The True Cost of Payment Fraud for Online Businesses

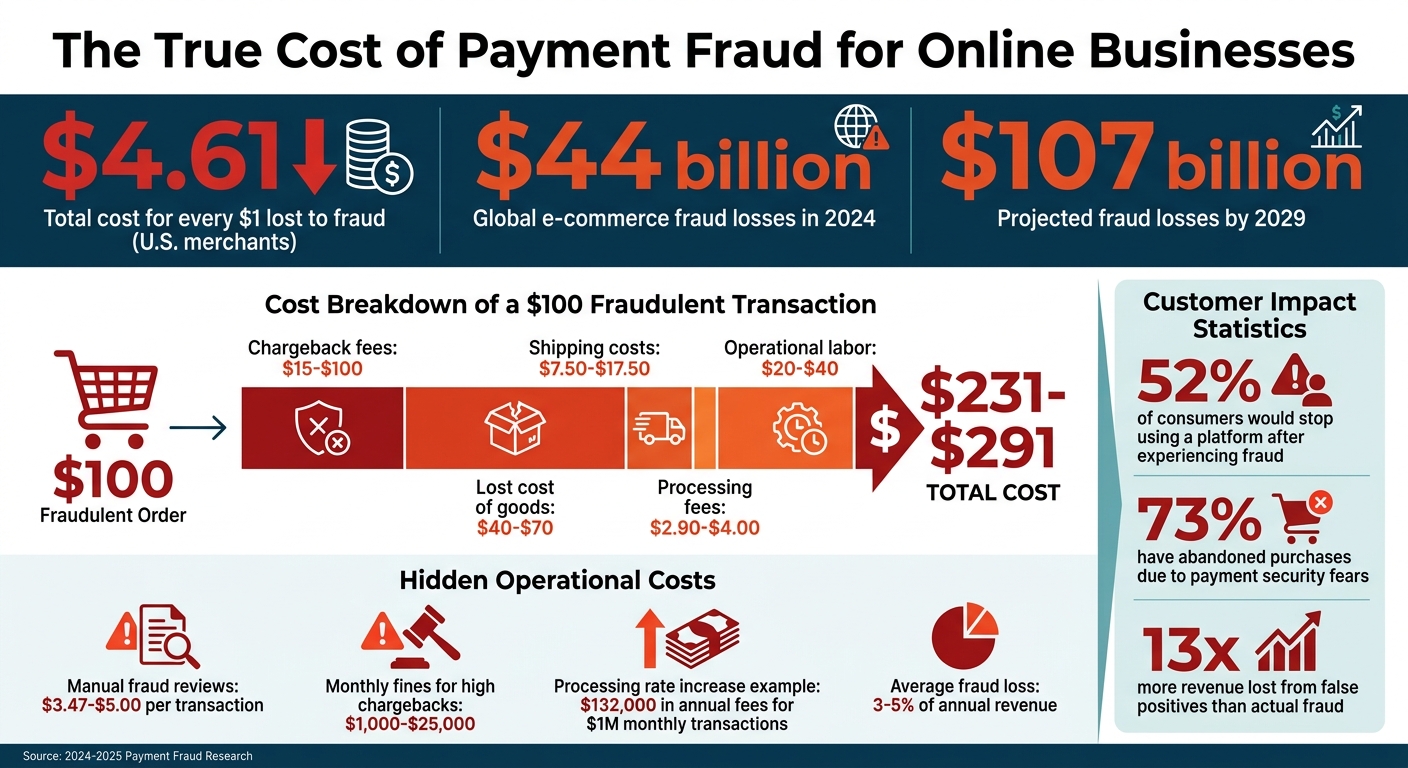

Payment fraud is draining online businesses more than you might think. For every $1 lost to fraud, U.S. merchants spend an extra $4.61 on fees, labor, and indirect costs. Global e-commerce fraud losses hit $44 billion in 2024 and are expected to skyrocket to $107 billion by 2029. Fraudsters are getting smarter, using AI to exploit businesses at every stage of the customer journey - from account creation to post-purchase.

Here’s what you need to know:

- Financial Impact: A $100 fraudulent transaction can cost businesses up to $291 after chargebacks, shipping, and operational expenses.

- Customer Trust: 52% of consumers would stop using a platform after experiencing fraud. False positives - blocking legitimate customers - can cause 13x more losses than the fraud itself.

- Hidden Costs: Manual fraud reviews cost $3.47–$5.00 per transaction, and high chargeback ratios can lead to monthly fines up to $25,000 or even blacklisting from payment processors.

- Prevention Tools: Advanced methods like device fingerprinting, real-time risk scoring, and machine learning can reduce fraud and false positives while protecting your revenue.

Fraud isn’t just about stolen money - it’s about lost trust, operational inefficiencies, and shrinking profit margins. Businesses must invest in multi-layered fraud prevention strategies to stay ahead.

The True Cost of Payment Fraud: Financial Impact Breakdown for Online Businesses

The Financial Impact of Payment Fraud

Direct Costs Breakdown

When a $100 fraudulent order occurs, the financial damage extends far beyond just the lost sale. Here’s how the costs add up:

- Non-refundable chargeback fees: These range from $15 to $100.

- Lost cost of goods: Typically between $40 and $70.

- Unrecoverable shipping costs: Anywhere from $7.50 to $17.50.

- Processing fees: An additional $2.90 to $4.00.

- Operational labor costs: Estimated at $20 to $40.

Altogether, a single fraudulent $100 transaction can cost a business between $231 and $291.

It doesn’t stop there. If a merchant’s chargeback ratio exceeds 0.9% to 1.5% of total transactions, they may face enrollment in monitoring programs such as Visa VAMP or Mastercard ECP. These programs impose monthly fines ranging from $1,000 to over $25,000. On top of that, high fraud rates can result in increased processing fees for all transactions. For example, a merchant handling $1 million in monthly transactions could see their processing rate jump from 2.4% to 3.5%, adding $132,000 in annual fees.

To put this into perspective, global chargeback losses alone reached $33.8 billion in 2025. These direct costs slice directly into profit margins, leaving businesses with less room to maneuver.

How Fraud Reduces Profit Margins

On average, fraud eats up 3% of annual revenue, and in high-risk markets, this figure can climb to 5%. For many businesses, this level of loss matches - or even exceeds - their entire net profit margin, making growth nearly impossible. Cal Weston, an expert in credit card dispute resolution, highlights the severity of the issue:

"The true cost of a single chargeback is typically 2 to 3 times the original transaction amount".

Small businesses often bear the brunt of these losses. About 63% of them report increased customer churn as a result of fraud, which further reduces future revenue streams. The financial strain doesn’t end with lost sales, though. Banks may impose reserve requirements, holding back 5% to 10% of daily sales in non-interest-bearing accounts for up to a year if chargeback ratios spike. This restriction can severely impact cash flow.

In the worst-case scenario, excessive chargebacks can land a merchant on the MATCH list, effectively barring them from mainstream payment processing for five years. These cascading challenges - lost revenue, reserve requirements, and operational penalties - amplify the financial risks for online businesses. As Maanas Godugunur, Senior Director of Fraud and Identity at LexisNexis Risk Solutions, puts it:

"Rising fraud costs strain businesses financially and damage customer trust".

sbb-itb-5d40823

Operational and Reputational Costs of Fraud

The Operational Burden of Managing Fraud

Fraud doesn’t just drain money - it also drains time and energy from your team. Right now, 44% of merchant organizations still rely heavily on manual fraud prevention processes. This means employees are stuck reviewing suspicious transactions by hand. And resolving just one dispute can take 40–60 minutes. That’s time spent gathering receipts, shipping confirmations, and device data - time that could be better spent focusing on growing the business.

The costs pile up quickly. For every $1 lost to fraud, U.S. merchants face a total cost of $4.61 when you factor in investigation expenses, dispute management, and customer support efforts - a figure that’s jumped 37% in just five years. Teams across engineering and customer service are forced to shift their focus from innovation to managing security rules, moderating tools, and responding to complaints about scams, phishing, and account takeovers. Fraud now touches every stage of the customer journey, requiring constant monitoring at every step.

But here’s the kicker: overly aggressive fraud prevention can backfire. 59% of U.S. merchants report that fraud measures increase customer churn. False positives - when legitimate customers are flagged as fraud risks - can drive shoppers away for good. These customers abandon their carts, and many don’t come back. This not only disrupts operations but also damages customer confidence, creating a ripple effect that can harm your reputation. The operational challenges of fraud management are deeply tied to the reputational risks it brings.

How Fraud Erodes Customer Trust

Fraud doesn’t just hurt your bottom line - it can also destroy your brand’s reputation. In fact, the reputational damage often outweighs the immediate financial loss. Consider this: 52% of consumers say they would stop using a platform entirely after experiencing fraud, and 21% would never shop again at a retailer where they were victims of fraud. This isn’t just about losing one sale - it’s about losing the lifetime value of a customer.

Fraud also changes how people shop. 73% of consumers have abandoned an online purchase due to fears about payment security, and 41% are now more cautious when shopping online because fraud tactics have become more sophisticated. The damage doesn’t stop with individual customers. 61% of ecommerce brands have faced negative media coverage after fraud incidents, and 40% of businesses report that fraud directly harms their brand image. For publicly traded companies, the stakes are even higher - 20% say fraud incidents negatively affect their stock price.

Martin Sweeney, CEO of Ravelin, puts it into perspective:

"A company's reputation means everything and must be protected as if it's a matter of life and death – from a business perspective, that's exactly what it is."

Perhaps the most troubling consequence of fraud is the lasting impact on smaller retailers. After experiencing fraud, 20% of consumers shift their spending to larger, more established brands. This creates what some call a “trust tax,” where smaller businesses face higher customer acquisition costs and lower customer lifetime value. The result? A double hit that makes it even harder for these companies to grow and compete. Fraud, in short, doesn’t just steal money - it steals trust, time, and opportunity.

Fraud Detection and Prevention Tools

Common Fraud Detection Technologies

Choosing the right fraud detection tools can be the deciding factor between stopping fraud in its tracks or losing thousands of dollars. While no single tool can catch every fraudulent attempt, combining multiple technologies creates a stronger defense.

Start with the basics. Tools like Address Verification Service (AVS) and CVV checks validate billing addresses and security codes against issuer records, ensuring the cardholder is legitimate. Adding 3D Secure 2.0 introduces an extra authentication step, shifting liability to the card issuer.

As fraudsters grow more advanced, detection systems need to keep pace. Device fingerprinting and behavioral biometrics work together to create unique user profiles by analyzing hardware, software, and user interactions - like browser settings or mouse movements - to differentiate real customers from bots. Velocity checks monitor the frequency of transactions from the same IP, email, or device, flagging suspicious patterns such as "card testing" attacks.

Modern systems rely on real-time risk scoring, powered by machine learning, to analyze dozens of data points in milliseconds - often in under 100ms. This allows transactions to be approved, blocked, or flagged before completion. For example, in May 2025, skincare brand Paula's Choice transitioned from a rules-based system to a machine learning model. Within three days, they saved over $100,000 in fraudulent orders, reduced their chargeback rate by 0.2%, and achieved a sixfold return on investment.

Advanced platforms also use model orchestration, running multiple detection methods simultaneously. Rules engines catch known patterns, supervised machine learning identifies statistical anomalies, graph networks uncover fraud rings, and sequential transformers recognize long-range behavioral trends. As Accertify notes:

"A platform that runs a sequential transformer while deprecating its rules engine is leaving fraud on the table".

This layered approach is critical, especially when 98% of merchants reported experiencing fraud in 2024. By leveraging diverse tools, businesses can build a robust, multi-layered fraud prevention strategy.

Using Multiple Fraud Prevention Methods

To effectively combat fraud, integrating various methods throughout the transaction process is essential. Merchants who use 12 or more data signals per transaction detect 3.4 times more fraud than those relying solely on basic tools like AVS and CVV. Additionally, combining velocity checks with behavioral scoring can reduce false positives from 8.2% to 2.1%.

A strong defense covers every stage of the customer journey. This includes device fingerprinting and IP reputation checks before a transaction, payment validation and real-time risk scoring during the transaction, and order verification and chargeback monitoring afterward.

Automated workflows streamline the process by auto-approving low-risk transactions, triggering step-up authentication for medium-risk orders, and declining high-risk attempts. This ensures that human reviewers focus on only about 13% of orders. For instance, in 2025, Harry's - a personal care brand - reduced its chargeback rate by 85% in just two months. Using a machine learning platform, its one-person fraud team identified bulk resellers creating fake accounts to purchase razor blades.

Automated fraud detection isn’t just faster; it’s also more effective. It can reduce chargebacks by 62% compared to manual review processes. But the goal isn’t just about blocking fraud - it’s about approving legitimate transactions with precision. Overly strict measures can backfire, costing businesses an extra $30 in lost sales for every dollar lost to fraud. A well-balanced, layered approach protects your business while keeping genuine customers happy.

Best Payment Stack for Reducing False Declines

How to Minimize Fraud Throughout the Transaction Process

Fraud prevention is an ongoing effort that spans every stage of the transaction process. Considering that online fraud is expected to cost e-commerce merchants $48 billion globally in 2025 and could climb past $56 billion by 2026, taking a structured, multi-stage approach is essential. By combining advanced detection tools with strategies tailored to each phase - before, during, and after the transaction - you can build a stronger defense against fraud.

Before the Transaction: Prevention Measures

The best way to deal with fraud is to stop it before it even starts. Identity verification and Know Your Customer (KYC) protocols act as the first line of defense, ensuring that the individuals creating accounts or placing orders are legitimate. For high-value purchases, requiring government-issued ID uploads or biometric facial recognition adds an extra layer of protection.

Start gathering data early. Tools like device fingerprinting, IP geolocation, and email reputation checks are effective at identifying risky users before they reach your checkout page. For instance, device fingerprinting alone can detect 34% of fraud attempts that bypass standard AVS and CVV checks, and when combined with email and IP checks, this figure jumps to 78%.

Certain tactics can significantly lower your fraud risk. For example, flagging email addresses created within 48 hours of a purchase can help catch disposable accounts often used for fraud. Setting velocity limits - which restrict the number of transactions from a single card, device, or IP address within 24 hours - can block suspicious activity. Additionally, tools like CAPTCHA and account creation monitoring help stop bots from testing stolen cards or setting up fake accounts.

Implement 3D Secure 2.0 selectively to shift liability for high-risk transactions, while ensuring low-risk customers don’t face unnecessary friction. Finally, clear return, refund, and shipping policies can help reduce "friendly fraud", which is responsible for a staggering 60% to 80% of all chargebacks.

During the Transaction: Real-Time Monitoring

Even with strong preventative measures, real-time monitoring during the transaction is critical. Modern systems use real-time risk scoring, analyzing hundreds of data points in under 100 milliseconds to assign a risk score between 0 and 100. Based on this score, orders can be automatically approved, flagged for additional verification (like 3D Secure or SMS codes), or declined outright.

Advanced techniques like behavioral analysis and velocity checks are key to catching sophisticated fraud attempts. For instance, systems can detect bot activity by analyzing non-human behaviors such as linear mouse movements or unusual typing patterns. Velocity checks, meanwhile, flag rapid transactions from the same IP or device.

Striking the right balance between security and customer experience is crucial. Merchants lose 13 times more revenue to legitimate orders that are wrongly declined than to actual fraud. By reserving step-up verification for medium-risk transactions, you can safeguard your business without alienating customers. Before rolling out new fraud rules, test them against 90 days of historical data to ensure false positives remain below 3%.

After the Transaction: Monitoring and Recovery

Fraud doesn’t always show up immediately, making post-transaction strategies just as important. Tools for chargeback monitoring and root cause analysis allow you to identify patterns and refine your defenses. Categorizing chargebacks - whether they stem from true fraud, friendly fraud, or merchant error - helps pinpoint underlying issues.

Automating dispute responses can make a huge difference. Merchants using automated tools achieve a 67% win rate in disputes, compared to just 32% for manual processes. Systems that compile key transaction data - like device fingerprints, IP logs, shipping confirmations, and customer communication - save time and strengthen your case. Connecting to chargeback alert networks such as Ethoca or Verifi CDRN also allows you to issue refunds before disputes escalate, avoiding fees that range from $20 to $100 per transaction.

Once fraud is confirmed, update blocklists with associated data like device fingerprints, email addresses, and shipping details to prevent repeat offenses. This creates a feedback loop that enhances the accuracy of machine learning models over time. Keep in mind that 40% of customers who successfully file one fraudulent chargeback will attempt another within 90 days.

Simple operational adjustments can also help. For example, optimizing your billing descriptor so that your company name is easily recognizable on credit card statements can reduce disputes caused by unrecognized charges - an issue behind 15% of friendly fraud cases. Additionally, providing clear order confirmations and proactive shipping updates can cut "item not received" disputes by up to 45%.

Creating a Fraud Prevention Plan for Your Business

Fraud prevention isn't a one-and-done task - it's an ongoing effort that demands thoughtful planning, consistent updates, and smart resource allocation. With 98% of merchants reporting fraud incidents in the past year and global companies projected to lose 7.7% of annual revenue to fraud by 2025, having a clear and flexible strategy is critical. The goal is to build a plan that addresses your business's specific risks while staying agile enough to adapt as fraud tactics evolve.

Identifying Your Fraud Risks

The first step is understanding the types of fraud that threaten your business. Common risks include card-not-present (CNP) fraud for e-commerce, account takeovers (ATO) for loyalty programs, refund abuse for industries like apparel or electronics, and promo abuse in sectors like iGaming or quick-service restaurants.

Take a close look at your business's sales channels - websites, mobile apps, and marketplaces - and assess the unique vulnerabilities of each. Map out your entire customer journey, from account creation to checkout and post-transaction activities, to pinpoint where authentication gaps might exist.

For industry-specific risks, focus on patterns unique to your field. For example, travel merchants should monitor for "impossible routes", while iGaming platforms should flag "same device/multiple accounts" scenarios. Establish a clear risk tolerance by analyzing historical data and setting quantifiable limits. Keep in mind that false positives, where legitimate orders are mistakenly declined, can cost up to 75 times more than actual fraud due to lost customer lifetime value.

Once you've mapped out the risks, you can move on to allocating your budget effectively.

Allocating Your Fraud Prevention Budget

When budgeting for fraud prevention, think beyond the value of stolen goods. Fraud comes with hidden costs like chargeback fees, shipping expenses, and operational labor. For perspective, industry benchmarks recommend allocating 0.5% to 1.2% of total revenue to fraud prevention tools.

One key area to prioritize is reducing false declines. For every $1 lost to fraud, overly strict prevention measures can cost up to $30 in legitimate sales. Manual reviews, which average $3.47 per transaction, should be reserved for high-value or complex cases, while automated systems handle 80–90% of decisions. AI-powered fraud detection tools can deliver a return on investment of 15x to 29x by minimizing false declines and recovering revenue.

Layer your defenses with multiple tools, including basic verification methods like AVS/CVV, device and behavioral intelligence, and machine learning scoring. Target specific performance metrics, such as keeping chargeback rates below 0.5% and achieving an auto-approval rate of at least 80%. Regularly audit declined orders, and if more than 6% turn out to be legitimate, adjust your thresholds to avoid unnecessary losses.

With a solid budget in place, the next step is to ensure your fraud prevention measures stay effective over time.

Monitoring and Updating Your Strategy

Fraud tactics evolve quickly - every six to eight weeks, in fact - so regular updates are essential. Merchants who update their fraud rules monthly see 43% fewer successful fraud attempts compared to those who update quarterly. Top-performing businesses maintain false positive rates below 2%, well under the industry average of 5.5%.

Set up feedback loops to analyze fraud losses, false positives, and customer disputes. Test new fraud rules in "shadow mode" for at least two weeks before enforcing them to avoid blocking legitimate transactions. Maintain multiple fraud detection models simultaneously, as older models may still catch specific fraud types.

Track key metrics regularly and adjust thresholds as needed:

| Monitoring Metric | Target | Review Frequency | Action if Off-Target |

|---|---|---|---|

| Chargeback Rate | Below 0.5% | Weekly | Tighten high-risk thresholds |

| False Positive Rate | Below 3% | Weekly | Loosen mid-range thresholds |

| Manual Review Rate | Below 15% | Monthly | Add rules for common patterns |

| ML Model Accuracy | Above 93% | Monthly | Retrain on recent data |

Categorize chargebacks weekly by root cause - true fraud, friendly fraud, or merchant error - to identify areas needing improvement. Retrain machine learning models quarterly using the latest 90 days of data to maintain accuracy above 93%. Conduct annual "red team" exercises, where internal teams simulate fraud attempts to uncover and fix vulnerabilities within 30 days.

"The strongest strategies assume fraud tactics will change and build processes to test, adjust, and deploy updates without disruption." - Stripe

Conclusion

Key Takeaways for Online Merchants

Payment fraud doesn’t just chip away at profits - it multiplies losses significantly. On average, U.S. merchants lose $4.61 for every $1 of fraud they experience. A seemingly small $100 fraudulent transaction can balloon into a cost of $231 to $291 when you include chargeback fees, shipping, manual reviews, and wasted acquisition expenses. Globally, e-commerce fraud losses are expected to soar to around $107 billion by 2029. These numbers highlight just how critical it is to understand the hidden costs of fraud.

Beyond direct financial losses, fraud creates operational headaches. For instance, manual reviews alone cost merchants between $3.47 and $5.00 per transaction. Strict fraud controls can also backfire - 59% of U.S. merchants say these measures hurt customer conversion rates, and 52% of consumers admit they’d leave a platform after experiencing fraud. To make matters worse, excessive chargebacks can lead to hefty fines ranging from $1,000 to $75,000 per month, or even land a business on the MATCH list, which effectively ends its ability to process credit card payments.

The solution? A layered defense strategy that combines prevention and recovery. Tools like device fingerprinting and behavioral biometrics can block fraud before it happens, while recovery strategies such as chargeback representment help reclaim revenue lost to friendly fraud - a problem responsible for 45% to 80% of merchant chargebacks. Merchants who actively contest disputes often see win rates of 50–70%.

Next Steps to Protect Your Business

Start by calculating the true cost of fraud for your business. Use this formula:

Total Cost = Direct Losses + Fees + Manual Review + Tooling + Compliance + False Positives + Reputation + Opportunity Cost.

This breakdown helps you identify exactly where your money is going, so you can focus your fraud prevention efforts where they’ll have the most impact.

Next, evaluate your current fraud prevention tools. If you’re still relying on static rules or outdated manual processes, you could be losing more than you think. Consider implementing multi-factor authentication (MFA) - a critical step, as 99% of successful account takeovers occur when MFA isn’t in place. Strengthen your defenses with AI-driven detection systems that adapt in real time. These systems analyze combined signals, which are 20 times more effective than relying on isolated data points. To further reduce chargebacks, set up alerts through services like Ethoca or Verifi. These alerts can intercept disputes early, preventing 20–40% of chargebacks.

If chargebacks are already a challenge, consider tools like DidIBuyIt. This platform automates dispute management with AI-powered analysis, generates professional documentation for banks, and offers step-by-step guidance to resolve disputes efficiently. By automating this process, you can turn a time-consuming task into a streamlined recovery strategy.

Staying ahead of fraud requires proactive measures, but the payoff is clear: better protection for your business and your bottom line.

FAQs

How do I calculate my business’s true cost of fraud?

When calculating the real cost of fraud for your business, it’s essential to look beyond the obvious losses. Fraud doesn’t just hit your bottom line directly - it also brings a range of hidden expenses that can add up quickly. Here's a breakdown:

- Direct losses: These are the immediate hits, like stolen funds, chargebacks, fraudulent payouts, and lost goods.

- Indirect costs: Think of the ripple effects - chargeback fees, the expense of monitoring and prevention measures, reduced conversion rates, and even losing loyal customers.

- Reputational damage: Perhaps the hardest to quantify, this includes the erosion of customer trust and the potential long-term impact on future revenue.

For North American e-commerce businesses, the numbers are staggering. For every $1.00 lost to fraud, the total cost balloons to about $3.00 when you factor in all these elements. That’s a hefty price tag for any business.

What’s a safe chargeback rate to avoid fines or being blacklisted?

A chargeback rate of less than 1% is typically seen as a safe zone, helping businesses avoid fines or restrictions on their accounts. Exceeding this threshold can result in penalties or even being blacklisted, which can seriously impact your operations and damage your reputation. Keeping the rate low is essential to safeguard your business.

How can I reduce false declines without letting more fraud through?

To keep fraud in check while reducing false declines, it's essential to use advanced fraud detection tools. Techniques like real-time transaction scoring and AI-driven systems can accurately detect over 95% of fraudulent activity while keeping false positives to a minimum.

On top of that, fine-tuning your authorization processes can make a big difference. By approving legitimate transactions that might otherwise be flagged incorrectly, businesses can recover lost sales. Striking this balance not only strengthens fraud prevention but also ensures a smoother and more positive customer experience.