Payment Security Best Practices for E-Commerce Businesses

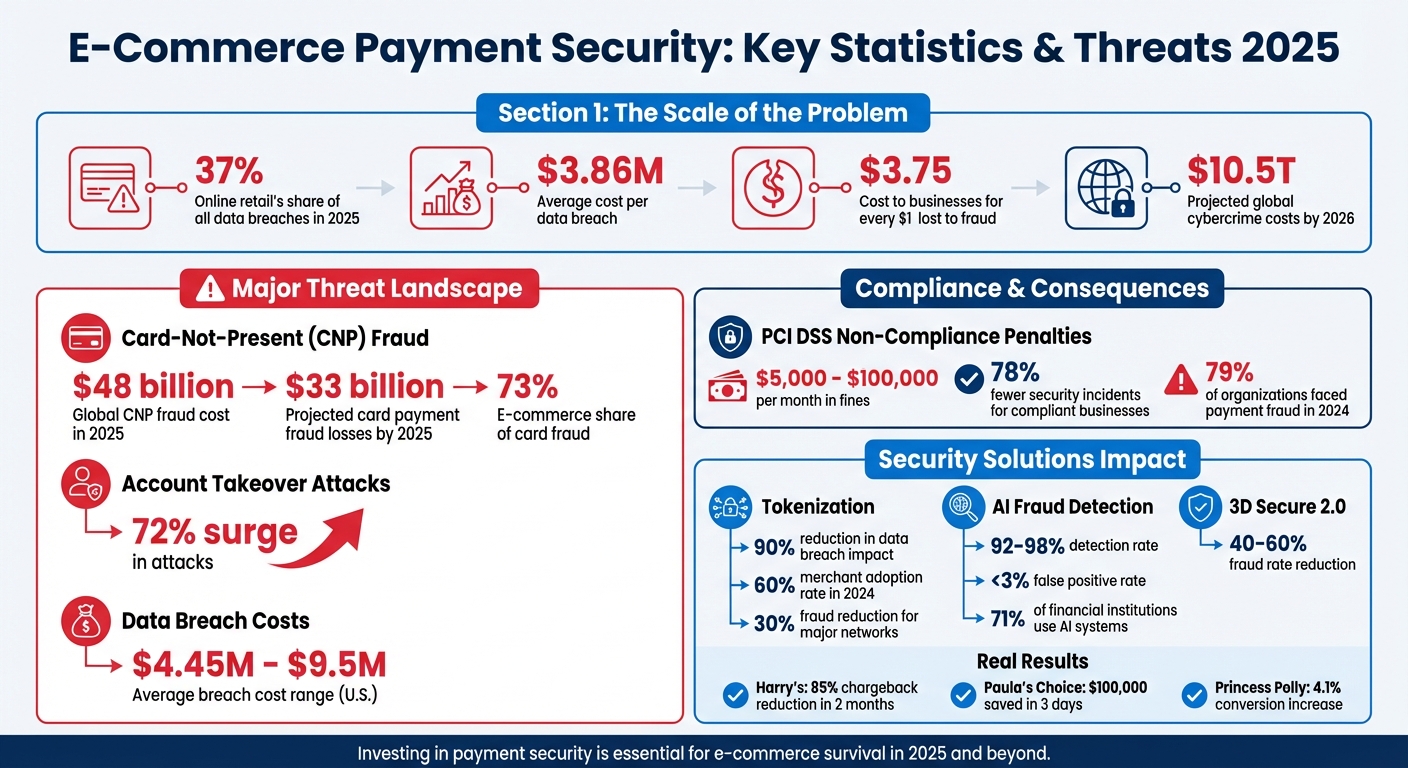

E-commerce businesses are prime targets for cyberattacks, with online retail accounting for 37% of all data breaches in 2025. The financial impact is staggering - $3.86 million per breach on average - and fraud costs businesses $3.75 for every $1 lost. Beyond financial losses, breaches damage reputations and erode customer trust.

To protect your business, here’s what you need to know:

- Top Threats: Card-Not-Present (CNP) fraud cost $48 billion globally in 2025, while account takeover attacks surged by 72%.

- Basic Protections: Use SSL/TLS encryption, PCI DSS compliance, and enable AVS and CVV checks to secure transactions.

- Advanced Measures: Tokenization, multi-factor authentication (MFA), and AI-driven fraud detection systems can significantly reduce risks.

- Payment Gateways: Opt for PCI DSS-compliant gateways with features like tokenization, 3D Secure 2.0, and fraud filters.

With cybercrime costs projected to exceed $10.5 trillion globally by 2026, investing in payment security isn’t optional - it’s a necessity. The article below outlines practical steps to secure your e-commerce platform and protect your customers.

E-Commerce Payment Security Statistics and Threats 2025

Online Payment Security: What You Need to Know

sbb-itb-5d40823

Basic Security Measures Every E-Commerce Business Should Use

Before diving into advanced security tools, every e-commerce business should establish a solid foundation of basic protections. These measures are essential for secure payment processing and fraud prevention. Without them, you risk fines, losing customer trust, and interruptions to your payment processes.

SSL/TLS Certificates for Encrypted Connections

An SSL certificate ensures a secure, encrypted connection between your server and your customers' browsers, safeguarding sensitive information like credit card numbers. This secure link is created through a quick handshake where the browser verifies your server's certificate and exchanges encryption keys. To stay protected, make sure your payment pages use TLS 1.2 or higher, which helps prevent man-in-the-middle attacks.

Since 2014, Google has used HTTPS as a ranking factor, and in 2018, Chrome began labeling non-HTTPS sites as "not secure". SSL certificates typically use 256-bit encryption and need to be renewed annually.

"An SSL certificate acts both like a passport to verify the website owner's identity and like a key to keep user data secure via strong encryption." – Michael Keenan, Shopify

Choose the right SSL certificate for your business:

- Domain Validated (DV): Ideal for small stores, costing $0 to $99 per year.

- Organization Validated (OV): Better for mid-sized businesses, priced between $100 and $999 annually.

- Extended Validation (EV): Best for large e-commerce platforms, with costs starting at $1,000 per year.

- Wildcard SSL: Secures multiple subdomains under one certificate, great for businesses with diverse site sections like shop.example.com and blog.example.com.

After installing your SSL, test its configuration using tools like Qualys SSL Labs' "SSL Server Test". Ensure all site resources - images, CSS, and JavaScript - load over HTTPS to avoid mixed content warnings, and renew your certificate well in advance to avoid lapses. Additionally, meet industry standards like PCI DSS to ensure comprehensive payment security.

PCI DSS Compliance: Meeting Payment Security Standards

PCI DSS (Payment Card Industry Data Security Standard) is a contractual requirement for businesses handling cardholder data, enforced by major card brands like Visa and Mastercard. Non-compliance can lead to fines ranging from $5,000 to $100,000 per month and could even result in losing the ability to process credit card payments. Data breaches, on average, cost businesses between $4.45 million and $4.88 million.

PCI DSS is built around 12 core requirements grouped into six objectives. These include securing networks, encrypting cardholder data, managing vulnerabilities, controlling access, monitoring systems, and maintaining a formal security policy. Starting March 31, 2025, PCI DSS v4.0 will be mandatory, introducing requirements like multi-factor authentication (MFA) for all card data system access and script integrity monitoring to counter Magecart-style attacks.

Simplify compliance by reducing your scope. Hosted payment solutions can shrink your PCI scope by up to 90%, qualifying you for the simpler SAQ-A questionnaire instead of the more rigorous SAQ-D, as card data is directly processed by the payment provider.

Compliance requirements vary by transaction volume:

- Level 1 merchants (processing over 6 million transactions annually) must undergo yearly on-site audits by a Qualified Security Assessor (QSA) and perform quarterly vulnerability scans.

For PCI DSS v4.0 compliance, ensure all JavaScript on payment pages is tracked, and use Content Security Policy (CSP) headers to block unauthorized script changes. Regularly conduct quarterly scans, annual penetration tests, and enforce MFA for all admin access. Strengthening security at the transaction level can further reduce risks.

Address Verification System (AVS) and CVV Checks

To combat fraud during transactions, use automated systems like Address Verification System (AVS) and CVV checks. AVS compares the billing address provided by the customer to the one on file with the card issuer, flagging mismatches that may indicate fraud. The CVV (Card Verification Value) - the 3- or 4-digit code on the card - adds another layer of security by confirming that the customer physically possesses the card. Since PCI DSS forbids storing CVV data, even a data breach won’t expose this sensitive information.

Most payment gateways handle AVS and CVV checks automatically. Configure your gateway to reject transactions that fail these checks, such as mismatched billing and shipping addresses or missing CVV codes. These measures also deter "card testing", where fraudsters use small transactions to check stolen card details.

Add extra safeguards:

- Set rate limits for checkout attempts, such as three attempts per minute per IP, to block bots from testing stolen cards.

- Avoid storing CVV data entirely, as it violates PCI DSS Requirement 3 and increases liability in case of a breach.

- Consider hosted payment forms provided by your processor to securely handle CVV and address data, keeping this information off your servers and reducing compliance scope.

For even stronger protection, implement 3D Secure 2.0. This technology provides additional authentication, offering a frictionless experience for low-risk transactions while challenging high-risk ones. It can reduce fraud rates by 40–60% and shifts liability to the card issuer.

Advanced Security Strategies for E-Commerce

Once you've established basic security measures, it's time to step up your game with advanced strategies that actively counter fraud in real-time. These tactics go beyond the basics, adapting to new fraud techniques and maintaining customer trust.

Data Encryption and Tokenization

Encryption scrambles sensitive data into unreadable ciphertext using algorithms like AES, protecting it as it moves from the customer's browser to your payment gateway. Tokenization, on the other hand, replaces sensitive card details with a randomly generated token, while the actual data is securely stored off-site. This approach can reduce the impact of data breaches by up to 90% and simplifies PCI compliance requirements.

The numbers highlight the stakes: global card payment fraud losses are projected to surpass $33 billion by 2025, with e-commerce transactions accounting for 73% of that figure. Additionally, the average cost of a data breach in the U.S. now hovers around $9.5 million.

"The whole security principle behind tokenization is that the token itself is useless if stolen. Since there's no mathematical key to reverse-engineer it, a hacker would have to breach the heavily fortified token vault to get the original data." – ChargePay

To further enhance security, use modern TLS standards for data in transit. Hosted payment fields, like Stripe Elements, ensure card data flows directly to your payment processor, keeping sensitive information off your servers and simplifying compliance with SAQ-A forms. These measures, combined with strong data protection, set the stage for even more secure transaction processes.

Multi-Factor Authentication (MFA) at Checkout

MFA makes it significantly harder for cybercriminals to succeed by requiring multiple verification steps, such as passwords, mobile devices, or biometrics. A standout example is 3D Secure 2.0 (3DS2), which allows banks to verify transactions behind the scenes, only involving customers when there's a potential risk. Risk-based authentication adds another layer, triggering MFA for high-value orders or unusual behavior like logins from new devices.

The benefits are clear. Princess Polly saw a 4.1% boost in conversion rates and a 7.6% reduction in checkout time after implementing authenticated checkout. Similarly, FragranceNet.com experienced a 3.4% increase in conversions and a 7.5% rise in new customer acquisitions by integrating one-time codes and pre-filled information.

Digital wallets like Apple Pay, Google Pay, and PayPal streamline authentication further by using built-in biometrics and tokenization. Passkeys, which rely on device-bound biometric credentials like FaceID or TouchID, are gaining traction too. In 2024, 61% of consumers considered passkeys more secure than traditional passwords, and 58% found them more convenient.

To prevent MFA fatigue, avoid over-relying on simple push notifications, which have been linked to 14% of security breaches. Instead, use methods like number matching or biometric confirmation. And if a payment fails during MFA, make sure the cart's contents and pre-filled fields remain intact for a smoother experience.

AI-Driven Fraud Detection

Advanced fraud detection systems go beyond user verification by monitoring behavior in real-time. AI analyzes transaction patterns and behavioral signals - like device fingerprints, typing rhythms, and navigation habits - to assign risk scores. These systems achieve detection rates between 92% and 98%, with false positive rates under 3%. This accuracy matters because every dollar lost to fraud can result in $30 in lost sales due to false declines. A single $100 fraudulent order could cost up to $340 when factoring in chargebacks and investigation fees.

Real-world examples showcase the effectiveness of these tools. Harry's reduced chargebacks by 85% in just two months using Sift's machine-learning models. Paula's Choice saved over $100,000 in fraudulent orders within three days and achieved a sixfold return on investment. Poshmark cut spam content by 60–70% within a week of deploying AI algorithms.

To optimize fraud prevention, consider a three-tier verification framework:

- Low-risk orders (score 0–30): Auto-approved instantly.

- Medium-risk orders (score 31–70): Require step-up verification like 3DS2 or SMS codes.

- High-risk orders (score 71–100): Automatically declined.

Adding rate limits in your web application firewall - such as capping login attempts to five per minute and checkout attempts to three per minute - provides an extra layer of defense. Since static fraud models can lose 10–15% accuracy within 90 days, retrain your machine learning models monthly to stay effective.

"The goal is not zero fraud - that requires declining too many legitimate customers. The goal is optimal fraud management: catching enough fraud to keep chargebacks below 0.3% while approving enough legitimate orders to maximize revenue." – ECOSIRE Research and Development Team

Regularly review false positives by examining decline appeals to avoid alienating legitimate customers. Tools like Stripe Radar (included with processing) or Radar for Fraud Teams (around $0.07 per screened transaction) provide actionable insights. Providers like Signifyd and Forter even offer chargeback guarantees, charging between 0.5% and 1.5% of the protected transaction value.

Choosing the Right Payment Gateway

Selecting the right payment gateway is a critical step in ensuring secure and seamless transactions for your customers. Think of it as the link between your checkout page and your customer’s bank. If this link is weak, it can lead to lost sales and security risks. With a staggering 70% of online shopping carts abandoned due to payment process issues, the stakes couldn’t be higher. A well-chosen payment gateway not only processes payments efficiently but also safeguards your business while building trust with your customers.

Key Features of Secure Payment Gateways

A secure payment gateway should come equipped with advanced tools to protect sensitive customer data. At the top of the list is PCI DSS Level 1 compliance, the gold standard for handling credit card information. Another must-have feature is tokenization, which replaces raw card details with unique digital tokens, ensuring sensitive information doesn’t reside on your servers. In 2024, tokenization adoption reached 60% among merchants, reducing fraud by 30% for major networks like Visa.

Encryption is another cornerstone of security. Your gateway should use SSL/TLS encryption to protect data during transmission. Pair this with 3D Secure 2.0, which adds an extra layer of verification, such as biometrics or one-time passwords, to confirm the cardholder’s identity. This not only reduces fraud but also shifts liability away from your business. Additionally, modern AI-driven fraud detection systems - used by over 71% of financial institutions - analyze transaction patterns, IP addresses, and geolocation in real time to flag suspicious activity.

Other essential features include AVS (Address Verification System) and CVV checks to confirm billing information and verify the cardholder’s presence during transactions.

"A secure payment gateway is the bedrock of customer confidence." – Razorpay

How to Evaluate and Set Up a Payment Gateway

Once you’ve identified the security features you need, the next step is to ensure the gateway integrates smoothly with your business operations. Start by verifying platform compatibility. Does the gateway offer native plugins for platforms like Shopify, WooCommerce, Magento, or BigCommerce? For custom-built websites, assess the quality of their APIs and SDKs - poor documentation can slow down your integration process. It’s also crucial to ensure the gateway works seamlessly with your CRM, accounting software, and customer support tools.

Settlement speed is another factor to consider. Opt for gateways offering fast payouts, such as T+1 or same-day settlements. If your business operates globally, check for support for local payment methods and multi-currency settlements.

Types of Payment Gateways:

- Hosted (Redirect): Redirects customers to an external site for payment processing. It’s easier to manage since the provider handles most security responsibilities, making it ideal for startups and small businesses.

- API / Integrated: Keeps the payment process on your site, offering more control but requiring stronger in-house security measures. This option is better suited for mid-size to enterprise businesses.

In terms of cost, most providers charge around 2.9% + $0.30 per transaction, with potential additional fees for chargebacks or cross-border transactions. Keep in mind that a one-second delay in your checkout page’s load time can drop conversions by 7%, and 53% of mobile shoppers will abandon a site that takes longer than three seconds to load.

Before launching, test your integration in a sandbox environment to ensure everything works as expected. Configure fraud filters to flag risky transactions, enable proxy detection to identify suspicious IPs, and activate two-factor authentication (2FA) on your gateway management account to prevent unauthorized changes. Decide whether to capture payments automatically or manually review high-risk orders for added control.

Lastly, offering digital wallets like Apple Pay and Google Pay, along with familiar payment methods, can significantly reduce cart abandonment. After all, 25% of shoppers leave their carts behind when they don’t trust a site with their credit card information.

Conclusion

Securing payment systems effectively requires a mix of solid baseline protections and forward-thinking strategies. By combining essential tools like SSL/TLS encryption and PCI DSS compliance with advanced approaches such as AI-powered fraud detection and tokenization, e-commerce businesses can create a strong shield against threats. With global cybercrime costs projected to exceed $10.5 trillion and CNP fraud expected to hit $48 billion by 2025, the stakes couldn't be higher.

The move from reactive to predictive security is gaining momentum. Modern AI tools now evaluate millions of data points in real time, identifying suspicious activity before a transaction is finalized. This shift is critical, especially when 79% of organizations faced payment fraud in 2024, and the average cost of a data breach reached $4.4 million. Notably, businesses that adhere to PCI DSS standards report 78% fewer security incidents. Such proactive methods form the backbone of robust monitoring systems.

Ongoing vigilance sets secure organizations apart from those at risk. Implementing real-time alerts, conducting quarterly vulnerability scans, and scheduling annual penetration tests are essential for identifying weak points. Automating patch management and keeping comprehensive logs of system access further enhance the ability to respond quickly to incidents.

FAQs

What’s the quickest way to reduce my PCI DSS scope?

The quickest way to shrink your PCI DSS scope is by choosing a payment setup that minimizes your interaction with cardholder data. For e-commerce businesses, hosted payment solutions are a great option. These redirect customers to third-party payment processors, keeping sensitive data off your systems. Alternatively, client-side tokenization methods can be used to secure transactions without storing or processing card data directly. Both strategies make compliance easier and help cut down on associated costs.

When should I turn on 3D Secure 2.0 at checkout?

To strengthen fraud prevention, create a smoother experience for mobile users, and meet PSD2 compliance, make sure to enable 3D Secure 2.0 at checkout. It's best to activate this feature during the payment process after fully integrating the system into your platform.

How do I tune fraud filters without causing false declines?

To fine-tune fraud filters effectively, it’s essential to strike a balance between catching fraud and ensuring a smooth customer experience. Leveraging AI-powered systems can make a big difference here. These systems assign detailed risk scores and evolve over time, helping to reduce false positives while keeping security intact.

Make it a habit to review cases of false declines regularly. This allows you to adjust risk thresholds and identify patterns in transactions that may need attention. By doing so, you can refine your filters, ensuring fewer legitimate customers are wrongly declined - all without sacrificing fraud prevention efforts.