Cross-Border Payments: Challenges and Solutions for Global E-Commerce

Cross-border payments are essential for global e-commerce, enabling businesses to reach international customers, pay overseas suppliers, and manage remote teams. However, these transactions come with challenges like high fees, slow processing times, fraud risks, and complex regulations. Here's a quick overview of the key points:

- High Costs: Hidden currency fees and intermediary charges can inflate costs by 1.5%-4%.

- Fraud Risks: International transactions face higher fraud rates, with chargebacks costing up to $100 per incident.

- Regulatory Hurdles: Compliance with varying laws like GDPR and AML is time-consuming and expensive.

- Slow Settlements: Payments often take 2–5 days, disrupting cash flow and causing exchange rate losses.

Solutions include:

- Using local payment methods (e.g., iDEAL, Pix) to increase approval rates.

- Implementing multi-currency accounts to avoid unnecessary conversions.

- Leveraging automation for compliance, reconciliation, and fraud prevention.

- Adopting AI tools for real-time fraud detection and dispute resolution.

Payments Unbound: The future of cross-border payments

sbb-itb-5d40823

Common Problems in Cross-Border Payments

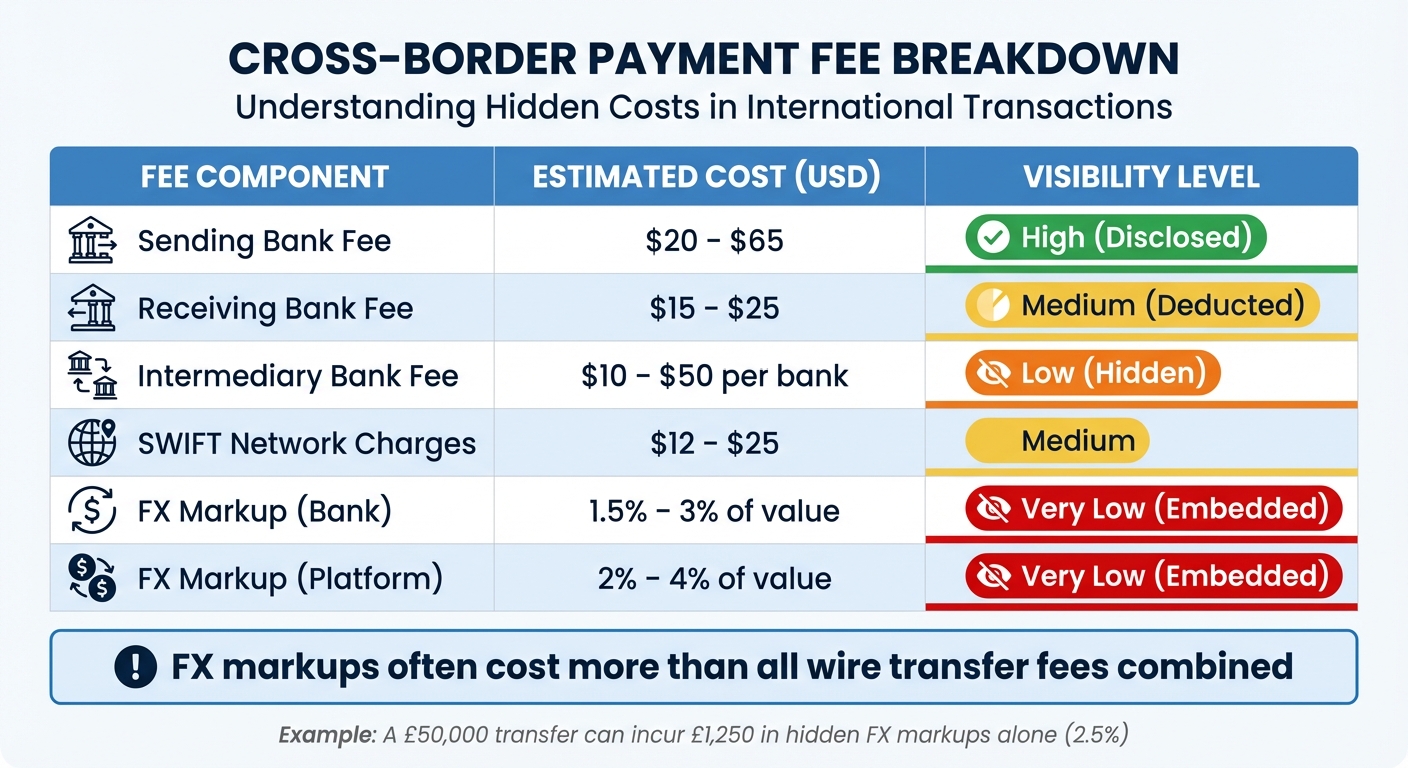

Cross-Border Payment Fee Breakdown: Hidden Costs and Visibility Levels

Cross-border payments come with challenges at nearly every stage of the process. Unlike domestic payments, which often follow straightforward paths, international transactions involve multiple intermediaries, complex regulations, and added costs. These hurdles often translate into high fees and unpredictable exchange rates, as explained below.

High Fees and Currency Exchange Rate Fluctuations

International payments are rarely simple. They typically pass through several banks, each taking a cut. On top of that, hidden fees - like foreign exchange (FX) markups - can inflate costs significantly. These markups, often ranging between 1.5% and 4% above the mid-market rate, are a major source of expense.

Here's an example: A £50,000 transfer from the UK to the U.S. in 2024 incurred total costs of £1,345 (about 2.7% of the transfer value). Of that, £1,250 came from hidden FX markups alone. On average, UK small and medium businesses lose £992.20 per international transaction due to these markups, leading to an annual collective loss of £4 billion.

"A 2.5% FX markup on a £50,000 transfer equals £1,250 in hidden costs, more than all wire transfer fees combined." - Torsion.ai

The situation worsens with less common currencies, where double conversions further increase costs. Settlement delays of 2–5 days can also cause exchange rates to shift during the transaction, leading to unexpected losses. For instance, a manufacturing company making $500,000 in monthly supplier payments faced annual losses of $134,000–$162,000 due to FX markups and delayed settlements. This included $10,000 in monthly FX fees and $50,000 in working capital tied up during the processing period.

| Fee Component | Estimated Cost (USD) | Visibility |

|---|---|---|

| Sending Bank Fee | $20 – $65 | High (Disclosed) |

| Receiving Bank Fee | $15 – $25 | Medium (Deducted) |

| Intermediary Bank Fee | $10 – $50 per bank | Low (Hidden) |

| SWIFT Network Charges | $12 – $25 | Medium |

| FX Markup (Bank) | 1.5% – 3% of value | Very Low (Embedded) |

| FX Markup (Platform) | 2% – 4% of value | Very Low (Embedded) |

Regulatory Compliance and Multi-Country Legal Requirements

Every country has its own set of payment regulations, making compliance a daunting task for global businesses. Anti-Money Laundering (AML) rules, Know Your Customer (KYC) requirements, and sanctions screening vary widely across jurisdictions. Businesses must also navigate conflicting privacy laws, such as the EU's GDPR, China's PIPL, and Brazil's LGPD. On top of this, some countries require companies to obtain specific licenses - like those from the FCA in the UK or MAS in Singapore - often necessitating the creation of local entities.

Failing to comply with these regulations can result in severe penalties, including fines, frozen accounts, or even a halt in operations. Compliance delays also impact customer experience, leading to abandoned transactions and lost trust. With the global cross-border payments market valued at $1 quadrillion in 2024 and the B2B segment alone accounting for $31.6 trillion, these regulatory hurdles add significant strain to businesses already grappling with fraud risks and disputes.

Fraud Risks, Chargebacks, and Dispute Resolution

Cross-border transactions are far more susceptible to fraud than domestic ones. In fact, 63% of card fraud value in 2021 came from international transactions. Fraudsters exploit gaps in oversight between countries, taking advantage of limited data sharing among regulatory bodies.

When fraud or disputes occur, resolving them is no small feat. Chargebacks, for instance, cost businesses between $20 and $100 per incident. But the real cost is much higher: for every $1 lost to fraud, businesses without strong fraud prevention measures lose an additional $4.24. Companies must also deal with immediate fund withdrawals and spend resources gathering evidence while coordinating across time zones.

"Every $1 lost to fraud costs $4.24 for businesses that don't integrate customer experience operations with fraud prevention strategies." - Stripe

Disputes are further complicated by jurisdictional differences. Evidence acceptable in one country might not meet the standards in another, and currency fluctuations during the process can make reconciliation tricky. Language barriers and time zone differences only add to the delays. High chargeback rates can lead to increased transaction fees - rising from around 2.9% to 4.5% or more - and, in extreme cases, termination of payment processing accounts.

Slow Payment Processing and Poor Visibility

Outdated payment infrastructures are another major issue. Settlement delays of 2–5 days are common, which can disrupt cash flow for businesses managing supplier payments, inventory, or refunds. During these delays, funds remain stuck in transit, tying up working capital.

The lack of real-time tracking makes matters worse. Unlike domestic payments, international transactions often pass through multiple correspondent banks, creating a "black box" effect. Merchants and customers are left in the dark about when funds will arrive. This uncertainty erodes trust - 59% of customers abandon their carts when their preferred local payment method isn't available.

How to Improve Cross-Border Payment Processing

To streamline cross-border payments, focus on reducing fees, speeding up transactions, and minimizing fraud risks. This can be achieved by combining local payment options, automation, and advanced risk management into a well-rounded strategy. Leveraging local payment methods and multi-currency solutions can also enhance the customer experience significantly.

Local Payment Methods and Multi-Currency Accounts

Integrating local payment methods is a proven way to increase conversion rates. For instance, in the Netherlands, the iDEAL payment system handles 57% of all transactions. Customers are more likely to complete a purchase when they see familiar payment options. In fact, 94% of global shoppers prioritize transparent pricing and their preferred payment methods during checkout.

Multi-currency pricing (MCP) is another game-changer. By displaying prices in a customer’s local currency, you not only make costs predictable but also reduce conversion fees, which can improve conversion rates by 24%. For example, formatting prices as €19.99 instead of €20.23 and using IP-based geolocation to show the correct currency can make a big difference.

Multi-currency wallets and virtual accounts allow businesses to hold funds in their original currency, avoiding unnecessary conversions. This means companies can convert funds when exchange rates are favorable and pay local vendors or taxes directly from these accounts. The result? Avoiding double-conversion fees and reducing exposure to fluctuating rates. Businesses that match their inflows and outflows in the same currency can save thousands annually.

Local acquiring and smart routing are also effective. By routing transactions through local acquirers that align with the card's BIN country - such as sending a UK card to a UK acquirer - businesses can significantly improve authorization rates. Single-integration platforms simplify this process by offering access to numerous local payment methods through a single API, cutting down on engineering effort while broadening global reach.

| Market | Critical Local Payment Methods |

|---|---|

| Germany | Klarna, SOFORT, PayPal |

| Netherlands | iDEAL |

| Brazil | Pix, Boleto Bancário |

| China | Alipay, WeChat Pay |

| India | UPI, Net Banking |

| Japan | Konbini (cash payments), Credit Cards |

Another key tactic is using Delivered Duties Paid (DDP) to collect import duties and taxes during checkout. Unexpected fees at delivery - known as "landed costs" - cause 65% of shoppers to abandon their carts. Displaying the total cost upfront builds trust and reduces cart abandonment.

API Integrations and Automated Reconciliation

Manual reconciliation is not only slow but also prone to errors. Real-time APIs can connect payment systems with ERP and accounting tools like NetSuite, Xero, or QuickBooks, boosting cash flow visibility and cutting payment errors by 66%. Validating country-specific payment details, such as IBANs, SORT codes, or Tax IDs, upfront can also prevent transaction failures.

Automation can further streamline processes by managing W-8/W-9 form collection and calculating withholdings for international contractors, ensuring compliance without manual effort.

"Managing international payments isn't just a back-office challenge - it's a business-critical operation." - Tipalti

For B2B or high-value transactions, SWIFT gpi offers end-to-end tracking and transparency on intermediary bank fees, addressing one of the most frustrating aspects of cross-border payments. Additionally, businesses should prepare for the mandatory controls under PCI DSS 4.0 by March 31, 2025, and the transition to ISO 20022 by November 22, 2025, which will enhance reconciliation with richer, structured data.

Automation also lays the groundwork for advanced fraud prevention powered by AI.

AI-Powered Fraud Detection and Risk Management

Fraud is a significant concern in cross-border transactions. AI tools are transforming fraud prevention by shifting from static rules to real-time behavioral analysis. These tools assess hundreds of data points - like customer identity, transaction patterns, geolocation, and device fingerprints - to assign risk scores in milliseconds.

AI models don’t just detect suspicious activities; they also automate case triage, allowing fraud analysts to focus on higher-risk cases. Pairing 3D Secure authentication with AI-driven fraud detection can block fraudulent transactions while minimizing disruptions for legitimate customers.

The financial impact of fraud is staggering: for every $1 lost, businesses incur an additional $4.24 in related costs. AI-powered tools can help reduce these losses while maintaining a smooth customer experience.

AI-Driven Transaction Dispute Recovery with DidIBuyIt

Efficiently resolving disputes is crucial for maintaining trust. DidIBuyIt simplifies this process by analyzing disputes, generating bank-ready documents, and offering step-by-step guidance for handling chargebacks and refund claims across platforms like Visa, Mastercard, Amex, and PayPal.

The platform’s encrypted data, 24/7 support, and real-time tracking ensure disputes are resolved quickly and securely. For businesses with high chargeback rates, these tools can cut dispute-related costs and reduce the risk of account termination.

| Plan Name | Price | Key Features | Best For |

|---|---|---|---|

| Basic Recovery | Flat Fee | AI analysis, bank-ready documents, step-by-step guidance, encrypted data | Standard disputes on supported platforms |

| Advanced Support | Flat Fee | Includes Basic features, priority support, advanced evidence preparation | Complex disputes needing detailed documentation |

This approach adds another layer to a comprehensive cross-border payment strategy.

Working with Global Payment Platforms

Global payment platforms can simplify compliance and streamline processes. Choose providers with expertise in navigating AML, KYC, and sanctions screening across multiple jurisdictions. Automated checks against international sanctions lists (OFAC, UN, EU) ensure compliance without manual effort.

Emerging technologies like blockchain and DLT are improving transparency, reducing intermediaries, and speeding up settlements. For example, global stablecoin transaction volumes reached $27 trillion annually as of 2025. Real-time payment networks such as FedNow (US), Faster Payments (UK), Pix (Brazil), and SPEI (Mexico) are also providing faster alternatives to traditional wire transfers.

Platforms that integrate local wallets - like Alipay, Apple Pay, and WeChat Pay - enhance transaction security and efficiency while catering to local preferences. PayPal’s cross-border trade volume, for instance, grew to $54.3 billion in Q3 2025, marking an 8% year-over-year increase.

"Success often turns on aligning demand with payments, cross-border payouts, fulfillment, and localized experiences that reduce friction for international buyers." - PayPal Editorial Staff

Finally, ensure your payment provider meets international standards like PCI DSS and SOC 2 to safeguard financial data. With the global cross-border payments market projected to exceed $250 trillion by 2027, the right platform can help businesses navigate challenges and seize growth opportunities.

Conclusion

Cross-border payments bring a unique set of challenges to global e-commerce, from steep fees and stringent regulations to fraud risks that slash approval rates to just 50–60%. Yet, these hurdles also open the door to potential advantages for businesses willing to adapt. By embracing local payment methods, multi-currency accounts, API-driven automation, and AI-powered fraud detection, companies can transform obstacles into opportunities.

As global markets grow, payment infrastructure has shifted from being a back-office necessity to a key driver of international expansion. Businesses that integrate local payment systems like iDEAL in the Netherlands or Pix in Brazil, display prices in local currencies, and adopt Delivered Duties Paid (DDP) shipping to avoid unexpected fees can see noticeable boosts in conversion rates.

Efficient dispute resolution is also critical in overcoming these challenges. Tools like DidIBuyIt simplify the process with AI-driven analysis and bank-ready documentation, cutting chargeback costs while preserving customer trust. Paired with real-time fraud detection and automated reconciliation, these technologies reduce manual workloads and financial strain caused by disputes.

The way forward is clear: diversify payment options, automate compliance and reconciliation, use AI for better security and efficiency, and focus on customer satisfaction with transparent pricing and local payment choices. As PayFuture aptly stated, "Payment failure is not a technical problem. It's a growth problem". By investing in modern payment systems and AI-driven solutions, your business can thrive in the ever-expanding global market.

FAQs

How can I reduce hidden FX fees on international sales?

To keep hidden FX fees in check when handling international sales, consider these approaches:

- Use multi-currency accounts: These accounts let you hold and transact in multiple currencies, reducing the need for frequent conversions.

- Pay in local currencies: Whenever possible, settle payments in the currency of the recipient to avoid costly conversion fees.

- Choose payment providers wisely: Opt for providers that offer transparent pricing and low currency conversion fees.

By implementing these strategies, you can cut down on unnecessary charges and take better control of your costs.

What do I need to stay compliant with AML, KYC, and privacy laws abroad?

To meet international regulations like AML, KYC, and privacy laws, it's crucial to verify the identities of customers, vendors, and contractors. This can be done by reviewing government-issued IDs, proof of address, and business registration documents. On top of that, keep an eye on transactions for any suspicious activity, report irregularities promptly, and leverage automated tools for real-time compliance checks.

Make it a priority to stay informed about local laws, including tax regulations and data privacy requirements. Conducting regular audits is also essential to ensure your processes remain in step with changing legal standards.

How can I lower chargebacks and win cross-border disputes faster?

To tackle chargebacks and resolve cross-border disputes more efficiently, it’s essential to focus on two key areas: fraud detection and structured dispute-resolution processes.

Start by strengthening fraud detection systems. This includes implementing robust counterparty verification measures to ensure the legitimacy of transactions. Taking these precautions helps safeguard against unauthorized activities.

At the same time, having clear legal, regulatory, and industry-level mechanisms in place can simplify dispute resolution. These frameworks provide a structured approach, making it easier to address disagreements quickly and fairly.

By combining these strategies, businesses can boost transaction security, cut down on fraud-related losses, and ensure faster, smoother resolutions for everyone involved.