Why Faster Payments Don't Always Mean Better Fraud Protection

Real-time payment systems like RTP and FedNow have made transferring money faster and more convenient, processing transactions in seconds rather than days. By early 2026, these systems connected thousands of financial institutions and handled millions of payments monthly. However, the speed of these services introduces new fraud risks:

- Irrevocable Transactions: Payments settle instantly, leaving no time to reverse fraudulent transfers.

- Fraud Detection Challenges: Traditional fraud systems can’t keep up with the speed of real-time payments, making it harder to identify scams before funds are withdrawn.

- Increased Fraud Cases: Scammers exploit the 24/7 availability of these systems, especially during weekends and holidays when banks are less staffed. Fraud losses from scams like Business Email Compromise (BEC) and Authorized Push Payment (APP) fraud are rising sharply.

To combat these risks, financial institutions are turning to AI-powered tools for faster fraud detection and prevention. These systems analyze transaction data in milliseconds, reducing false positives while improving fraud prevention. For consumers and businesses, using multi-layered security measures and monitoring transactions in real time are crucial steps to staying protected. Platforms like DidIBuyIt also simplify dispute resolution when fraud occurs, offering tools to recover funds efficiently.

While faster payments are convenient, balancing speed with effective fraud prevention is key to ensuring secure transactions.

The SUMMIT Series: Shaping the future of fraud in real time payments

sbb-itb-5d40823

Fraud Cases in Real-Time Payment Systems

Real-world examples reveal how quickly criminals take advantage of the speed offered by instant payment systems. Below, we explore two detailed cases - one involving RTP systems and another focusing on FedNow - to highlight the risks tied to real-time settlements.

Case Study: Fraud in RTP Transactions

In March 2025, Meridian Financial Services, based in Chicago, faced a shocking attack that exposed the weaknesses in real-time payment systems. Fraudsters managed to steal $847,000 in just eight seconds by targeting 23 compromised business accounts. They used a combination of automated credential stuffing - where stolen usernames and passwords were repeatedly tested - and SIM-swapping to bypass multi-factor authentication. While the victims were located in Chicago, the fraudulent transactions originated from residential IP addresses in Lagos, Nigeria.

Meridian’s fraud detection system at the time relied on batch processing, which grouped transactions for analysis rather than evaluating them in real-time. By the time the system flagged suspicious activity, the stolen funds had already been withdrawn from 47 cash-out locations. In response to this incident, Meridian adopted a real-time IP verification system, which led to a significant reduction in their annual fraud losses - from $4.7 million to $312,000.

"Traditional fraud models were too slow for instant settlement... verification systems have milliseconds, not hours, to make risk decisions."

- Meridian Financial Services

This case illustrates how legacy fraud detection tools struggle to keep up with the rapid pace of instant payments, leaving institutions vulnerable to sophisticated attacks.

Case Study: Scams in FedNow Transactions

The challenges faced by FedNow transactions echo similar concerns about the vulnerabilities of instant payments. Fraud in these systems has become a growing issue, with Authorized Push Payment (APP) fraud - where victims are tricked into willingly sending money to fraudsters - causing $8.3 billion in losses in 2024. This number is expected to climb to $14.9 billion by 2028. One of the most prevalent forms of APP fraud is Business Email Compromise (BEC), which alone resulted in $3.05 billion in losses in 2025, up from $2.9 billion in 2023. In these scams, criminals impersonate executives or vendors through fake emails, persuading employees to authorize instant transfers to fraudulent accounts.

What makes these scams especially damaging is the irreversible nature of both FedNow and RTP transactions. By the time victims realize they’ve been duped, the funds are often withdrawn within minutes, leaving little to no chance of recovery. Michael Moon, from Strategic Market Development at iPiD, highlights the issue: "The acceleration [of APP fraud] is driven by instant payment systems that eliminate the time buffer fraud detection systems once relied on".

These examples make one thing clear: the speed and efficiency of real-time payments demand equally fast and effective fraud prevention measures. Without them, businesses and individuals remain at significant risk.

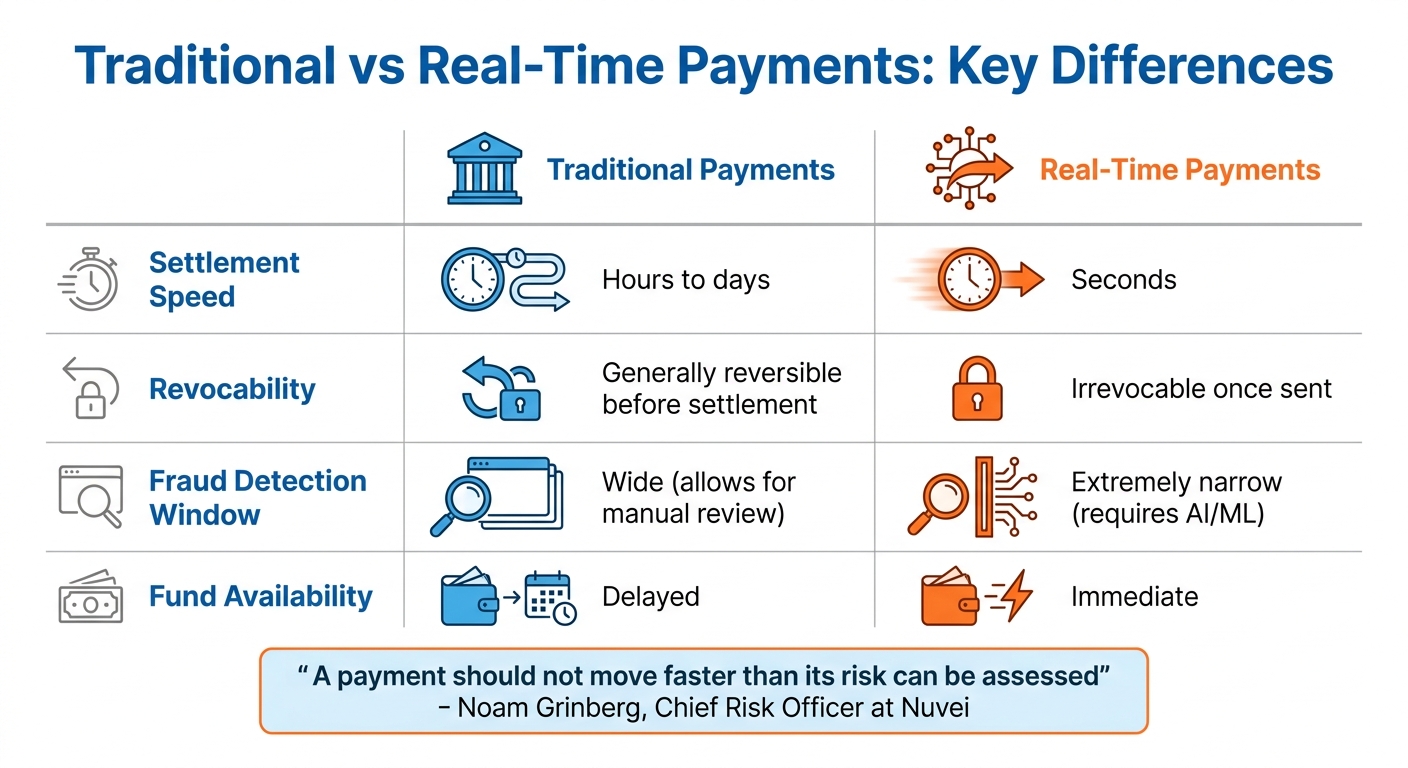

Why Speed Reduces Fraud Detection

Traditional vs Real-Time Payments: Fraud Detection Comparison

Real-time payments have introduced a new challenge: fraud detection must now happen in mere milliseconds. As Noam Grinberg, Chief Risk Officer at Nuvei, aptly states:

"A payment should not move faster than its risk can be assessed".

This highlights the core issue: faster payments demand lightning-fast fraud analysis, leaving little room for error or intervention.

Less Time for Fraud Analysis

In the past, fraud detection systems relied on a buffer period - the time between when a transaction was initiated and when it settled. This delay gave banks the chance to flag, investigate, or verify anything suspicious. However, with real-time payments, that buffer is gone. Decisions that used to take minutes or hours must now be made instantly.

Traditional systems, which often rely on pre-set rules, struggle to keep up with this pace. Meanwhile, fraudsters have embraced AI, using it to scale attacks like social engineering and creating synthetic identities at a speed traditional systems can't match. The result? Institutions now have fewer opportunities to intervene and stop fraudulent transactions before they’re completed.

Difficulty Reversing Transactions

The challenges don't stop at detection. Real-time payments also complicate the process of reversing fraudulent transactions. Since funds settle instantly, fraudsters can withdraw the money almost immediately, leaving little to no time for recovery. Unlike older systems, where a delay in settlement acted as a safety net, real-time payments offer no such protection.

Adding to the risk is the shift to "push" payment models, where the payer initiates and controls the transfer. This makes these systems particularly vulnerable to Authorized Push Payment (APP) fraud, where victims are tricked into sending money directly to criminals. Alarmingly, 36% of financial institutions report uncertainty about how to handle refund requests for cases of authorized fraud.

| Feature | Traditional Payments | Real-Time Payments |

|---|---|---|

| Settlement Speed | Hours to days | Seconds |

| Revocability | Generally reversible before settlement | Irrevocable once sent |

| Fraud Detection Window | Wide (allows for manual review) | Extremely narrow (requires AI/ML) |

| Fund Availability | Delayed | Immediate |

Real-time payments may bring convenience, but they also demand a new level of vigilance and innovation in fraud prevention.

AI-Powered Solutions for Fraud Protection

With the rise of real-time payments, the need for instant fraud detection and quick dispute resolution has become more critical than ever. Artificial intelligence (AI) has taken center stage in combating fraud, analyzing massive amounts of data - like spending habits, geolocation, device details, and IP addresses - in just milliseconds. Unlike older systems that rely on fixed "if/then" rules, AI continuously evolves to counter new threats, including deepfakes and synthetic identities.

Today, 94% of organizations use AI and machine learning to assess fraud risks based on transaction patterns. Moreover, 83% of industry leaders report that AI has significantly reduced false positives and improved customer retention. Companies that have utilized AI for over five years save, on average, $4.3 million annually in lost revenue - nearly double the savings of those newer to the technology. Noam Grinberg, Chief Risk Officer at Nuvei, succinctly explains:

"Intelligence is no longer an overlay to fraud systems. It is what determines their effectiveness".

For example, in February 2026, Citi teamed up with iPiD to expand "Citi Verify", a tool designed to validate payee information before transactions occur. This ensures account details match, lowering the risk of misdirected payments in an environment where instant settlements make recovery nearly impossible. Similarly, American Express improved fraud detection by 6% using advanced AI models like long short-term memory (LSTM), while PayPal boosted its real-time fraud detection capabilities by 10% through continuously learning AI systems.

How AI Improves Fraud Detection

AI integrates directly into the transaction process, making fraud decisions in real time as payments are authorized - essential for the speed required by instant settlement systems. It evaluates behavioral biometrics, such as keystroke patterns, device interactions, and transaction speed, while also monitoring negative lists and user behavior to verify identities without disrupting the payment flow.

This technology is not only quick but also scalable, handling high transaction volumes while minimizing false positives - cutting them by up to 83%. Additionally, 80% of organizations report that AI has reduced the need for manual reviews, allowing fraud teams to focus on complex cases.

While AI strengthens fraud prevention, it also plays a crucial role in resolving fraud when it does occur.

DidIBuyIt: A Solution for Dispute Resolution

Even with advanced fraud prevention, some fraudulent transactions slip through the cracks. That’s where DidIBuyIt comes in - a platform powered by AI to simplify the dispute resolution process. It provides users with tools to create professional, bank-compliant documents, along with step-by-step guidance for resolving chargebacks and refund claims across major networks like Visa, Mastercard, Amex, and PayPal.

DidIBuyIt handles the often-confusing world of dispute documentation with encrypted data management, 24/7 customer support, and real-time tracking of dispute outcomes. This service empowers users - whether individuals or businesses - to resolve disputes efficiently, without needing legal expertise or spending hours navigating bank requirements.

DidIBuyIt Plans Comparison

| Feature | Basic Recovery Plan | Advanced Support Plan |

|---|---|---|

| AI Dispute Analysis | ✓ | ✓ |

| Bank-Ready Documents | ✓ | ✓ |

| Step-by-Step Guidance | ✓ | ✓ |

| Priority Support | – | ✓ |

| Advanced Evidence Prep | – | ✓ |

Both plans offer flat-rate pricing and support for all major payment platforms. The Advanced Support Plan is ideal for more complex disputes, including high-value transactions or sophisticated fraud cases, offering priority assistance and enhanced evidence preparation.

Best Practices for Secure Faster Payments

Securing transactions in real-time payment systems is no small task. It demands a multi-layered approach - relying on one security measure simply isn’t enough. With faster payments being irrevocable, the focus must be on prevention. Once funds are transferred, recovering them is often impossible.

Use Multi-Layered Security Measures

A strong defense starts with layering multiple security techniques. For instance, identity verification during onboarding can weed out synthetic identities early on. Then, risk-based authentication - like multi-factor authentication - kicks in when something seems off. Add in tools like behavioral biometrics and data tokenization, and you’ve got a recipe for safer transactions. Sara Seguin, Global Head of Product Marketing and Strategic Advisory at Alloy, puts it well:

"Friction-right banking is about adding the right security layer at the right time. It's not about removing all friction but implementing smart, targeted steps to protect customers without unnecessarily slowing down transactions".

Behavioral biometrics, for example, can detect unauthorized users by analyzing things like typing patterns, mouse movements, or how someone handles their device - even if they’re using valid credentials. This matters because 75% of consumers say they’d switch financial institutions if they felt security measures were lacking. The message is clear: strong security isn’t just about protection - it’s also a business priority. These foundational steps pave the way for real-time monitoring.

Monitor Transactions in Real-Time

Once layered protections are in place, constant vigilance is key. Real-time payments mean real-time risks, so monitoring systems must work fast. Modern tools use real-time interdiction, pausing suspicious transactions instantly for review. This approach compresses fraud detection into the short window before a transaction is finalized.

With real-time payment volumes increasing by over 50% year-on-year in 2025, the time to catch fraud has become razor-thin. Quick action is no longer optional - it’s essential.

Use AI Tools for Better Protection

To bolster real-time monitoring, AI tools step in as a powerful ally. These systems analyze transaction patterns, device details, and behavioral cues in milliseconds, making them indispensable for fraud prevention.

For those who do encounter fraud, platforms like DidIBuyIt simplify the recovery process. Using AI, they generate bank-compliant documentation and guide users through chargebacks across major payment networks. And with 57% of consumers prioritizing improved fraud detection from their banks, it’s clear that combining AI-powered prevention with effective dispute resolution is the way forward. Together, these tools create a robust defense strategy for the fast-paced world of real-time payments.

Conclusion: Balancing Speed and Security

Real-time payments have transformed how money moves, but speed without proper safeguards can lead to serious issues. As Noam Grinberg, Chief Risk Officer at Nuvei, wisely states:

"A payment should not move faster than its risk can be assessed".

The financial sector has already faced $12 billion in operational losses from over 20,000 cyberattacks in the past two decades. This underscores the need for smarter defenses to keep up with the rapid pace of modern payment systems.

The answer isn’t to slow down payments - it’s to ensure fraud detection moves just as quickly. Thanks to AI-powered systems, fraud can now be identified almost instantly, enabling real-time protection without compromising convenience. Organizations that have embraced AI tools for over five years report nearly double the cost savings compared to recent adopters, highlighting the long-term value of these technologies.

For those navigating payment disputes, DidIBuyIt provides a practical solution by simplifying the recovery process. Combining prevention with efficient dispute resolution isn’t just a good idea - it’s a necessity in today’s fast-moving financial landscape.

FAQs

Why are real-time payments so hard to reverse?

Real-time payments are challenging to reverse because their speed leaves almost no room to catch fraudulent activity. These transactions are completed in mere seconds, eliminating the chance for manual reviews or intervention before the money is transferred. While this quick processing boosts efficiency, it also creates a higher risk for fraud.

What fraud types increase most with instant payments?

Fraud types that see the biggest rise with instant payments include scams and unauthorized transactions. The speed of these payments creates a smaller window for identifying and halting fraudulent activity, which makes traditional fraud prevention techniques less effective. This happens because the rapid transfer of funds limits the time available for intervention and verification before the money changes hands.

What should I do immediately after sending money to a scammer?

If you’ve fallen victim to a scam and sent money, it’s crucial to act fast. Reach out to your bank or payment service provider right away to attempt to halt or recover the transaction. Be sure to report the scam to law enforcement or the appropriate authorities to help launch an investigation. Since many payment methods process quickly, time is of the essence. Keep a close eye on your accounts for any unusual activity and maintain detailed records of all communications related to the incident.