How Fintech Is Reshaping Personal Finance Management

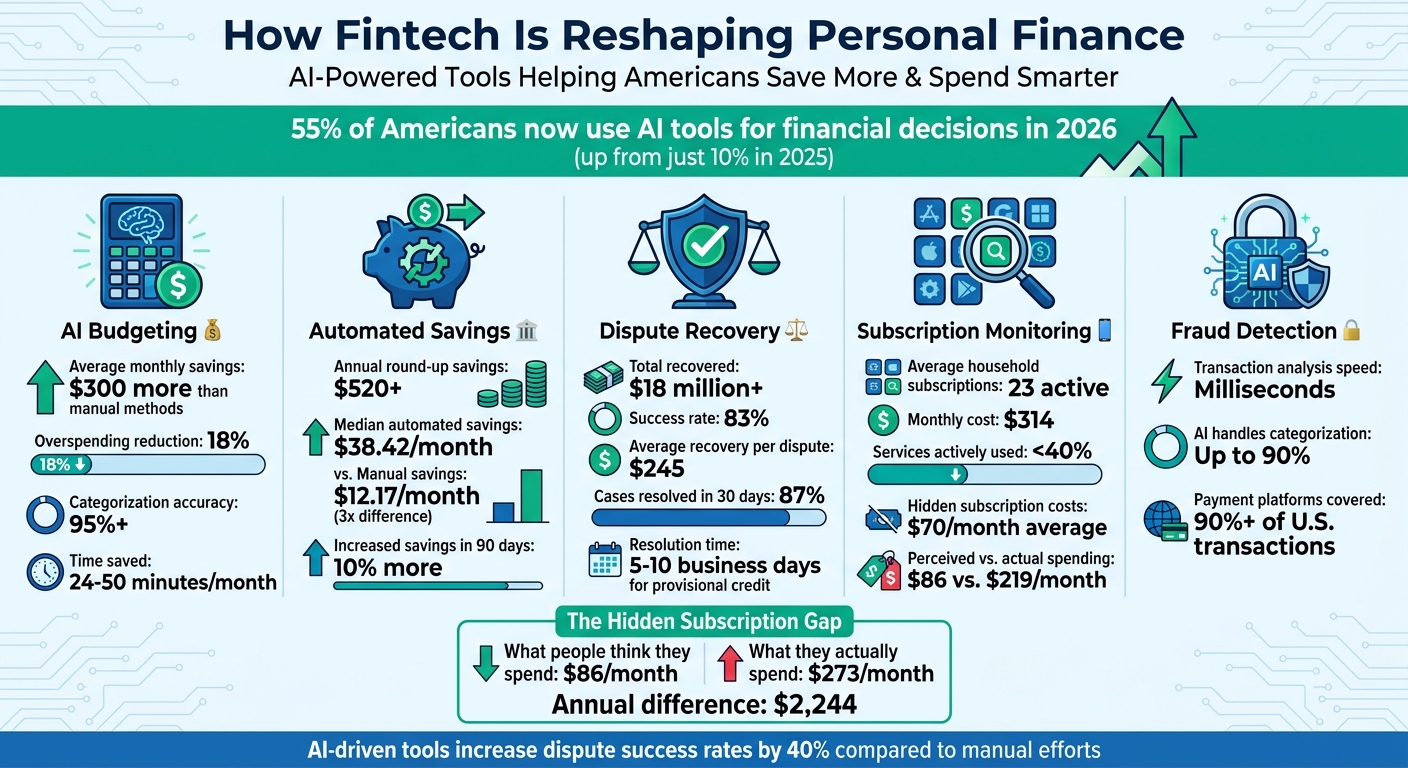

Managing your money is no longer just about tracking expenses - it’s about letting technology do the hard work for you. By 2026, 55% of Americans are using AI tools for financial decisions, up from just 10% in 2025. These tools don’t just monitor your spending, they actively help save money, detect fraud, and manage subscriptions. Here's what fintech is doing for personal finance:

- AI Budgeting: Real-time alerts, automatic categorization, and spending forecasts help users save $300 more monthly.

- Automated Savings: Features like round-ups and "safe-to-save" analysis make saving effortless, adding up to $520+ annually.

- Dispute Recovery: AI platforms like DidIBuyIt recover $245 per dispute on average, with an 83% success rate.

- Subscription Monitoring: AI reveals hidden costs, flagging unused subscriptions that cost households $314/month on average.

- Fraud Detection: Instant alerts catch suspicious activity before it affects your account.

Fintech is making money management smarter by automating tasks, saving time, and helping users keep more of their earnings. Let’s dive into how these tools work and why they’re changing the game.

How Fintech AI Tools Are Transforming Personal Finance in 2026

AI in Fintech: What’s Changing Behind the Scenes at Banks with Jason Pereira

sbb-itb-5d40823

AI-Powered Budgeting and Expense Tracking

AI-driven budgeting is changing the way people manage their finances by connecting directly to bank accounts through secure APIs like Plaid and MX. This allows for real-time transaction monitoring, setting the stage for tools that help with savings and even dispute recovery. The result? A more dynamic and transparent approach to money management that helps avoid those dreaded end-of-month surprises.

The results speak for themselves. On average, users of automated budgeting tools save $300 more per month compared to those using manual methods. Additionally, early trials show that these tools can cut overspending by 18%. This is achieved through three key features: real-time alerts, automatic expense categorization, and proactive warnings to address potential issues before they escalate.

Real-Time Spending Alerts

AI-powered budgeting apps use advanced algorithms to analyze spending patterns and immediately flag unusual activity, such as duplicate subscriptions or unexpected price increases. These alerts also update a "Safe Daily Spend" figure in real time, helping users stay on track.

Some systems go even further by identifying emotional spending triggers. For example, they might flag late-night purchases or spending after a stressful day, offering insights into not just what you're spending but why. By combining instant notifications with intelligent analysis, these tools make it easier to adjust spending habits as they happen.

Automated Expense Categorization

Manually tagging transactions is tedious - especially since the average person has around 50 financial transactions per month. AI eliminates this hassle by automatically categorizing purchases into groups like groceries, dining out, or subscriptions.

Using key details like merchant name, transaction amount, and time, AI matches spending to historical patterns with over 95% accuracy. For instance, a charge from "STARBKS" at 8:30 AM is likely coffee, not groceries. Accuracy improves as the system learns: new users generally see 70–80% accuracy initially, which can climb to 90–93% after about 50 manual corrections. For recurring merchants, accuracy often reaches 98–99%.

"The difference between traditional budgeting and AI budgeting is like the difference between manually shifting gears and having an automatic transmission. One requires constant attention and skill; the other just works." – OptiVault

This automation saves users between 24 and 50 minutes each month compared to manual tracking. It also provides immediate spending insights, helping users identify "slow leaks" like forgotten subscriptions. For example, while many believe they spend $86 per month on subscriptions, the actual average is closer to $273 - a difference of $2,244 annually.

With this foundation in place, predictive analytics take budgeting to the next level.

Predictive Analytics for Budget Planning

By analyzing past spending, predictive analytics can forecast upcoming bills, adjust daily spending limits, and identify opportunities to save. Unlike traditional budgets, which often fail when unexpected expenses arise, AI-powered systems adapt in real time. This flexibility is one reason why nearly 80% of people abandon traditional budgeting within the first month.

AI also identifies patterns like increased spending on weekends or paydays, helping users make smarter adjustments. You can even ask questions like, "Can I afford a $2,000 vacation next month?" and get tailored answers based on projected income and expenses.

"AI does not wait for mistakes. It anticipates them. If your patterns suggest you are likely to overspend next week, AI can alert you early and suggest a gentle course correction." – Vera Money

With real-time alerts, automated categorization, and adaptive forecasts, AI budgeting tools are redefining how we approach personal finance.

Automated Savings Tools and Goal-Based Planning

Budgeting tools help you track where your money goes, but automated savings features take it a step further by helping you actually save. These systems move money to your savings automatically, removing the need for constant decision-making. Let’s dive into how round-up features and AI-driven analysis make saving easier and more effective.

Round-Up Savings Features

Round-up tools work by saving the spare change from your everyday purchases. For instance, if you buy a coffee for $4.35, the tool rounds it up to $5.00 and transfers the extra $0.65 into your savings. By analyzing transaction data, these tools identify eligible purchases and bundle the round-ups into transfers after transactions are settled.

If you average about 30 transactions a week, you could save over $10 weekly - adding up to more than $520 a year. A study published in January 2026 in the Journal of Behavioral Finance looked at 12,471 users of the Acorns platform. It found that users who automated their round-ups saved a median of $38.42 per month, nearly three times the $12.17 saved by those doing it manually. Plus, manual savers spent an average of 47 seconds per transaction on calculations and app-switching, while automation removed that hassle entirely after setup.

Some tips to maximize round-ups: If you link round-ups to a credit card, ensure you have a checking account buffer - users without one are 3.7 times more likely to face negative cash flow. Also, aim to allocate between 1% and 3% of your take-home pay to round-ups. Exceeding 15% could lead to missed essential payments like rent. Many banks, such as SoFi, offer free round-up features, but standalone apps might charge fees that could eat into your savings.

AI-Driven Safe-to-Save Analysis

While round-ups are great for small savings, they don’t give you the full picture of your finances. That’s where AI-driven "safe-to-save" tools come in. These systems analyze your income, spending patterns, and account balances to figure out how much you can safely set aside without disrupting your daily needs.

AI tools separate fixed expenses like rent and utilities from flexible spending like dining out or entertainment. They also recognize patterns - like higher grocery bills at the end of the month or weekend spending spikes - and adjust savings recommendations accordingly. If your income changes or an unexpected expense pops up, the system recalibrates to avoid overdrafts.

"AI based saving uses software that looks at your spending patterns over time and suggests realistic ways to save based on how you actually live, not how you are told you should live." – Vera Money

Platforms like Piere have shown that users save, on average, 10% more within their first 90 days. Piere’s MyPlan™ feature explains: "A MyPlan™ savings plan shows you exactly how much you can safely set aside each month for your retirement and savings needs, while still covering your bills and everyday expenses". By connecting multiple accounts - checking, savings, and even retirement - these tools can provide even more precise recommendations.

Building on these insights, goal-based sub-accounts can help you allocate savings toward specific objectives.

Goal-Based Sub-Accounts

Goal-based sub-accounts let you save for specific milestones, like creating an emergency fund, planning a vacation, saving for a home, or paying off debt. Think of each sub-account as a digital envelope, earmarking funds for individual goals.

This method taps into psychology. Seeing your progress toward a goal can be incredibly motivating, making money management feel less like a chore and more intuitive. Some platforms even celebrate small achievements, helping reduce the stress often tied to finances. For example, YNAB users save an average of $600 in their first two months and $6,000 in their first year by using a zero-based budgeting approach. AI tools enhance this process by offering tailored advice that feels more like coaching than just reports.

To make the most of goal-based savings, organize your goals by timeline: short-term (1–3 years for emergencies or debt), medium-term (home down payments), and long-term (retirement). This structure helps AI tools model future scenarios more accurately. You can authorize automated transfers based on your safe-to-save analysis and use AI-generated "Insight Cards" to spot unusual spending patterns early. The result? A savings plan that aligns with your life, not the other way around.

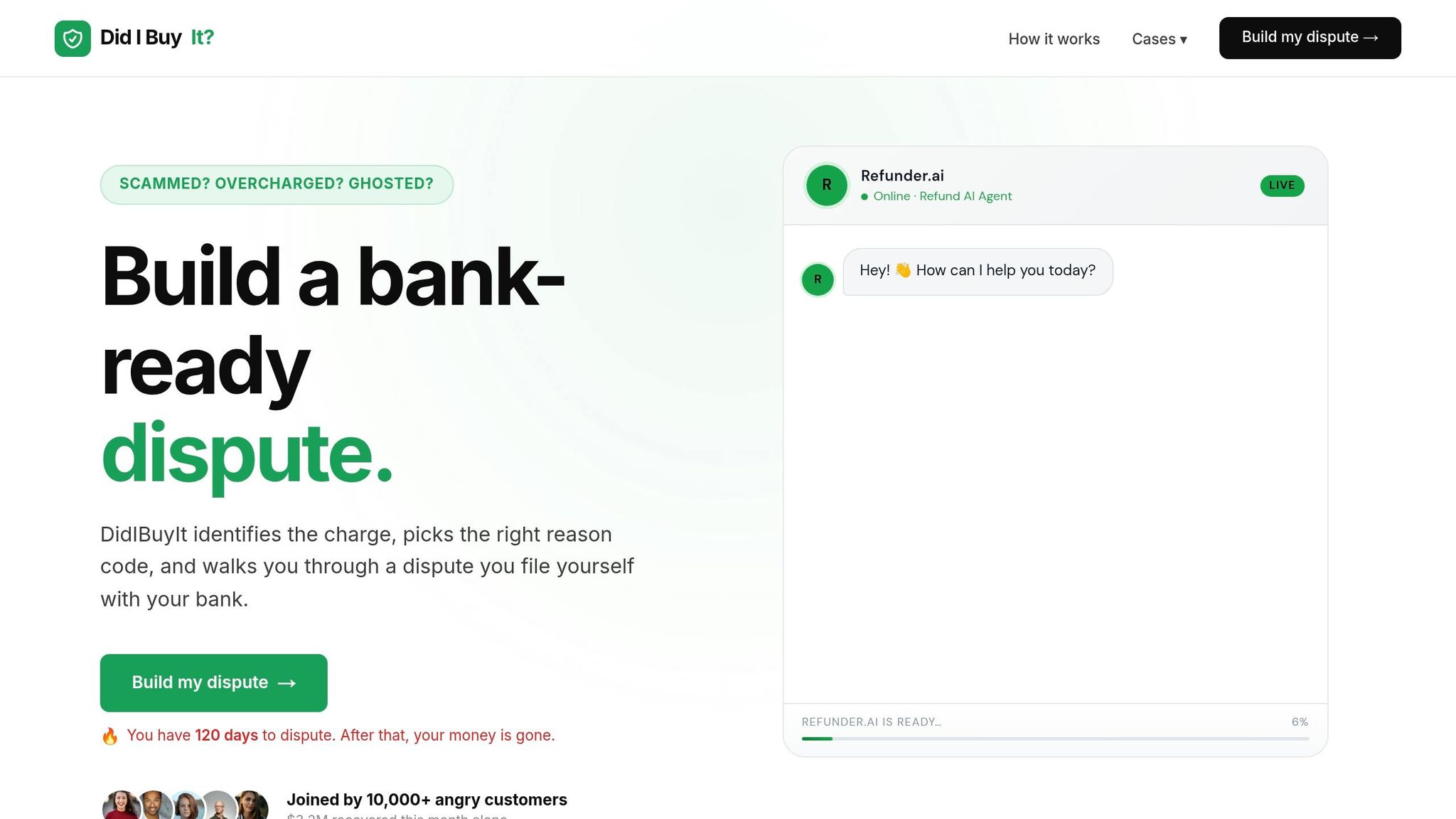

AI-Driven Dispute Recovery: DidIBuyIt

AI is reshaping how we manage finances, and it's making a big difference in dispute recovery too. DidIBuyIt is an AI-powered platform that simplifies the process of resolving unauthorized charges and subscription errors. With over $18 million recovered from more than 284,000 disputes and an impressive 83% win rate, it’s clear that this tool is changing the game for dispute resolution.

AI-Powered Dispute Analysis

DidIBuyIt uses AI to analyze disputed transactions in under three minutes. By examining merchant data, amounts, dates, and patterns, it determines the exact dispute code banks need for approval. This precision is crucial, as 60–80% of chargebacks fail without professional guidance due to incorrect codes or incomplete evidence.

Here’s how it works: Imagine being charged $49.99 for an unauthorized gym membership renewal on your Visa card. The AI identifies it as a fraudulent charge and generates a report with a 92% likelihood of recovery. Or consider a double hotel charge of $250 on your Mastercard - DidIBuyIt’s AI flags the error instantly by matching identical timestamps. It even scans bank statement descriptors within seconds to separate legitimate charges from fraudulent ones.

Once the analysis is complete, the platform compiles all necessary documentation for your dispute.

Bank-Ready Documentation and Step-by-Step Guidance

After analyzing your case, DidIBuyIt creates professional dispute letters in PDF format. These documents include transaction logs, evidence summaries, and timelines specifically formatted for U.S. banks, using dollar signs and proper formatting for thousands. The letters comply with Regulation E, ensuring they meet all banking standards for electronic fund transfers.

The platform walks you through four simple steps: upload your statement, let the AI generate compliant dispute documents, and submit them via your bank’s portal or by mail. It also provides word-for-word scripts for phone calls with your bank and a customized evidence checklist, including critical details like cancellation timestamps and tracking numbers.

"The evidence checklist made the difference. I'd submitted my dispute without the cancellation email timestamp. That one document won the case."

This streamlined process cuts resolution time significantly, with most users receiving provisional credit within 5 to 10 business days.

Support for Major Payment Platforms

DidIBuyIt works seamlessly across major payment platforms, including Visa, Mastercard, American Express, Discover, and digital wallets like PayPal, Apple Pay, Google Pay, Venmo, and Cash App. Together, these platforms account for over 90% of U.S. card transactions. The platform also offers tailored playbooks for over 4,200 banks and credit unions, including major institutions like Chase, Bank of America, Wells Fargo, Citibank, Capital One, and American Express.

The results speak for themselves. For example, a California user recovered $1,200 from fraudulent American Express charges after the AI detected suspicious activity. In another instance, a Texas user reclaimed $350 from PayPal subscription errors, crediting the success to the platform’s bank-ready letters. On average, users recover $245 per dispute, with 87% of cases resolved within 30 days. DidIBuyIt’s AI-driven system increases success rates by 40% compared to manual efforts.

Subscription Monitoring and Fraud Detection

Fintech is reshaping how we manage money, offering tools like real-time budgeting and automated savings. But it doesn’t stop there - subscription monitoring and fraud detection are stepping up to give you even more control over your finances. These tools not only help you keep track of recurring charges but also safeguard your money from fraudulent activities.

Unused Subscription Tracking

Many of us underestimate just how much we spend on subscriptions. As of early 2026, the typical American household has 23 active subscriptions, costing about $314 per month. Yet, most people actively use fewer than 40% of these services. That’s where fintech tools come in. Using AI, they comb through your transaction history to uncover recurring charges you might have forgotten. They even decode vague billing descriptors like "AMZN DIGITAL" (Amazon Prime or Audible) or "APPLE.COM/BILL" (iCloud or Apple Music), linking them to the actual service.

These tools also flag sneaky price hikes between billing cycles and spot duplicate subscriptions, like paying for two Netflix or cloud storage plans. Here’s the kicker: while most people think they’re spending around $86 per month on subscriptions, the real number is closer to $219 - a 2.5x difference. This gap happens because nearly half of recurring charges go unnoticed. And with streaming services raising prices by an average of 13% in 2025, it’s clear why regular subscription audits are essential.

Real-Time Fraud Alerts

Subscription tracking helps you avoid paying for what you don’t use, but fraud detection goes a step further by protecting your money from unauthorized transactions. AI-powered systems analyze transactions in milliseconds, flagging anything suspicious before the payment even goes through. These tools assess everything from device data to behavioral patterns, assigning a risk score to each transaction. For instance, if an unusual international transfer or a charge from an unfamiliar merchant pops up, you’ll get an instant alert on your phone.

The rise of instant payments has made fraud detection even more critical. With money moving in seconds instead of days, AI has to act just as fast to catch unauthorized activity. On top of that, many apps let you take control with features like spending limits, disabling international transfers, or freezing your account instantly. These options put the power in your hands, allowing you to respond to threats the moment they arise.

Future Trends: Open Finance and Embedded Services

Fintech is entering a new era where your entire financial life can be interconnected. Open finance and embedded services are making it easier than ever to access, share, and manage your money securely and without hassle.

Open Finance for Data Sharing

Open finance takes the concept of open banking and broadens it to include your full financial portfolio. This means you can securely link data from pensions, insurance policies, investments, loans, and even cryptocurrency - not just your checking account activity.

With secure APIs, platforms can exchange information in real time, but only with your explicit consent. For instance, Moneyhub, a UK-based platform, uses these APIs to combine data from pensions and investments, helping users create smarter tax strategies. In Brazil, Belvo enables apps to securely access users' banking, tax, and personal finance data, powering tools like budgeting apps and credit scoring systems.

The European Union is advancing this approach through the Financial Data Access (FiDA) regulation, set to roll out between 2026 and 2027. This regulation aims to make data sharing across your financial accounts easier and more standardized. In North America, the Financial Data Exchange (FDX) standard already covers over 60 million consumer accounts. With these developments, AI tools can offer personalized financial advice and automate savings plans by analyzing a complete financial picture. However, strict data protection laws like GDPR ensure that companies must handle this data responsibly - violations can lead to fines of up to $20 million or 4% of global revenue.

Embedded Financial Services in Everyday Apps

Building on open finance, embedded services integrate financial tools directly into everyday apps. This means you might encounter financial options - like instant loans or real-time payouts - while shopping online or using gig-economy platforms. These innovations are powered by Banking-as-a-Service (BaaS) models.

"The biggest structural shift in personal finance technology over the past five years is something most users don't notice: the banking-as-a-service layer underneath the apps they use daily."

- DualMedia

The numbers are staggering: embedded finance transaction volumes are projected to reach $7 trillion by 2026 and could surpass $12 trillion by 2030. Shopify, for example, uses embedded finance to offer working capital loans to merchants, leveraging real-time sales data. By February 2026, Shopify Capital had already provided over $5 billion in cash advances. Uber has also embraced this model, enabling drivers to receive instant payouts rather than waiting for traditional payment cycles.

For consumers, these advancements mean financial tools become almost invisible. You might book a flight and add travel insurance with one click or explore financing options for a major purchase directly within an online marketplace. Automotive marketplace Boatzon has even integrated real-time financing pre-approval into its platform, allowing users to view loan options while browsing inventory.

"The future of fintech isn't about better apps. It's about apps that disappear into your life. The money part? It just works." - Alexis Oliver

To make the most of these tools, consider using traditional banks for complex needs, neobanks for daily transactions, and automation for routine financial tasks. Regularly review your data-sharing permissions to stay in control. These trends highlight how AI is reshaping everything from budgeting to savings and even dispute resolution.

Conclusion

Fintech is reshaping the way we manage personal finances, making it smarter and more efficient. AI-powered tools now handle up to 90% of transaction categorization, giving you a clear picture of your spending habits without lifting a finger. Beyond tracking, modern fintech solutions are actively safeguarding your finances. For instance, DidIBuyIt boasts an 83% success rate in resolving disputes, saving users from the headache of dealing with complex bank policies or paying hefty legal fees. In just five minutes, AI evaluates your case, identifies the best legal arguments using Visa and Mastercard rules, and prepares professional dispute documentation.

"Lawyers charge $400/hour and do exactly what our AI does for free: find the right reason code, draft a dispute letter, and compile your evidence." - DidIBuyIt

AI-powered subscription monitoring is another game-changer, helping Americans uncover forgotten recurring charges that, on average, drain $70 per month. Some tools go a step further by negotiating lower rates on bills like cable or internet, putting more money back into your pocket.

These technologies work together to create a seamless system that not only identifies problems but also improves financial security and efficiency. By redirecting funds from unnecessary charges to investments, fintech tools empower users to make smarter financial choices. With 55% of Americans now relying on AI for financial decision-making as of early 2026, it's clear that fintech is setting a new standard for managing money with less stress and more control.

FAQs

Are AI budgeting apps safe to link to my bank?

AI budgeting apps can be a secure option to connect with your bank - if they adhere to stringent security measures. Many well-known apps implement encryption to safeguard your data, use multi-factor authentication for added protection, and avoid storing your bank passwords altogether. Before using any app, take the time to review its security policies, ensure it doesn’t sell your data, and confirm that user privacy is a top priority. By carefully evaluating these factors, you can confidently leverage AI tools without compromising your financial information.

How does “safe-to-save” decide what I can save?

"Safe-to-save" leverages AI-driven tools to evaluate your income, spending patterns, and overall financial habits. By doing so, it creates personalized and flexible savings goals that align with your financial situation. This approach ensures you can save efficiently without compromising your day-to-day necessities.

What do I need to file a dispute successfully?

To successfully file a dispute, start by collecting clear and detailed evidence related to the charge or issue in question. Many modern processes incorporate AI tools to simplify the process. These tools can detect and classify the dispute type and even draft letters for your review before submission. The key to success lies in providing accurate details and thorough supporting documentation. AI systems can then analyze this information, streamline the resolution process, identify potential issues, and offer helpful insights, making the entire experience smoother and more efficient.