ATM Skimming: How to Spot a Compromised Machine

ATM skimming is a growing threat where criminals steal your card details and PIN using hidden devices on ATMs. These devices, such as card-reader overlays, deep insert skimmers, and tiny cameras, are designed to blend in with the machine, making them hard to detect. In 2026 alone, over 400 skimmers were removed from ATMs across major U.S. cities, preventing nearly $428 million in losses.

Key Takeaways:

- What to Look For: Loose card readers, raised keypads, mismatched colors, adhesive residue, or tiny holes near the keypad.

- How It Works: Skimmers steal card data while hidden cameras or keypad overlays capture your PIN.

- Where It Happens: Isolated or dimly lit ATMs, especially at gas stations or small shops, are common targets.

- How to Protect Yourself: Use ATMs in secure locations, shield your PIN, inspect machines before use, and monitor your accounts regularly.

If you suspect tampering, cancel your transaction, report it to your bank immediately, and freeze your card to minimize losses. Federal law limits your liability to $50 if you act within two business days. Stay alert and proactive to safeguard your finances.

How to tell if there is debit card skimmer on gas pumps, ATMs

sbb-itb-5d40823

How ATM Skimming Works

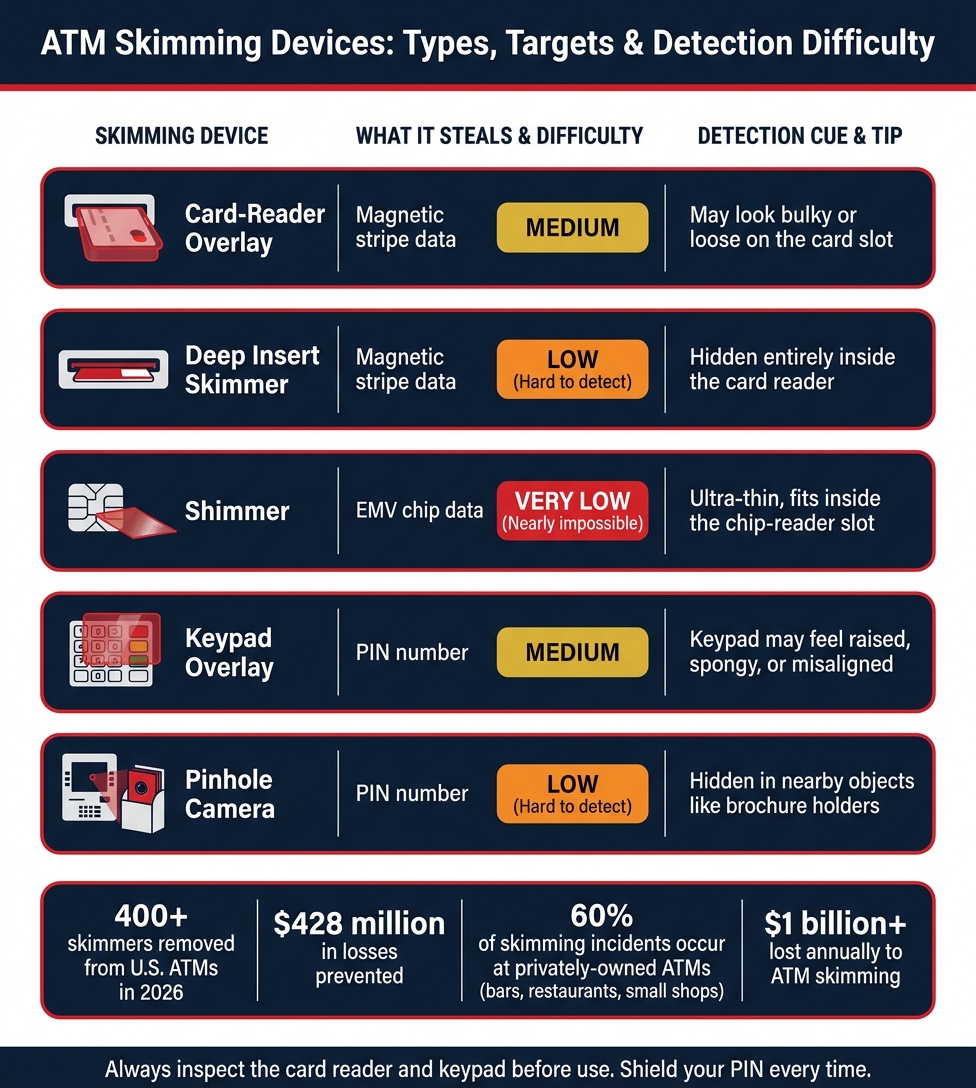

ATM Skimming Devices: Types, Targets & Detection Difficulty

ATM skimming is a two-step crime where criminals steal your card data and PIN separately, then combine the two to access your funds.

Types of Skimming Devices

Different skimming devices are designed to target specific pieces of information. For example, card-reader overlays, also called fake bezels, are plastic shells placed over the ATM’s card slot. When you insert your card, the overlay reads and stores the data from the magnetic stripe. Deep insert skimmers work similarly but are hidden entirely inside the card reader, making them nearly impossible to detect from the outside.

As chip-enabled cards became more common, criminals adapted by using shimmers. These ultra-thin devices are inserted into the chip-reader slot to intercept data from EMV chips, bypassing the added security these chips were meant to provide.

To capture your PIN, thieves use either a keypad overlay, which records keystrokes, or a pinhole camera placed discreetly near the ATM. As Michael Benardo from the FDIC explains:

"If positioned correctly, a brochure holder on an ATM is the perfect place to hide a mini-camera that can record PIN numbers as customers type them." [1]

Here’s a quick look at the most common skimming devices and how easy they are to detect:

| Device Type | What It Steals | How Easy to Spot |

|---|---|---|

| Card-Reader Overlay | Magnetic stripe data | Medium - may look bulky or loose |

| Deep Insert Skimmer | Magnetic stripe data | Low - hidden inside the slot |

| Shimmer | EMV chip data | Very low - fits inside the slot |

| Keypad Overlay | PIN number | Medium - keypad may feel raised |

| Pinhole Camera | PIN number | Low - hidden in nearby objects |

How Skimmers Are Installed and Retrieved

Installing a skimming device is surprisingly quick. Criminals use adhesives like glue or double-sided tape to attach overlays in seconds. These devices are custom-made to match the color, texture, and branding of specific ATM models, making them blend in seamlessly [4][5].

Thieves often target isolated or dimly lit ATMs, such as those in the back of gas stations or hotel lobbies, where they can work unnoticed. However, they also go after high-traffic locations like convenience stores, where people are in a rush and less likely to notice anything unusual [1]. Alarmingly, about 60% of skimming incidents occur at privately-owned ATMs, such as those found in bars, restaurants, and small shops [4].

In the past, criminals had to return to retrieve the devices to access stolen data. Now, many use Bluetooth-enabled skimmers, which transmit stolen card information wirelessly to a nearby phone or laptop [1].

What Criminals Do with Stolen Card Data

Once thieves have your card number and PIN, their next step is typically creating a cloned card - a counterfeit version of your card encoded with the stolen data. This fake card can then be used at ATMs or retail stores just like the original.

Before making large transactions, criminals often run a small test transaction to confirm the stolen card works. If successful, they act quickly, draining accounts through ATM withdrawals, online purchases, or by selling the stolen data to others on the dark web. This practice, known as carding, highlights how short the window can be between theft and fraud. That’s why it’s so important to regularly monitor your accounts and inspect ATMs for signs of tampering.

How to Check an ATM for Tampering

Understanding how skimming devices work is just the beginning. The real challenge is spotting signs of tampering before you use an ATM. A quick inspection can go a long way in protecting your financial information.

Checking the Card Reader and Keypad

Start with a close visual inspection. The card reader should sit snugly against the machine with no gaps, odd bulges, or mismatched colors. Amber Holmes, an FDIC Financial Crimes Information Specialist, explains:

"The best way to determine if an ATM has a false cover is to look for flaws like loose wires, seams that are not flush and slots or keypads that look out of place." [1]

Next, examine the keypad. A legitimate keypad will feel firm and lie flat. If it feels raised, soft, or misaligned, that's a red flag. Also, check for signs like adhesive residue, scratches, or cracked plastic around the card slot - these could indicate recent tampering.

How to Physically Test ATM Components

Beyond just looking, give the ATM a quick physical check. Before inserting your card, gently pull on the card reader. Real ATM components are securely attached, so if the reader moves or feels loose, don’t use that machine.

Similarly, lightly tug at the keypad’s edges. If it feels detached or unstable, it could be a fake overlay. Pay attention to how the card slot feels when inserting your card - unusual resistance or tightness might suggest an internal skimmer.

Here’s a quick reference guide:

| Component | How to Test | Signs of Tampering |

|---|---|---|

| Card Reader | Tug and wiggle the slot | Loose fit, bulky appearance, or unusual resistance when inserting the card |

| Keypad | Pull at the edges | Raised surface, spongy feel, visible glue, or misaligned graphics |

| ATM Housing | Run fingers over the surface | Rough patches, tape residue, or seams that don’t sit flush |

Once you’ve checked the card reader and keypad, take a moment to look for hidden cameras.

Spotting Hidden Cameras Near the Keypad

Skimmers may steal your card data, but criminals also need your PIN. That’s where hidden cameras come in. These tiny devices often blend into the ATM and are easy to overlook.

Pay special attention to areas above the keypad and along the sides of the machine. Brochure holders are another common hiding spot. Michael Benardo, Manager of the FDIC’s Cyber Fraud and Financial Crimes Section, advises:

"Also check for tiny holes in the ATM housing or in something else that looks like it was hastily stuck onto the ATM to cover a small camera." [1]

Look for attachments that seem out of place - different textures, colors, or alignment can be giveaways. If something doesn’t feel right, trust your instincts. And always shield the keypad with your free hand while entering your PIN. It’s one of the simplest and most effective ways to block a camera’s view.

How to Lower Your Risk of ATM Skimming

Spotting a tampered ATM is a great first step, but it’s just one layer of protection. To further reduce your chances of falling victim to ATM skimming, it’s essential to develop smart habits in your everyday banking activities. These small changes can go a long way in keeping your money and information safe.

Choosing Safer ATMs and Payment Methods

Where you withdraw money matters. ATMs located inside bank lobbies or branches are much less likely to be tampered with than those in isolated spots like gas stations or convenience stores. Michael Benardo, Manager of the FDIC's Cyber Fraud and Financial Crimes Section, explains:

"ATMs in secluded locations are more likely to be altered." [1]

If you can, avoid standalone ATMs in quiet areas. Additionally, consider using mobile wallets like Apple Pay or Google Pay for payments. These methods rely on tokenization vs. encryption to protect data, using unique codes instead of card numbers. This makes it nearly impossible for skimming devices to steal useful information.

Keeping Your PIN Private

A simple but effective habit is covering the keypad with your free hand while entering your PIN. This prevents hidden cameras from capturing your code and discourages anyone nearby from peeking. Even if the ATM looks fine, it’s a good practice to follow every single time.

Don’t fall for myths like entering your PIN in reverse to alert authorities - it doesn’t work. Instead, focus on keeping your PIN private and secure.

Another proactive step is contacting your bank to lower your daily withdrawal limit. While this won’t stop a skimmer from stealing your data, it can limit the amount of money they can access before you notice the issue.

Finally, make it a habit to monitor your accounts regularly. This is one of the best ways to catch fraudulent activity early.

Keeping an Eye on Your Accounts

The sooner you catch fraud, the less you stand to lose. According to the Electronic Funds Transfer Act (EFTA), if you report unauthorized debit transactions within two business days, your liability is capped at $50. Wait longer, and you could be on the hook for up to $500 or more [1].

To stay ahead, enable real-time transaction alerts through your bank’s app. Amber Holmes, an FDIC Financial Crimes Information Specialist, points out:

"Thieves might make low-dollar withdrawals or charges as a way to test a counterfeit debit or credit card before they use it for big-dollar transactions." [1]

What to Do If You Suspect ATM Skimming

If you think an ATM has been tampered with, it's crucial to act quickly. Taking immediate steps can help protect your finances and minimize potential losses.

Canceling the Transaction Right Away

If you notice anything suspicious - like a loose card reader, an unusually thick keypad, or adhesive around the card slot - cancel the transaction immediately. Press "Cancel", retrieve your card (if possible), and leave the machine. Avoid touching or interacting with any part of the device that seems altered. Report the issue to the ATM operator using the contact number displayed on the machine. If you're inside a store or bank branch, notify an employee right away. You can also file a report with your local police using their non-emergency line, as this report could be useful during your bank's investigation. After leaving the ATM, contact your bank to report the situation.

Reporting the Incident to Your Bank

Once you're away from the ATM, call your bank right away to freeze your card and request a replacement. Acting quickly ensures you stay within the legal timeframe for limiting your liability.

Under the Electronic Fund Transfer Act (EFTA), reporting the issue within two business days caps your liability at $50. If you wait longer than 60 days, you could be responsible for the full amount of any fraudulent transactions [1][2].

When contacting your bank, be prepared with key details: the ATM's location, the date and time of your visit, and a list of any suspicious or unauthorized transactions, no matter how small. As Amber Holmes, a Financial Crimes Information Specialist at the FDIC, points out:

"Thieves might make low-dollar withdrawals or charges as a way to test a counterfeit debit or credit card before they use it for big-dollar transactions." [1]

These small charges are intentional and should always be flagged. Once your card is frozen, you can start disputing any unauthorized transactions.

Disputing Fraudulent Charges with DidIBuyIt

After freezing your card, use DidIBuyIt to create a solid dispute case. This platform leverages AI to draft professional dispute letters that reference your legal rights under laws like the EFTA. It also helps organize supporting documents, such as your police report and communication with the bank, while tracking the progress of your case in real time. By keeping everything organized, DidIBuyIt simplifies the process of disputing fraudulent charges and ensures your case is as strong as possible.

Conclusion: How to Stay Protected from ATM Skimming

ATM skimming results in over $1 billion in losses for financial institutions and consumers every year [3]. However, by building a few smart habits, you can significantly reduce the risk of falling victim to these schemes.

Before using an ATM, take a moment to inspect it. Look for signs like mismatched colors, bulky attachments, glue residue around the card slot, or anything that seems off. Check that the card reader and keypad are securely attached. Whenever possible, stick to ATMs in well-lit, secure locations. Better yet, consider using mobile wallets with contactless payment options. These use tokenization, which bypasses the vulnerabilities targeted by skimming devices [5].

If you suspect tampering, cancel your transaction immediately and leave the ATM. Amber Holmes, a Financial Crimes Information Specialist at the FDIC, offers this advice:

"Be suspicious if your card doesn't easily go into the machine or if the card reader appears loose, crooked or damaged, or if you notice scratches, glue, adhesive tape or other possible signs of tampering." [1]

Acting quickly is key if you detect tampering. The Electronic Fund Transfer Act (EFTA) limits your liability to $50, as long as you report the issue to your bank within two business days [1]. Tools like DidIBuyIt can simplify this process by generating dispute letters, organizing your documents, and tracking your case in real time. Staying alert and responding swiftly can help protect your account and minimize the damage caused by ATM skimming.

FAQs

Can skimmers steal data from chip (EMV) cards too?

Skimmers are primarily designed to capture data from the magnetic stripe on cards. They can't directly access the information stored on chip-enabled cards (EMV cards). This is because EMV cards rely on encryption and generate dynamic data for each transaction, making them far more difficult to clone or exploit.

What should I do if the ATM kept my card and I suspect skimming?

If an ATM holds onto your card and you suspect foul play like skimming, stop using the machine right away and reach out to your bank or card issuer immediately. Avoid trying to retrieve the card on your own, as this could expose you to additional fraud risks. Instead, follow the steps your bank provides, which might include visiting a branch or calling their customer service line. After reporting the issue, keep a close eye on your account for any unauthorized charges or transactions.

How fast can thieves use skimmed card data after I use an ATM?

Thieves can exploit skimmed card data almost instantly after your ATM transaction if a skimming device is in place. These devices are designed to quickly grab your card details and PIN, giving criminals the ability to access your account right away. To safeguard your information, always check ATMs for signs of tampering. Look for things like loose or wobbly card slots and strange keypad overlays before using the machine. Staying alert can make all the difference.