access to a broader range of financial data, like your transaction history and account activity - not just your credit score. This deeper insight helps lenders make more precise assessments and may result in loan offers that are customized to your financial habits. For those with responsible financial behavior, it might even boost approval chances. However, it does come with privacy concerns, as sharing this data with third parties requires your consent.