Friendly Fraud vs. True Fraud: The Difference Banks Care About

Friendly fraud and true fraud are two distinct types of payment disputes, and understanding the difference is critical for resolving them effectively. Here's the key takeaway:

- True Fraud: Occurs when a criminal uses stolen payment details to make purchases without the cardholder's knowledge. The cardholder is not involved, and banks rely on tools like AI, IP tracking, and behavioral biometrics to detect it. Merchants rarely recover losses from true fraud.

- Friendly Fraud: Happens when a legitimate cardholder disputes a valid purchase. This can be unintentional (e.g., forgetting a subscription) or deliberate (e.g., claiming an item wasn’t delivered). It accounts for 75% of chargebacks, costing merchants $3.60 for every $1 lost.

Banks investigate disputes by analyzing transaction data, timestamps, and customer behavior. Merchants and consumers both benefit from strong evidence and proactive measures. Tools like DidIBuyIt streamline documentation and help navigate disputes efficiently.

Quick Comparison Table:

| Feature | True Fraud | Friendly Fraud |

|---|---|---|

| Who Initiates | Criminals using stolen data | Legitimate cardholder |

| Intent | Theft | Mistake or opportunism |

| Detection Timing | At checkout | After purchase |

| Merchant Recovery | Rare | Possible with evidence |

Friendly fraud is a growing issue, with disputes projected to rise by 42% by 2026. Merchants can reduce risks by using clear billing descriptors, tracking deliveries, and maintaining records, while consumers should review charges carefully before filing a chargeback.

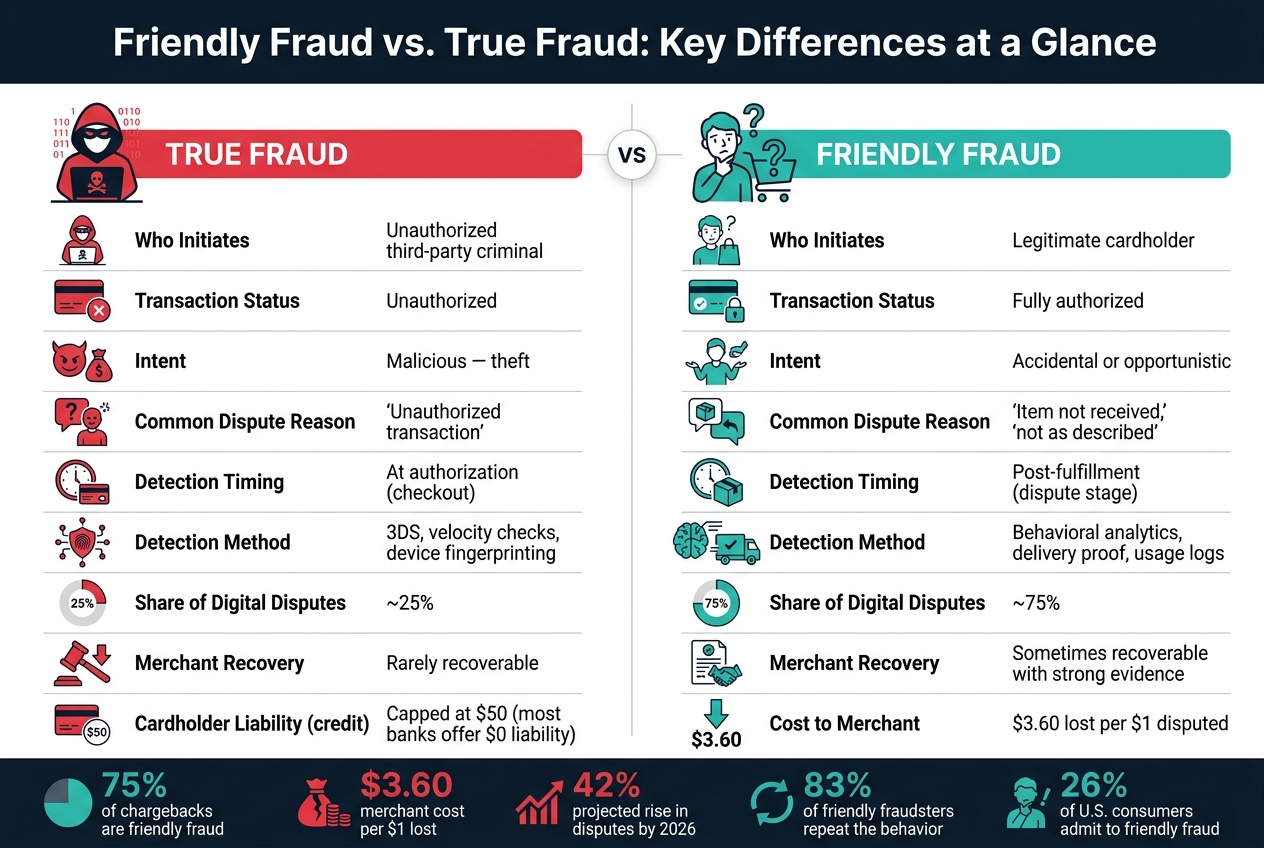

Friendly Fraud vs. True Fraud: Key Differences at a Glance

Friendly Fraud Is RUINING Your Business - How to Stop Losing Money

sbb-itb-5d40823

What Is True Fraud?

True fraud, often referred to as third-party fraud, happens when a criminal uses stolen payment details to make unauthorized purchases. In these situations, the actual cardholder is completely unaware of the transaction - they neither initiate nor approve it. Usually, the cardholder only discovers the fraudulent activity after checking their bank statement or receiving an alert from their financial institution.

"True fraud is when a third party uses stolen credit card information to make an unauthorized transaction." - Chargeback Gurus [8]

Characteristics of True Fraud

True fraud starts with compromised payment data. Criminals acquire this information through methods like phishing scams, data breaches, account takeovers, or skimming devices. Often, they first make small test purchases to check if the card works before moving on to larger fraudulent transactions [8].

A defining characteristic of true fraud is that the cardholder is completely uninvolved. They never consent to the transaction. Thanks to the Fair Credit Billing Act, credit cardholders' liability for unauthorized charges is capped at $50, though most banks now offer zero-liability policies. For debit cards, reporting fraud within two business days limits liability to $50, but if the fraud goes unreported for more than the standard chargeback windows, the cardholder may be responsible for the entire loss [8].

Merchants also face significant losses from true fraud. Beyond losing revenue, they often deal with stolen inventory, shipping costs, and chargeback fees. Merchants with high fraud rates may even face stricter oversight from card networks or risk losing their payment processing privileges altogether [6].

How Banks Detect True Fraud

Banks rely on advanced tools to identify and stop true fraud in real time. They use AI and machine learning systems to monitor transactions for unusual activity, such as a sudden large purchase in a different state or a transaction from an unfamiliar IP address [8].

Banks also analyze behavioral biometrics - like typing speed and mouse movements - to create a unique profile for each account holder. This makes it harder for fraudsters to mimic legitimate users [8]. On the technical side, tools like tokenization (replacing card numbers with unique identifiers), EMV chip technology, and 3D Secure 2.0 multi-factor authentication add extra layers of security during transactions [6].

Under Regulation E, banks are required to investigate fraud claims within 10 business days. If the investigation takes longer, they must provide provisional credit to the affected consumer while continuing their review for up to 45 days [9].

What Is Friendly Fraud?

Friendly fraud - sometimes called first-party or chargeback fraud - happens when a customer disputes a legitimate purchase with their bank instead of requesting a refund directly from the merchant. Unlike cases of true fraud, this doesn’t involve stolen card details or criminal activity. Instead, the cardholder themselves initiates the dispute. While some disputes may arise from genuine misunderstandings, others are intentional attempts to avoid paying for a purchase.

The term "friendly" might sound harmless, but it simply refers to the fact that the dispute comes from the actual customer, not from someone using stolen credentials. This type of fraud is surprisingly common - 26% of U.S. consumers admit to engaging in it, and 72% of cardholders view chargebacks as an acceptable alternative to asking the merchant for a refund [3][5].

"Friendly fraud isn't just a fraud issue. It's a post-purchase behavior issue. And for many brands, it's the largest driver of dispute rates." - Jodi Lifschitz, Head of Content, Chargeflow

Common Traits of Friendly Fraud

Friendly fraud often starts with something that seems minor or even unintentional. For example, a charge might go unrecognized because the billing descriptor doesn’t match the store name, or a customer might forget about a subscription renewal. Sometimes, a family member makes a purchase on a shared account, and the primary cardholder disputes the charge as unauthorized.

Modern banking apps have made disputing charges incredibly easy - often just a few clicks away - which can make this approach more appealing than contacting the merchant directly.

Types of Friendly Fraud

Friendly fraud can take several forms, including:

- Buyer’s remorse: A customer regrets a purchase, whether it was an impulse buy or a product that didn’t meet expectations, and disputes the charge instead of returning the item.

- Subscription forgetfulness: A customer signs up for a free trial, forgets to cancel, and later disputes the charge when the subscription renews.

- Family fraud: A household member uses a shared account to make a purchase without the primary cardholder’s knowledge, leading to a dispute.

- Cyber shoplifting: A customer receives a product but claims it was never delivered or arrived damaged, allowing them to keep both the item and the refund.

The financial toll of friendly fraud is no small matter. For every $1 lost to friendly fraud, merchants face an average cost of $3.60 when factoring in fees, lost inventory, and administrative expenses. Even more concerning, 83% of those who commit friendly fraud are likely to do it again [3][10].

Key Differences Between Friendly Fraud and True Fraud

The main difference between friendly fraud and true fraud boils down to one critical question: who made the purchase? In true fraud, a criminal uses stolen card details to make unauthorized transactions that the actual cardholder never approved. On the other hand, friendly fraud occurs when the legitimate cardholder makes the purchase but later disputes it. This key distinction significantly affects how banks investigate these cases.

True fraud often triggers alerts during checkout. Signs like unusual locations, mismatched devices, or a high volume of rapid transactions can raise suspicion before the order is even processed. In contrast, friendly fraud looks completely normal at the time of purchase since it’s a legitimate transaction. The problem only arises later when the cardholder files a dispute.

The intent behind these fraud types also sets them apart. True fraud is always malicious - someone is intentionally stealing. Friendly fraud, however, spans a range of scenarios. It could be a genuine mistake, such as a customer not recognizing a billing descriptor, or it could be deliberate, like someone disputing a charge to keep both the product and their money.

Here’s a side-by-side breakdown of the differences:

Comparison Table: Friendly Fraud vs. True Fraud

| Feature | True Fraud | Friendly Fraud |

|---|---|---|

| Initiator | Unauthorized third-party criminal | Legitimate cardholder |

| Transaction Status | Unauthorized | Fully authorized |

| Intent | Malicious - theft | Accidental or opportunistic |

| Common Dispute Reason | "Unauthorized transaction" | "Item not received", "not as described" |

| Detection Timing | At authorization (checkout) | Post-fulfillment (dispute stage) |

| Detection Method | 3DS, velocity checks, device fingerprinting | Behavioral analytics, delivery proof, usage logs |

| Frequency (digital disputes) | ~25% of disputes | ~75% of disputes [2] |

| Recoverability for Merchants | Rarely recoverable | Sometimes recoverable with strong evidence |

For online merchants, friendly fraud is an especially big problem. It accounts for 60% to 80% of all chargebacks [4], making it the most common issue by far. Because of this, merchants and banks need to approach friendly fraud and true fraud differently. Each requires its own evidence and strategies, and using the wrong approach can lead to wasted resources and strained relationships with customers.

How Banks Investigate Fraud Claims

When a cardholder disputes a charge, banks follow a structured process to determine whether the transaction was authorized. Depending on whether it’s a case of true fraud or friendly fraud, banks adjust their approach to collecting evidence and resolving the issue.

Evidence Evaluation

The investigation begins with the bank gathering information from the cardholder. They’ll ask for transaction specifics and why the charge is believed to be fraudulent. For example, was the card lost or stolen? Investigators then dive into transaction data - examining timestamps, IP addresses, location details, and device IDs. These clues can help determine if the cardholder was physically or digitally present during the transaction, which might point to friendly fraud.

Banks also look for patterns typical of true fraud, like card testing. This happens when fraudsters make small purchases to confirm a stolen card works before attempting larger transactions. On the other hand, friendly fraud might stem from forgotten subscriptions, accidental in-app purchases by children, or disputes over charges after a free trial ends.

When merchants challenge a chargeback through a process called representment, they submit evidence (and the merchant will know you filed it) such as delivery confirmations, signed invoices, IP logs, or customer service communications. Under Visa's Compelling Evidence 3.0 (CE3.0) framework, merchants can even use two prior transactions with matching IP addresses or device IDs (older than 120 days) to show the cardholder has an established history with their business [1]. Once all evidence is collected, banks follow strict timelines to resolve the dispute.

Timelines and Resolution Processes

The Fair Credit Billing Act requires banks to make a decision within 10 business days. If more time is needed, the investigation can extend to up to 45 days, provided the bank issues provisional credit to the cardholder’s account within the initial 10-day window [8].

Cardholders usually have 60 to 120 days from the transaction date to dispute a charge, depending on the bank and card network. For merchants, the representment process typically takes at least 30 days. If the bank sides with the cardholder after reviewing the merchant’s evidence, the case may escalate to arbitration. At this stage, the losing party could face additional fees running into hundreds of dollars.

| Investigation Phase | Timeline | What Happens |

|---|---|---|

| Initial Review | 10 business days | Bank evaluates the claim and issues a decision or provisional credit [8] |

| Extended Investigation | Up to 45 days | Further evidence analysis; provisional credit must be issued [8] |

| Dispute Filing Window | 60–120 days | Timeframe for cardholders to file a dispute [8] |

| Merchant Representment | 30+ days | Merchant submits evidence; bank re-assesses the chargeback [8] |

Why This Distinction Matters for Banks and Merchants

Understanding the type of fraud at play isn't just a technicality - it carries major financial consequences for both banks and merchants.

The Cost of Fraud

By 2026, global chargeback volumes are projected to reach 337 million annually, marking a 42% rise from 2023. Resolving a single dispute can cost two to three times the original transaction amount [11][12]. For example, a $50 dispute can balloon to $150 once you factor in fees and operational costs - not to mention the expense of the lost product.

"Friendly fraud is the cost nobody budgets for. A 1% dispute rate on a $50 subscription sounds manageable until you add the chargeback fee, the lost revenue, the operational cost of responding, and the threat to your merchant account." - Rishabh Goel, Co-founder & CEO, Dodo Payments [4]

Banks face their own challenges. Investigating a single dispute can cost up to $70 in staff time and resources [11]. Outdated, rule-based systems only make things worse, with false positive rates often exceeding 90% - meaning most flagged cases actually involve legitimate customers [12]. And the stakes are high: around 17% of cardholders either reduce or completely stop using their cards after a poor dispute experience [12]. This underscores how crucial it is to correctly identify fraud types. To tackle these issues, banks and merchants are increasingly turning to AI tools to simplify the process and cut costs.

How AI Tools Like DidIBuyIt Help

At first glance, true fraud and friendly fraud can look almost identical: the card was used, the purchase went through, and the transaction amount seems normal. The key difference lies in the context, and that's where AI tools like DidIBuyIt come in.

For consumers, DidIBuyIt's AI-powered analysis reviews transaction details to determine if a dispute is justified or if the merchant's refusal can be challenged. It then helps frame the case effectively and generates documentation tailored to meet banks' evidentiary standards.

For merchants, the tool simplifies the process of building a strong defense. DidIBuyIt organizes critical digital records - such as login timestamps, delivery confirmations, and usage logs - into a clear and structured response. This helps merchants present a solid case when disputes arise, saving time and reducing the risk of financial loss.

Prevention Strategies for Consumers and Merchants

Taking action to prevent fraud before it occurs is key for both consumers and merchants. By adopting proactive measures, you can significantly lower the risks.

Preventing True Fraud

To guard against true fraud, layered security is your best bet. These measures make it much harder for someone to misuse stolen card details.

Start by enabling multi-factor authentication (MFA) on your banking and shopping apps. Pair that with 3D Secure (3DS) at checkout, which adds an extra verification step to confirm the cardholder's identity. Together, these steps create a strong barrier against unauthorized transactions.

Simple habits also go a long way. Never share one-time passwords (OTPs), avoid making transactions over public Wi-Fi, and keep a close eye on your bank statements to catch any suspicious activity early. A 2020 survey revealed that 38% of participants had experienced account takeovers in the previous two years [5], highlighting how common these attacks have become.

Reducing Friendly Fraud

Friendly fraud is tougher to address because it starts with a legitimate purchase. For merchants, the goal is to minimize customer confusion and prevent disputes over valid transactions.

One effective tactic is using clear billing descriptors. If the name on a customer’s statement doesn’t match the brand they know, they might assume the charge is fraudulent. Including a customer service phone number in the descriptor gives them a way to resolve confusion without filing a chargeback. Additionally, sending order confirmations, shipping updates, and delivery tracking links can significantly reduce "item not received" claims. Make sure your return policy is easy to find and encourages customers to use it instead of disputing charges. First-party fraud reports surged from 14.6% in 2024 to 35.9% in 2025 [13], making clear communication and transparency more important than ever.

"Friendly fraud might sound like a contradiction. There's nothing friendly about a customer disputing a legitimate purchase and costing you the transaction amount, chargeback fees, and hours of operational work." - Primer [14]

For merchants dealing with repeat offenders, keeping detailed records is crucial. Document login timestamps, delivery confirmations, and customer service interactions. This evidence strengthens your case when disputing chargebacks and can be further streamlined with AI tools designed to manage documentation.

How DidIBuyIt Can Help

Whether you’re a consumer reporting an unauthorized charge or a merchant disputing a wrongful claim, having the right documentation can make all the difference. DidIBuyIt offers an AI-powered platform that reviews transaction details, assesses whether a dispute is valid, and generates professional, bank-ready documentation tailored to what financial institutions require.

For merchants, it organizes digital records into a structured format ready for submission. For consumers, it provides step-by-step guidance to ensure all necessary documentation is included. Supporting major payment platforms like Visa, Mastercard, Amex, and PayPal, DidIBuyIt ensures data security with encryption at every step of the process.

Conclusion: How to Handle Fraud Disputes with Confidence

Here’s the bottom line: true fraud happens when criminals use stolen credentials to make unauthorized transactions, while friendly fraud occurs when a legitimate cardholder disputes a valid purchase. Banks treat these two scenarios very differently, so it’s crucial for merchants and consumers to understand the distinction.

The financial impact is no small matter. Friendly fraud accounts for the majority of chargebacks, and for every $1 lost, merchants face an additional $3.60 in costs due to fees, lost goods, and other expenses [3].

Handling disputes incorrectly can be pricey. Merchants who exceed a 1% chargeback rate risk being added to the MATCH List [10], which can severely limit their ability to process payments. On the other hand, consumers who frequently file questionable disputes may face reduced privileges or even account reviews [7].

Preparation is everything. Merchants should keep thorough records - like delivery confirmations, IP logs, and communication history - to build strong representment cases. For consumers, reaching out to the merchant first is a smart move, as banks track dispute patterns over time [3][7]. Tools like DidIBuyIt’s AI-powered platform can simplify the process by compiling evidence that aligns with the standards of major payment networks like Visa, Mastercard, Amex, and PayPal. Whether you’re a consumer questioning a charge or a merchant disputing a chargeback, having the right documentation can make all the difference. If your initial claim is rejected, understanding the chargeback appeal process is the next step.

FAQs

How can I tell if a charge is true fraud or friendly fraud?

True fraud occurs when stolen card details or compromised accounts are used for unauthorized transactions. On the other hand, friendly fraud happens when a cardholder disputes a charge they actually authorized. This can stem from misunderstandings, buyer’s remorse, or even accidental purchases.

To distinguish between the two, it’s important to look at key factors like whether the charge matches the cardholder’s usual spending habits or if they recognize the transaction. For merchants, gathering evidence is crucial. Things like purchase records, delivery confirmations, and other transaction details can help build a strong case.

What evidence actually helps win a chargeback?

To successfully contest a chargeback, you need to present clear and well-organized documentation. This includes:

- Proof of the transaction: Provide receipts or invoices showing the purchase details.

- Delivery or service records: Show evidence that the product was delivered or the service was completed as promised.

- Customer communication: Include emails, messages, or other correspondence proving the customer authorized the purchase.

Additionally, supply any materials that directly counter the claim or clarify any misunderstandings. The key is to ensure your records are thorough and easy to follow, making it clear why the chargeback is unwarranted.

Can filing too many disputes hurt my bank account?

Filing too many disputes can indeed have a negative impact on your bank account. Each chargeback, even in cases of friendly fraud, comes at a cost. On average, merchants and banks lose $2.40 for every dollar of fraud. If disputes become excessive, your financial institution might impose account restrictions or subject your transactions to closer scrutiny.