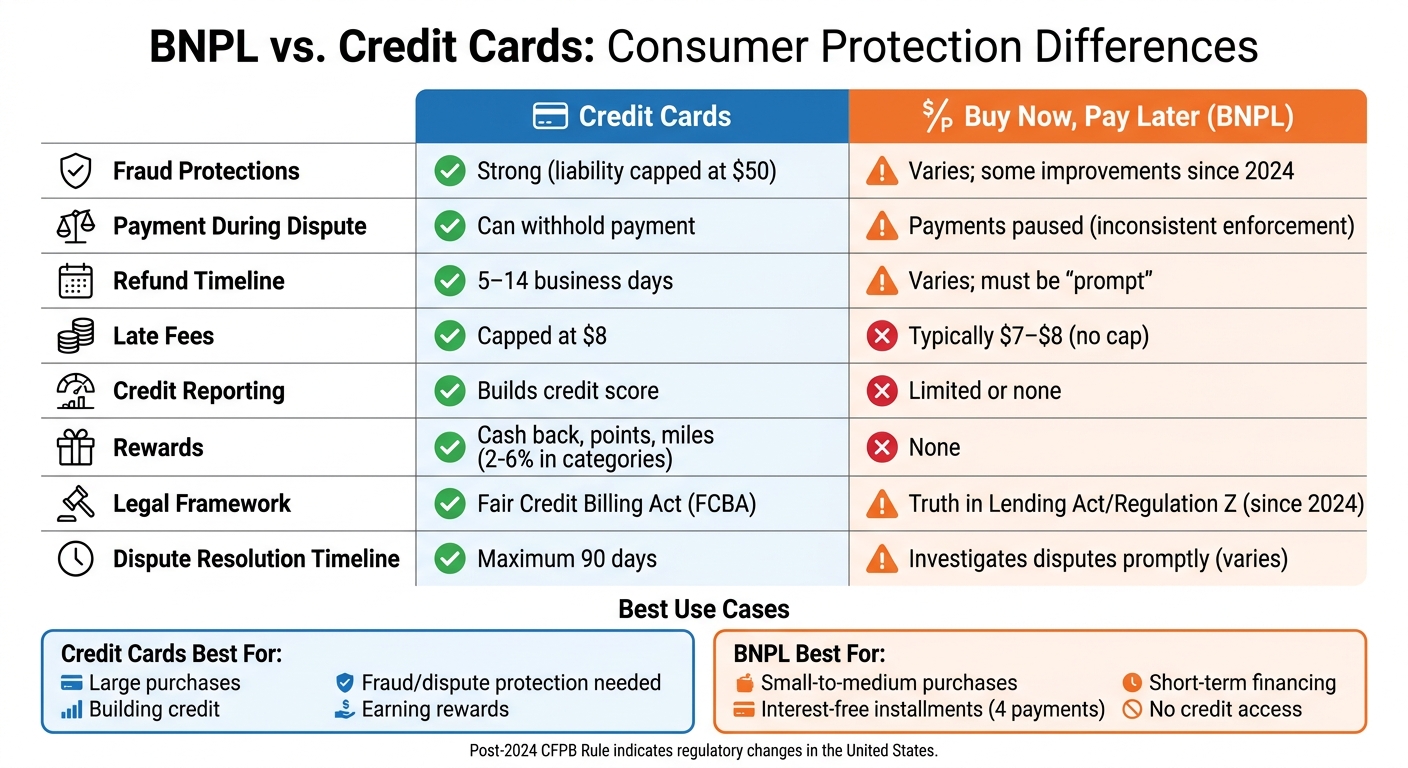

BNPL vs. Credit Cards: Consumer Protection Differences

When should you use Buy Now, Pay Later (BNPL) or credit cards? It depends on your needs. Credit cards offer stronger fraud protections, dispute rights, and rewards, while BNPL can be useful for interest-free, short-term payments. However, BNPL’s protections still lag behind credit cards, even after recent regulatory updates.

Key takeaways:

- Credit Cards: Best for large purchases, building credit, and fraud/dispute protection. Federal laws ensure clear billing, refunds, and fraud liability capped at $50.

- BNPL: Good for small-to-medium purchases with interest-free installments. However, limited credit reporting, higher late fees, and inconsistent protections can be risks.

Quick Comparison Table:

| Feature | Credit Cards | BNPL (Post-2024 Rule) |

|---|---|---|

| Fraud Protections | Strong (liability capped at $50) | Varies; some improvements since 2024 |

| Payment During Dispute | Can withhold payment | Payments paused (inconsistent enforcement) |

| Refund Timeline | 5–14 business days | Varies; must be "prompt" |

| Late Fees | Capped at $8 | Typically $7–$8 (no cap) |

| Credit Reporting | Builds credit score | Limited or none |

| Rewards | Cash back, points, miles | None |

Bottom line: Credit cards provide better protections and perks, while BNPL may suit short-term, smaller purchases if managed carefully.

BNPL vs Credit Cards: Consumer Protection Comparison Chart

Buy Now, Pay Later Apps vs. Credit Cards: The Pros and Cons | WSJ

sbb-itb-5d40823

How Consumer Protections Differ After CFPB Rule Changes

On May 22, 2024, the Consumer Financial Protection Bureau (CFPB) introduced an interpretive rule that redefined how Buy Now, Pay Later (BNPL) services are regulated. Under this rule, BNPL providers are now considered "card issuers" as outlined by the Truth in Lending Act and Regulation Z - the same legal framework that applies to traditional credit cards. This decision specifically impacts "pay-in-4" plans (interest-free installment loans repaid in four or fewer payments), categorizing the digital accounts used for these services as "credit cards."

CFPB Rule Changes Explained

The rule, effective July 30, 2024, imposes credit card-like consumer protections on BNPL providers. For instance, BNPL lenders must now investigate disputes and pause payments during the investigation process, just like credit card companies. If you return a product or cancel a service, the BNPL provider must promptly credit your account instead of continuing to withdraw payments while the merchant processes the return. Additionally, BNPL companies are required to issue periodic billing statements, similar to those provided by credit card issuers.

CFPB Director Rohit Chopra emphasized the importance of these changes, stating:

"Regardless of whether a shopper swipes a credit card or uses Buy Now, Pay Later, they are entitled to important consumer protections under long-standing laws and regulations already on the books" [4].

According to Chopra, the goal was to ensure that BNPL providers do not gain an unfair advantage by bypassing established consumer rights and responsibilities [7]. These adjustments bring BNPL practices closer to credit card standards, but some critical differences remain.

Where BNPL Protections Still Fall Short

While these changes improve certain aspects of BNPL regulations, there are still notable gaps when compared to credit card protections.

One major issue is that BNPL products are not classified as "open-end credit." This means BNPL providers are not required to assess a borrower’s ability to repay the loan before approval. Unlike credit card issuers, BNPL providers are also not subject to the $8 late fee cap mandated by the CARD Act, leaving room for higher penalties.

Another significant shortfall is the lack of mandatory credit reporting. BNPL providers are not required to report customer activity to credit bureaus, which has two major consequences. First, on-time payments do not contribute to building a borrower’s credit history. Second, lenders cannot see a consumer’s total debt load, potentially enabling "loan stacking", where individuals take on multiple BNPL loans without lenders having a full view of their financial obligations.

Klarna, a major BNPL provider, criticized the new rules, stating:

"Trying to regulate BNPL like a credit card is like comparing apples with oranges. ... They operate in fundamentally different ways" [7].

Fraud and Dispute Resolution: BNPL vs. Credit Cards

Fraud Protections for Credit Cards

When it comes to fraud protections, credit cards set a high standard. Federal law limits your liability for unauthorized charges to just $50 [9]. The process for disputes is also clearly outlined. To initiate a dispute, you need to send a written notice to your card issuer's billing inquiry address within 60 days of receiving the statement with the error. Once your issuer receives the notice, they must acknowledge it within 30 days and resolve the issue within two billing cycles, or no more than 90 days [9]. During this time, you're not required to pay the disputed amount, and the issuer cannot take collection actions or report the charge as delinquent. These clear protections make credit cards a reliable option for handling fraud-related issues.

Fraud Protections for BNPL Services

Historically, BNPL services have struggled to offer the same level of fraud protection as credit cards. Consumers often found themselves required to continue making payments even while disputing fraudulent charges [1]. However, a May 2024 ruling by the CFPB brought some changes. The rule reclassified BNPL providers as "card issuers" under the Truth in Lending Act and Regulation Z, requiring them to investigate disputes, pause payment obligations during these investigations, and provide credits for returned items. These updates specifically apply to "pay-in-4" plans, which are interest-free installments paid in four or fewer payments [4][8].

Despite these advancements, enforcement has been inconsistent. By May 2025, reports indicated that the CFPB had stopped enforcing the rule, leading to uneven practices across BNPL providers [3]. While some major companies have voluntarily adopted measures like payment pauses and dispute resolution processes, these policies are not universal [1]. This inconsistency highlights the need to carefully evaluate how each payment method handles fraud before making a choice.

Side-by-Side Comparison: Dispute Resolution

Here’s a quick look at how credit cards and BNPL services stack up when it comes to resolving disputes:

| Feature | Credit Cards | BNPL Services (Pay-in-4) |

|---|---|---|

| Legal Framework | Fair Credit Billing Act (FCBA) [9] | Truth in Lending Act/Regulation Z [4] |

| Fraud Liability | Capped at $50 by law [9] | Varies; 2024 rule aimed to align with credit cards [4] |

| Payment During Dispute | Can withhold payment during investigation [9] | Must pause payments during investigations (enforcement varies) [3] |

| Dispute Reporting Window | 60 days from statement date [9] | 60 days from statement (per new guidelines) [4] |

| Resolution Timeline | Maximum 90 days [9] | Investigates disputes promptly [4] |

Refund and Return Policies: BNPL vs. Credit Cards

How Credit Card Refunds Work

When it comes to credit cards, federal law ensures a straightforward refund process. If you return a faulty product, the merchant typically credits your original card, reducing your balance within 5 to 14 business days [11].

For defective items costing more than $50 and purchased within 100 miles of your home, you may legally withhold payment if the merchant doesn’t resolve the issue [10]. However, keep in mind that any rewards or points earned on the purchase are usually deducted when the refund is processed [11]. Additionally, if you're expecting a refund close to your payment due date, it's a good idea to pay your balance anyway to avoid late fees, as the credit may not appear until the next billing cycle [11].

How BNPL Refunds Work

Refunds for Buy Now, Pay Later (BNPL) services can be trickier because they involve multiple parties - the consumer, the BNPL lender, and the merchant. This often leads to delays, with CFPB Director Rohit Chopra describing the process as “the runaround” [12].

One major issue is that many BNPL users have had to continue making installment payments even after returning an item. In some cases, payments continued until all scheduled installments were completed [12]. In 2021 alone, consumers disputed or returned $1.8 billion in transactions across five major BNPL providers, with more than 13% of all BNPL transactions involving a return or dispute [5][2].

To address these challenges, the May 2024 CFPB rule introduced new requirements. BNPL providers must now investigate disputes, pause payment obligations during the investigation, and ensure refunds are credited to consumer accounts promptly [5][12].

Side-by-Side Comparison: Refund and Return Protections

Here’s a quick comparison of how credit cards and BNPL services handle refunds and returns:

| Feature | Credit Cards | BNPL Services (Post-2024 Rule) |

|---|---|---|

| Refund Timeline | 5–14 business days [11] | Varies; must be "prompt" under new rules [12] |

| Payment During Return | Can withhold payment for defective goods over $50 [10] | Must pause payments during investigation [12] |

| Refund Mechanism | Statement credit to account balance | Credit to installment loan balance |

| Legal Protection | Fair Credit Billing Act / Truth in Lending Act | Truth in Lending Act (Regulation Z) [5][2] |

| Rewards Impact | Points/rewards deducted upon refund [11] | No rewards to lose (most plans are interest-free) [12] |

| Process Complexity | Direct reversal through card issuer | Requires coordination between merchant and lender [12] |

If you're dealing with a return or refund issue, it’s essential to contact the merchant first and keep all relevant documentation, such as shipping receipts, email confirmations, and tracking numbers, to strengthen your case [10][5].

Billing Transparency and Other Differences

After exploring fraud and refund protections, it's clear that billing transparency and extra perks further set credit cards apart from BNPL services.

Credit Card Benefits and Transparency

Credit cards make it easier to track your spending. Every purchase appears on a single monthly statement, giving you a straightforward snapshot of where your money went [13]. Thanks to federal regulations like the Truth in Lending Act and the CARD Act, issuers are required to provide standardized disclosures about interest rates and fees, ensuring you won't encounter unexpected charges.

But the advantages don't stop at transparency. Credit cards often come with rewards that BNPL services simply don't offer. Many cards let you earn cash back, points, or travel miles on your purchases - some even offer up to 2% back on everything or 5% to 6% in select categories [3][16]. On top of that, credit cards often include extended warranties and purchase protection, covering theft or damage for 90 to 120 days [6][16]. For big-ticket items like electronics or appliances, these protections can translate into substantial savings.

"Credit cards make your purchases much easier to keep track of. You can see everything you've bought all in one place... Conversely, each BNPL offer is its own separate loan that you have to keep track of." - WalletHub [13]

BNPL services, on the other hand, come with their own set of challenges and risks.

BNPL Billing and Risks

With BNPL, every purchase functions as an individual installment loan, which means users must juggle multiple payment schedules. In 2022, 63% of BNPL borrowers had several loans running at the same time, and 33% used multiple providers simultaneously [15]. While the CFPB's May 2024 rule now mandates that BNPL providers issue periodic billing statements similar to credit cards [2], the regulatory framework is still a work in progress.

Late fees for BNPL services average $7 to $8 per missed payment [16][3]. While this might seem small, studies indicate that BNPL users incur an average of $176 more annually in overdraft and credit card late fees compared to those who don't use BNPL [6]. The ease of approval for these services can encourage "impulse borrowing", which is particularly concerning given that 71% of BNPL users already carry revolving credit card debt [3].

"BNPL providers are not held to the same regulatory standards as credit card issuers. This means terms can be inconsistent, and penalties for late payment may not be easily understood." - Eden Dombrowa, CorServ [14]

Which Payment Method Should You Choose?

The right payment method depends entirely on your financial situation and what you're buying. There's no one-size-fits-all answer - each option has its strengths based on the context of your purchase.

When to Use Credit Cards

Credit cards shine when you're making high-value purchases, buying items that might need to be returned, or shopping in situations where strong fraud protection is a must. They also help build your credit history and often offer rewards like 2% to 6% cash back in specific categories. For example, if you're purchasing electronics, appliances, or shopping online from lesser-known retailers, credit cards provide the added security of chargeback mechanisms and dispute rights.

If you're planning a big purchase, look for a card with a 0% introductory APR period, which can last anywhere from 15 to 21 months. Additionally, many major issuers like Chase, American Express, and Citi now offer installment plans for purchases over $75 to $100. These plans mimic the structure of Buy Now, Pay Later (BNPL) services but come with the added protections of traditional credit cards.

When BNPL Is a Better Option

Buy Now, Pay Later is ideal for smaller to medium-sized purchases that you can comfortably pay off in four installments. It’s especially useful if you need interest-free financing or don’t have access to traditional credit. Categories like fashion or electronics often fall into this range, with total costs typically under a few hundred dollars - making the structured payments manageable. However, keep in mind that BNPL generally offers limited dispute protections, so it’s not the best choice when consumer safeguards are critical.

To use BNPL wisely, stick to one plan at a time. Statistics show that 60% of BNPL users manage multiple loans simultaneously, and 41% reported missing a payment in 2024. If you already carry credit card debt (a situation seen in 71% of BNPL users), adding BNPL loans could increase your risk of overdraft fees and late charges.

Tips for Making the Right Choice

Your decision should align with the size of the purchase and your financial habits. While both options have their benefits, keeping a few guidelines in mind can help you make the best choice.

- Before using a BNPL service, ensure the provider complies with CFPB regulations on dispute rights and payment pauses.

- Check if the service reports on-time payments to credit bureaus. Many only report missed payments, which can harm your credit without reflecting your positive payment history.

FAQs

Does BNPL protect me if the item never arrives?

Recent regulations have ensured that Buy Now, Pay Later (BNPL) services must provide protections similar to those offered by credit cards. This includes support for dispute resolution and refunds in cases where your item doesn’t arrive or is returned.

It’s important to review the specific terms of your BNPL provider to understand how to file a dispute or request a refund. Each provider may have its own process, so knowing the details can save you time and hassle if an issue arises.

If I return something bought with BNPL, when do payments stop?

When you return an item bought using a Buy Now, Pay Later (BNPL) service, your payments usually stop once the refund is processed by the provider. However, this process can take up to 50 business days. In some cases, you might need to notify the provider - often through their app - to pause payments while the refund is being handled. Be sure to review your BNPL provider's policies for detailed guidance on how to proceed.

Can BNPL hurt my credit score even if it doesn’t build credit?

Yes, Buy Now, Pay Later (BNPL) services can hurt your credit score, even though they typically don't contribute to building it. If you miss payments, some providers may report this to credit bureaus, which could negatively affect your credit history. Additionally, if BNPL services are treated like credit cards under certain rules, they might show up on your credit report. To protect your credit, always pay on time and carefully review the terms and conditions of your BNPL provider.