How Digital Payments Are Changing Consumer Behavior in 2026

Digital payments are transforming how people pay and shop in 2026. Here's what you need to know:

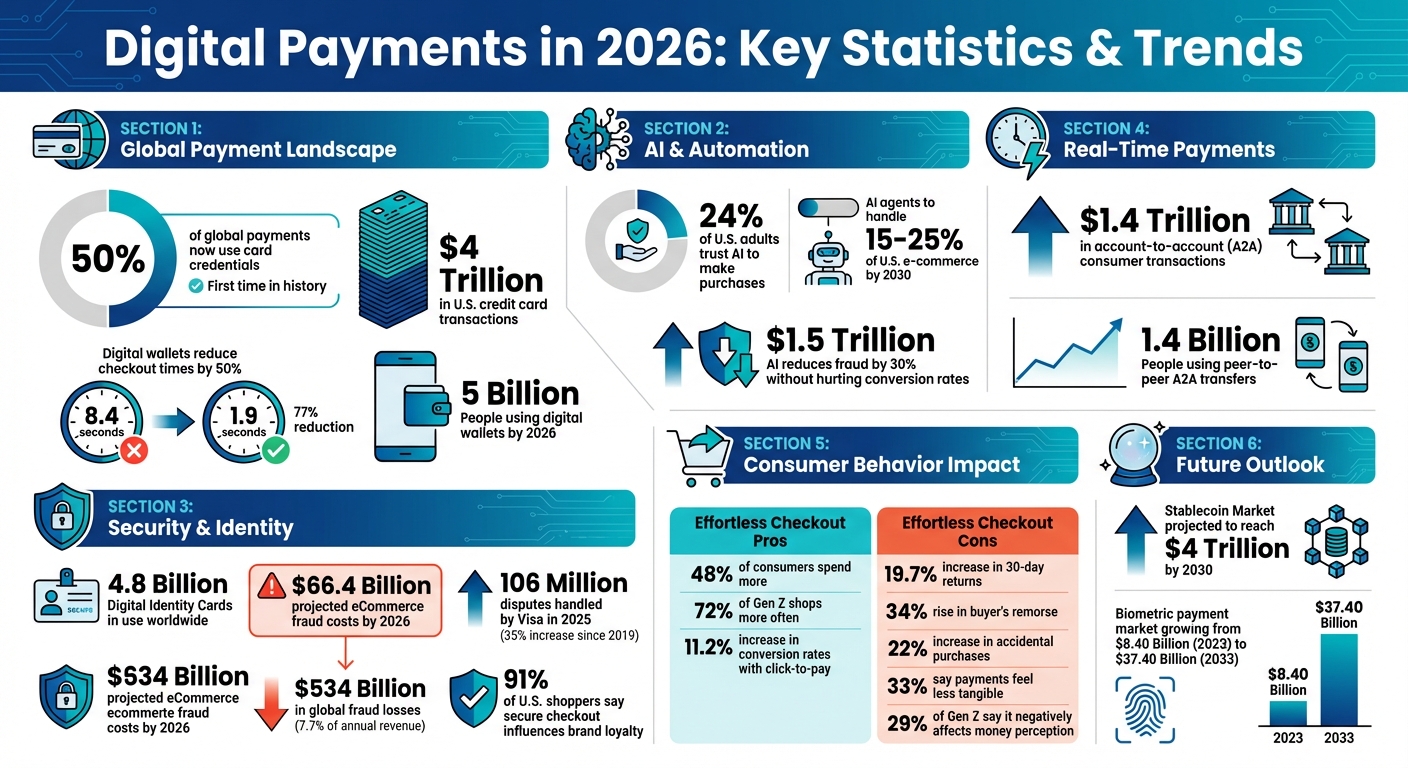

- Convenience and Speed: Half of all global payments now use card credentials, with U.S. credit card transactions surpassing $4 trillion. Digital wallets cut checkout times by 50%.

- AI and Automation: AI tools can now make purchases for users, but only 24% of U.S. adults trust them fully.

- Biometric Security: Fingerprint and facial recognition are common, with 4.8 billion digital identity cards in use worldwide. Advanced fraud detection protects against rising deepfake threats.

- Real-Time Tracking: Account-to-account payments hit $1.4 trillion, offering instant updates on spending.

- Impact on Spending Habits: Faster checkouts increase impulse buying but also lead to higher return rates and buyer’s remorse.

The rapid evolution of payment technology is reshaping consumer habits, emphasizing the need for secure, fast, and user-friendly systems.

Digital Payment Statistics and Consumer Behavior Trends 2026

How Modern Consumer Habits Are Transforming Global Payments

sbb-itb-5d40823

Major Trends Changing How Consumers Pay

The way people handle payments is evolving rapidly, driven by advancements in technology that are reshaping the relationship between consumers and their money. By 2026, three key trends are expected to redefine payment behaviors in the U.S.

AI-Powered Payment Tools

AI is stepping up from just offering recommendations to actually making purchases for consumers. Known as agentic commerce, this approach allows AI tools to handle tasks like searching, comparing, and completing transactions automatically. Users can set specific rules for these agents, such as spending limits, approved merchants, or time constraints. For instance, someone might program their AI with a rule like:

Yes, if the bill is below $100; No, if it is above.

This enables faster, more efficient transactions without needing manual approval every time. But trust remains a hurdle - only 24% of U.S. online adults are comfortable letting AI handle routine purchases as of 2025. Building confidence in these systems will be crucial for broader adoption. While AI simplifies transactions, biometric methods are making them more secure.

Biometric Authentication for Secure Payments

Fingerprint and facial recognition have become go-to payment methods, with 4.8 billion people expected to have digital identity cards by 2026. These technologies eliminate the need for physical cards or PINs, speeding up transactions and enhancing security through unique biometric data. However, as these systems grow, so do the threats. Oliver Jenkyn, Group President at Visa, cautioned:

2026 will, unfortunately, see a material increase in the sophistication and volume of these AI powered identity attacks.

To combat these risks, advanced measures like 3D depth sensing and skin texture analysis ensure that the person making the payment is real, not a deepfake or synthetic identity. Tokenization adds another layer of protection by replacing raw biometric data with encrypted tokens, so even if a breach occurs, sensitive information remains safe. While these innovations secure individual transactions, another trend is transforming how consumers manage their money.

Real-Time Transaction Tracking

Instant access to account balances and spending details has become the norm. Account-to-account (A2A) transactions are expected to hit $1.4 trillion in consumer value by 2026, with about 1.4 billion people using peer-to-peer A2A transfers. This real-time connectivity allows users to see exactly where their money is going as transactions happen. The adoption of the ISO 20022 data standard adds even more value by offering richer transaction details, making it easier to reconcile accounts and detect fraud. Consumers can also set personalized payment rules, like using credit for large purchases and debit for everyday expenses. As Vicki Hyman, Director of Global Communications at Mastercard, pointed out:

You can automate commerce, but you can't automate trust.

Real-time tracking is helping to build that trust, especially as payments become more seamless and integrated into everyday apps.

How Payment Technology Affects Buying Decisions

Payment technology is no longer just about convenience - it's actively shaping how and why people make purchases. With advancements like AI and biometric security, these innovations are streamlining checkouts and influencing consumer behavior in unexpected ways.

How Easy Payments Lead to Faster Purchases

Click-to-pay technology has transformed the checkout process, cutting the median time from 8.4 seconds down to just 1.9 seconds - a massive 77% reduction. By simplifying multiple steps into one quick action, this technology has made shopping faster and more seamless. Unsurprisingly, 48% of consumers admit to spending more when the checkout process is effortless.

Tiffany Johnson, Chief Product Officer at NMI, summed it up perfectly:

If you're not making it an easier experience, then consumers are just going to go elsewhere... From the merchant side, it's table stakes if you want to keep the clicks and the eyes.

But this speed comes with a cost. A study across 43,000 stores revealed that while click-to-pay boosted conversion rates by 11.2%, it also led to a 19.7% increase in 30-day return rates. The simplified process often bypasses moments where consumers might reconsider their purchases, leading to a 34% rise in buyer’s remorse and a 22% uptick in accidental purchases.

The impact is particularly noticeable among Gen Z shoppers. A whopping 72% of them shop more often when frictionless payment options are available. However, 29% say these experiences have negatively affected their perception of money, and 33% of all consumers admit that digital payments make spending feel less tangible, sometimes leading to overspending.

While speed is crucial for driving sales, it’s clear that balancing it with thoughtful design is essential to avoid unintended consequences.

How Better Security Builds Consumer Trust

As payment systems get faster, ensuring security becomes even more critical. Consumers want to know that speed doesn’t come at the expense of safety. In fact, 91% of U.S. shoppers say a smooth and secure checkout experience directly influences their likelihood of returning to a brand.

AI is playing a big role in this area, reducing fraud by 30% without hurting conversion rates. This is especially important as global eCommerce fraud is expected to cost merchants a staggering $66.4 billion by 2026. Paul Fabara, Chief Risk and Client Services Officer at Visa, noted:

In 2026, the combination of real-time intelligence, AI-driven detection, global collaboration, and shared identity-protection capabilities will define the next frontier of safety in commerce.

Still, many shoppers remain cautious about fully autonomous systems. Only 24% of U.S. online adults trust AI to handle routine purchases on their behalf. To bridge this trust gap, biometric authentication methods - like liveness checks and deepfake detection - are becoming essential. They offer a balance between speed and protection, addressing concerns about increasingly sophisticated fraud techniques.

Brands that can deliver both hassle-free experiences and strong security measures have a clear advantage in winning consumer loyalty.

AI-Powered Dispute Resolution and Consumer Confidence

As digital payments evolve, dispute resolution has become essential for maintaining consumer trust. With payments happening faster than ever, resolving disputes efficiently is no longer just a back-office task - it’s a front-line priority. To illustrate the scale of the challenge, Visa handled 106 million disputes globally in 2025, marking a 35% increase since 2019. This surge highlights the growing demand for transparency and swift resolutions when consumers face unrecognized charges or errors. Nobody wants to spend hours on phone calls or wade through endless paperwork to resolve a problem.

AI is stepping in to make dispute resolution smoother and more consumer-friendly. Sam Abadir, Research Director at IDC Financial Insights, summed it up perfectly:

Dispute management is moving from a back-office function to a strategic priority, driven by rising volumes, regulatory scrutiny, and growing pressure to protect customer experience.

By automating processes like dispute classification and predicting outcomes, AI allows consumers to file claims in minutes instead of hours. These advancements not only speed up resolutions but also enhance the overall payment experience.

How DidIBuyIt Simplifies Disputed Transactions

DidIBuyIt has reimagined the dispute process with AI, turning what used to be a complicated ordeal into a quick, efficient solution. The platform’s AI-powered wizard can classify disputes in under 3 minutes, analyzing merchant data and transaction details to create a tailored recovery strategy. It generates a "battle plan" that includes a reason code, an evidence checklist, and bank-ready PDF documentation.

The results speak for themselves: DidIBuyIt boasts an 83% win rate and has recovered more than $18 million for customers across 284,000 disputes. Filing a claim takes an average of under 5 minutes, and banks typically resolve cases within 10–30 business days, often issuing provisional credit within 5–10 days.

One of the platform’s standout features is its ability to navigate complex regulations. Its AI assesses bank policies, Visa/Mastercard network rules, and merchant terms to ensure filings comply with financial standards. Even when merchants claim "no refunds", card network rules often override such policies in cases like non-delivery or billing errors.

DidIBuyIt also maintains a searchable database of over 50,000 transaction descriptors, helping consumers identify unfamiliar charges before filing a dispute. This proactive feature reduces confusion and prevents unnecessary claims. It’s also effective in addressing "friendly fraud", where consumers mistakenly dispute legitimate charges.

DidIBuyIt Plans: Basic Recovery vs. Advanced Support

To cater to different needs, DidIBuyIt offers two service tiers:

| Feature | Basic Recovery | Advanced Support (AI Wizard) |

|---|---|---|

| Cost | Free | Paid/Premium |

| Database Access | Access to 50,000+ merchant descriptors | Full access with personalized analysis |

| Documentation | General bank guides and advice | Professional, ready-to-file PDF documents |

| Strategy | Self-guided | AI-generated "Battle Plan" and scripts |

| Evidence | Manual collection | AI-powered evidence checklist and reason codes |

| Speed | Variable | Under 5 minutes to generate filing |

| Win Probability | Not included | Included |

The Basic Recovery plan is perfect for those who want free access to the descriptor database and general guidance. It’s a solid option for identifying charges and exploring initial steps. On the other hand, the Advanced Support plan takes things to the next level with the AI wizard. It automates case analysis, generates professional documentation, and even provides scripts for bank interactions. This plan eliminates much of the hassle and guesswork that often accompanies disputes.

It’s worth noting that filing a chargeback through DidIBuyIt won’t impact your credit score. Chargebacks are a consumer protection mechanism, not a credit-related event.

How to Use New Payment Methods Effectively

Building on earlier discussions about AI-driven security, here are some practical tips to help you make the most of biometric tools and real-time monitoring to secure your financial transactions.

Using Biometric and AI Tools for Better Security

Biometric authentication and real-time transaction monitoring can protect your finances while making purchases more convenient. However, not all biometric systems are equally secure. The biometric payment market is expected to grow significantly, from $8.40 billion in 2023 to $37.40 billion by 2033. To maximize security, opt for payment apps that store biometric data directly on your device's secure chip instead of centralized servers.

When setting up biometric payments, enable features like liveness detection, which requires actions such as blinking or head movements to ensure authenticity. Paul Fabara, Visa's Chief Risk and Client Services Officer, highlighted the growing sophistication of fraud attempts:

The fight for identity is entering a new AI-driven era... criminals are moving upstream, using deepfakes, synthetic identities, and hyper-realistic impersonation to seize control of a consumer's entire identity.

For added protection, use digital wallets that tokenize your card data. Christine Hurtubise, Vice President of AI and Machine Learning at FIS, explained how this works:

Tokens that are assigned for Apple Pay wallets, for example, require authorization that recognize your face.

This combination of biometrics and tokenization provides a streamlined yet secure payment experience. To further enhance security, set up multiple biometric markers like fingerprints and facial recognition. Also, keep your device updated to access the latest AI-driven liveness detection features, which counter evolving spoofing techniques. Interestingly, nearly 33% of Millennials believe biometrics improve security, compared to less than 25% of Gen X.

While biometrics strengthen authentication, real-time monitoring adds another layer of defense.

Using Real-Time Monitoring to Control Your Finances

Real-time monitoring works alongside biometric security by identifying unusual activity based on your spending patterns, login locations, and device usage. This proactive approach can help you detect fraud before it becomes a major issue. For context, global fraud losses in 2025 are projected to reach $534 billion, representing 7.7% of annual revenue for companies worldwide.

Enable instant transaction notifications to catch unauthorized charges immediately. Be extra cautious during high-risk times like tax season or the holidays, when scammers often target consumers with deceptive offers. Paul Fabara emphasized the importance of speed in fraud prevention:

Speed is now one of the most powerful tools in global fraud prevention.

If you’re using AI shopping assistants - which could be adopted by 81% of consumers by 2026 - set strict spending rules. For instance, you might program limits such as "Approved for dining and travel, Declined for healthcare" or "Declined for purchases over $100". Oliver Jenkyn, Group President at Visa, described this functionality:

Now your agent can shop for you by asking: 'What would Oliver choose if faced with these purchase options?'

Pair real-time monitoring with tools like multi-factor authentication (MFA) and encryption for added protection. Be ready for AI systems to request extra verification if a transaction looks unusual - this step-up authentication is designed to safeguard your account. Additionally, reviewing your transaction history manually can help identify subtle irregularities that automated systems might overlook. On the convenience side, digital wallets can cut mobile checkout times in half compared to manual entry, ensuring these security measures don’t feel like a hassle.

What's Next for Digital Payments

Moving Toward Easier Payment Experiences

The days of manual checkout are fading fast, giving way to a future where payments are completely seamless. Here's a groundbreaking shift to keep in mind: by 2026, half of all consumer payments worldwide will be made using card credentials instead of cash - a historic first.

AI is also stepping up its game. Shopping agents powered by artificial intelligence are evolving from merely offering recommendations to autonomous purchasing. By 2030, these agents are expected to handle 15% to 25% of all e-commerce purchases in the U.S.. Globally, this "agentic commerce" could drive $1.5 trillion in spending. To stay ahead, merchants need to ensure their digital platforms are ready for this shift by implementing machine-readable data and API-first checkout systems.

On another front, stablecoins are moving from speculative investments to regulated payment tools. Thanks to the U.S. GENIUS Act of 2025, the global stablecoin market could grow to $4 trillion by 2030. These digital currencies offer faster, more affordable options for cross-border payments. Deloitte highlights their broader significance:

Stablecoins are not just a cheaper cross-border instrument; they reflect a broader shift toward programmable, real-time settlement embedded directly into commercial activity.

Together, these developments signal a future where both consumers and businesses must adapt quickly to thrive in an ever-changing payment ecosystem.

Key Takeaways for Consumers and Businesses

Digital payments are reshaping how we think about security, identity, and financial control. By 2026, it's estimated that 5 billion people will use digital wallets, while 4.8 billion will hold digital identity cards. This makes tools like biometrics and real-time monitoring essential for combating increasingly sophisticated fraud.

For consumers, these advancements mean faster checkouts, stronger fraud defenses, and shopping experiences tailored to their preferences. For businesses, the stakes are higher than ever. Success will depend on how quickly and effectively they can adopt these cutting-edge payment technologies. As Zachary Aron, Global and U.S. Payments Leader at Deloitte, explains:

Competitive advantage will come from how quickly, intelligently, and responsibly leaders activate these capabilities to deliver differentiated value.

The payment landscape of 2026 will reward those who embrace innovation and adapt to these sweeping changes.

FAQs

How do I set safe spending rules for an AI shopping agent?

Managing an AI shopping agent responsibly means putting safeguards in place to keep spending under control. Here’s how you can do it:

- Set Clear Spending Limits: Define caps for each transaction or a specific timeframe. For example, you might limit the agent to $100 per purchase or $500 per month.

- Authorize Trusted Agents: Only allow agents with secure verification methods to handle transactions. This could include multi-factor authentication or encrypted credentials.

- Restrict Purchases to Approved Categories: Ensure the AI is limited to buying items from pre-approved categories, like household supplies or office equipment, to prevent unintended purchases.

- Enable Real-Time Monitoring: Keep an eye on transactions as they happen. This allows you to quickly detect and address any unauthorized activity.

- Create Dispute and Error Protocols: Have a plan in place for resolving issues, whether it’s a mistaken purchase or a billing error.

By following these steps, you can maintain control over AI-driven transactions while minimizing risks.

Are biometric payments safe against deepfakes and spoofing?

Biometric payments are increasingly vulnerable to threats like deepfakes and synthetic media, which can easily exploit older systems. Alarmingly, recent estimates reveal that 1 in 5 biometric fraud attempts now involve deepfakes. To stay ahead of these evolving risks, payment systems must prioritize adopting advanced technologies that can effectively identify and block these sophisticated attacks.

What should I do first if I see a charge I don’t recognize?

If you spot a charge that seems unfamiliar, the first step is to dispute it using AI-powered tools. These tools are built to make the process easier by identifying questionable charges early and offering explanations to address the issue promptly.

For cases of suspected unauthorized activity, reach out to your bank or payment provider right away. They can help report the charge and kick off a dispute process to resolve the matter quickly.