Stablecoins vs. Traditional Wire Transfers: A Settlement Comparison

When transferring money, you have two main options: stablecoins or wire transfers. Each has its strengths, but they differ in speed, cost, and accessibility. Here’s a quick breakdown:

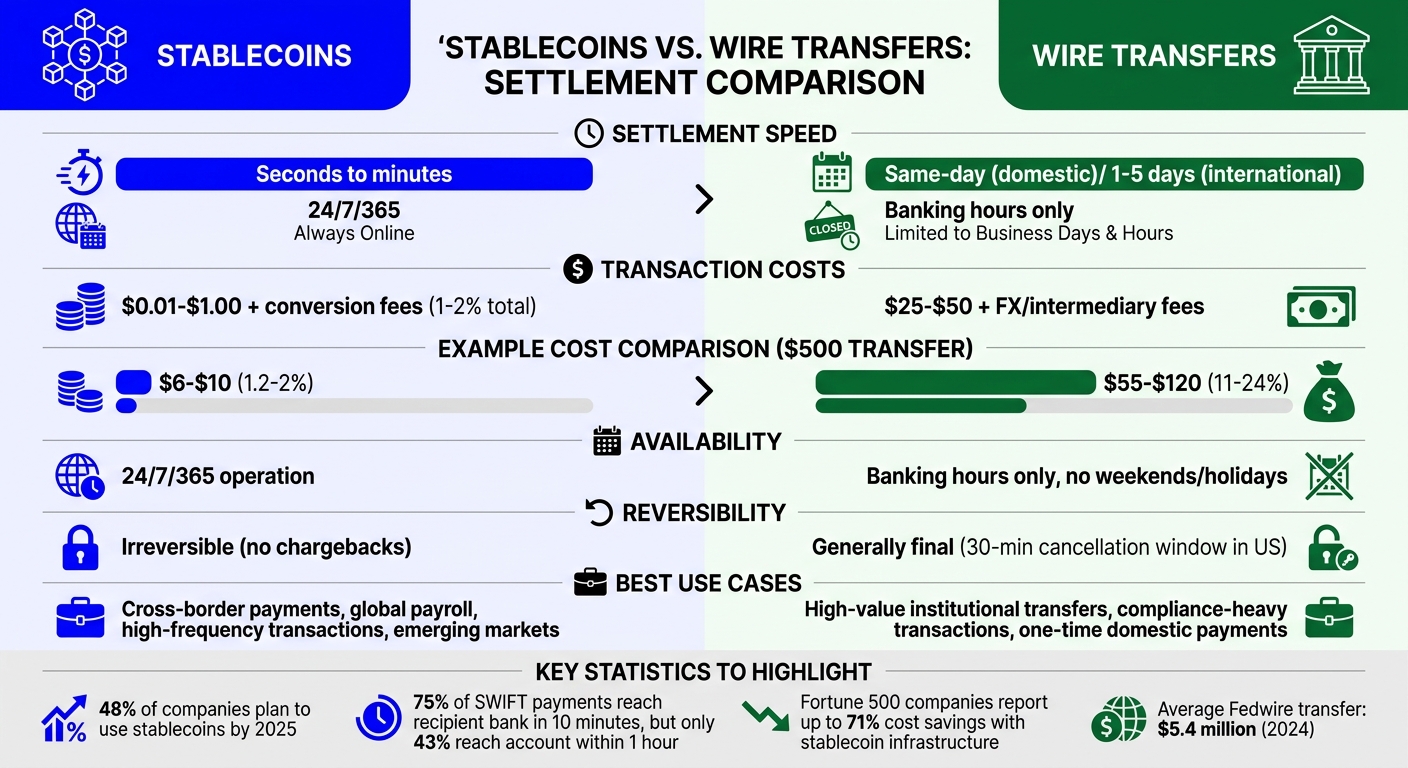

- Stablecoins: Digital tokens pegged to fiat currencies, offering near-instant, low-cost transactions 24/7. Great for cross-border payments, global payroll, and regions with limited banking infrastructure.

- Wire Transfers: Bank-based transfers suited for high-value or compliance-heavy transactions. Domestic wires are same-day (during business hours), while international wires can take 1–5 days and involve higher fees.

Quick Comparison

| Feature | Stablecoins | Wire Transfers |

|---|---|---|

| Speed | Seconds to minutes | Same-day (domestic); 1–5 days (international) |

| Cost | $0.01–$1.00 + conversion fees | $25–$50 + FX/intermediary fees |

| Availability | 24/7/365 | Banking hours only |

| Reversibility | Irreversible | Limited (30-minute cancellation window in the U.S.) |

| Best For | Cross-border, small-to-medium payments | High-value, compliance-heavy transactions |

Stablecoins excel in speed and cost-efficiency, while wire transfers are better for large, regulated payments. Choosing the right method depends on your transaction needs.

Stablecoins vs Wire Transfers: Speed, Cost, and Availability Comparison

Settlement Speed Comparison

How Fast Are Stablecoin Settlements?

Stablecoin transactions are completed in a matter of seconds or minutes. These transactions run on blockchain networks that never take a day off - no weekends, holidays, or banking hours to worry about. Once a transaction is confirmed on the blockchain, it’s final and cannot be reversed.

"Stablecoin settlement operates on blockchain networks and offers a fundamentally different model: on-chain transfers settle in minutes, operate 24 hours a day, 7 days a week, 365 days a year, and are not limited by banking hours, correspondent banking networks, or geographic boundaries." - Sphere Team

This speed is a game-changer for businesses. By 2025, nearly half (48%) of surveyed companies plan to use stablecoins, citing fast settlement as a key reason. For instance, Stripe now enables U.S. merchants to accept stablecoin payments with almost instant settlement.

Contrast this with traditional wire transfers, which are tied to banking schedules and often face delays.

How Fast Are Wire Transfer Settlements?

Domestic wire transfers, processed through systems like Fedwire, generally settle on the same day - provided they’re initiated during business hours. Miss the cutoff time, and the transfer gets pushed to the following business day. Weekends and bank holidays can stretch out the delay even further.

International wire transfers, however, are much slower. While 75% of SWIFT cross-border payments reach the recipient’s bank within 10 minutes, the funds don’t immediately show up in the recipient’s account. Factors like local banking hours, compliance checks, and domestic processing systems can extend the wait time to anywhere between 1 and 5 business days. Notably, only 43% of these payments actually reach the recipient’s account within one hour.

"The last mile remains stubborn. Delays typically occur at the post-arrival crediting step - the beneficiary leg - where local banking hours, compliance checks, and domestic rails determine end-to-end speed." - Team Bitwage

Speed Comparison Table

| Feature | Stablecoin Settlement | Domestic Wire Transfer | International Wire Transfer |

|---|---|---|---|

| Average Speed | Seconds to Minutes | Same-day (within cutoff) | 1–5 Business Days |

| Operating Hours | 24/7/365 | Business hours only | Business hours only |

| Intermediaries | None (Peer-to-Peer) | Central Bank (Fedwire) | 3–5 Correspondent Banks |

| Finality | Instant on-chain | Final once settled | Final once settled |

| Primary Delay Factors | Network congestion | Cut-off times, holidays | Time zones, manual checks |

sbb-itb-5d40823

How Stablecoins Will Eat Payments

Transaction Costs and Fees

While transaction speed is undoubtedly important, the fees associated with each method play a big role in determining overall efficiency. Let’s break down the differences between stablecoin transactions and traditional wire transfers.

Stablecoin Transaction Fees

Stablecoin transactions are known for their low network fees, often referred to as "gas fees", which vary depending on the blockchain used. For example:

- Solana charges approximately $0.0001 per transaction.

- Polygon fees range between $0.001 and $0.01.

- Layer 2 networks like Base, Arbitrum, and Optimism typically charge between $0.05 and $0.50.

- Ethereum mainnet, while pricier, ranges from $1 to $15 depending on network congestion.

When converting fiat currency into stablecoins, additional fees apply. Institutional platforms like Circle Mint offer 0% fees for high-volume transactions, while Coinbase Prime charges between 0 and 50 basis points (0.5%) based on transaction volume. Retail platforms, such as MoonPay or Ramp, tend to charge higher rates, typically between 1% and 4.5%.

Overall, stablecoin transfer costs generally fall below 2% of the transaction value. Unlike traditional methods, there are no intermediary banks or surprise deductions along the way.

Now, let’s see how these costs compare to wire transfers.

Wire Transfer Fees

Traditional wire transfers, on the other hand, come with a variety of fees that add up quickly. Here’s a breakdown:

- Domestic wire transfers through systems like Fedwire cost between $25 and $50 per transaction. For example, JPMorgan charges $50 for business wires, Bank of America charges $45, and HSBC UK charges £17 as of Q1 2026.

- International wire transfers include upfront fees, intermediary bank deductions of $10–$25 per bank, receiving fees between $15 and $30, and foreign exchange (FX) markups ranging from 1.5% to 6%.

"Small payments under $500 have the largest relative SWIFT penalty - sometimes 15-20% of the gross - because the fixed sender fee dominates." - Eco

For a $5,000 international wire, total costs can range from $80 to $160 when factoring in all fees and FX spreads. Additionally, about 1% to 2% of cross-border wires fail or require manual intervention, leading to further operational expenses.

Cost Comparison Table

| Transaction Amount | Route | Traditional Wire Cost | Stablecoin Cost |

|---|---|---|---|

| $500 | US to EU | $55 – $100 | $6 – $10 |

| $500 | US to Asia | $70 – $120 | $6 – $10 |

| $10,000 | US to EU | $350 – $650 | $55 – $105 |

| $10,000 | US to Asia | $400 – $700 | $55 – $105 |

For smaller amounts, the contrast is even starker. A $500 transfer through traditional wires can eat up 10% to 24% of the total value, while stablecoin fees typically remain between 1% and 2%. As Stripe points out, "A payment that might cost 6% of the transaction amount through traditional remittance channels can cost under $1 with stablecoins".

Reliability and Transaction Finality

When it comes to sending money, reliability and transaction finality are just as important as speed and cost. You want to know your payment will arrive and that once it’s processed, it’s truly done. Stablecoins and wire transfers handle these aspects differently, each with its own pros and cons.

Stablecoin Reliability and Finality

Stablecoin transactions are usually finalized within seconds or minutes, with every transaction permanently recorded on a blockchain. This means they can’t be reversed.

"Stablecoin transactions are irreversible by nature. For businesses, this means no risk of chargebacks. However, it also means there's no 'undo' button if funds are sent to the wrong address".

Once confirmed, the transaction is final. While this eliminates the risk of chargebacks, it also means recovering funds sent to the wrong address depends entirely on the recipient’s willingness to cooperate. To reduce this risk, many businesses use tools like address whitelisting, which ensures payments are only sent to pre-approved wallet addresses.

The reliability of stablecoins also hinges on how well the issuer manages reserves. Opting for regulated options like USDC, which adheres to strict reserve and transparency standards (such as those outlined in the EU’s MiCA regulation), can help minimize counterparty risk.

Wire Transfer Reliability and Finality

Wire transfers are generally final once completed, but the process behind them is less transparent and can take more time. For instance, while SWIFT messages confirm that payment instructions have been sent, there’s often a delay before the funds actually move between banks.

"The gap between SWIFT's financial instructions and banks' actual transfer execution creates a choppy process where payments appear confirmed but remain temporarily inaccessible".

This segmented process means that while you might receive confirmation, the funds may not yet be available.

In the U.S., senders have a 30-minute window to cancel certain remittances at no cost. After that, reversing a transaction becomes much harder and isn’t guaranteed. Banks do have error-resolution procedures, but once a wire transfer is executed, reversing it requires cooperation from the receiving bank, which can complicate things. Considering that the average Fedwire transfer in 2024 was about $5.4 million, these transactions often involve significant sums, making reliability critical.

Wire transfers also lack the real-time visibility that blockchain transactions offer. Instead of being able to track the process online, you’re reliant on intermediary banks for updates, which can lead to delays and additional inquiries.

Reliability Comparison Table

| Feature | Stablecoins | Wire Transfers |

|---|---|---|

| Transparency | High; publicly visible on blockchain 24/7 | Limited; dependent on bank updates |

| Transaction Finality | Instant/near-instant upon confirmation | Same-day (domestic) to 5 days (international) |

| Reversibility | Irreversible; no chargebacks possible | Generally final; 30-minute cancellation window (U.S.) |

| Dispute Resolution | None; requires a separate follow-up transaction | Bank-led error investigation; recalls not guaranteed |

| Operating Hours | 24/7/365 | Restricted to banking hours and business days |

| Execution Risk | High (errors are permanent) | Moderate (recalls are difficult but possible) |

Use Cases and Limitations

When to Use Stablecoins

Stablecoins shine in scenarios where speed, low fees, and around-the-clock availability are essential. They are particularly useful for cross-border B2B payments and global payroll, eliminating the delays often experienced with traditional systems. B2B payments, in particular, are growing at a rapid pace.

Global payroll is another area where stablecoins excel. Companies paying freelancers, digital nomads, or distributed teams in nearly 200 countries can avoid the typical 1–5 day delays associated with traditional wire transfers. For instance, in October 2025, Bitwage reported processing over $400 million in payroll for more than 90,000 workers across 4,500 companies, enabling same-day payouts in stablecoins to nearly 200 countries.

In regions with high inflation, such as Argentina, Nigeria, and Turkey, stablecoins pegged to the U.S. dollar help protect value against volatile local currencies. They are also a cost-effective solution for high-volume, low-margin businesses. Some Fortune 500 companies leveraging stablecoin infrastructure have reported cost savings of up to 71%. These features make stablecoins a strong option for specific transactional needs.

When to Use Wire Transfers

Wire transfers remain a dependable choice for large institutional transactions, especially those exceeding $500,000, where regulatory compliance and consumer protections are critical. Industries like healthcare, which often have strict compliance requirements, tend to favor wire transfers because their internal policies may not yet support digital assets.

For one-time domestic payments where urgency isn’t a concern, wire transfers are also a practical option - provided both parties are already integrated within the traditional banking system. However, this reliability often comes with trade-offs in terms of speed and cost, which are discussed further below.

Limitations of Each Method

Both stablecoins and wire transfers have their downsides. Stablecoins, for example, are irreversible and may involve additional conversion steps that can incur fees. Moreover, regulatory requirements differ by region, and the stability of stablecoins depends on whether the issuer maintains adequate reserves.

Wire transfers, on the other hand, are slower and more expensive. International transactions often require three to five intermediary banks, each adding fees that can push costs above $100 per transaction. Additional foreign exchange markups can further increase expenses. Wire transfers are also limited by banking hours, cut-off times, and public holidays.

Choosing the Right Settlement Method

Building on the analysis of speed, costs, and reliability, let’s dive into when each settlement method works best.

Best Scenarios for Stablecoins

Stablecoins shine in situations where speed and low costs are non-negotiable. This makes them ideal for supplier payments in regions like Mexico, Nigeria, or the Philippines, where traditional banking systems can be costly or slow. For example, stablecoins can drastically reduce expenses in emerging markets while ensuring payments are processed almost instantly.

As one industry expert noted:

"A treasurer needing to pay a supplier before a shipment release deadline cannot wait 3 days for a SWIFT wire to clear." – Eco

Stablecoins are particularly valuable for:

- High-frequency international payouts

- Immediate, 24/7 liquidity needs

- Payments in areas with limited banking infrastructure

In practice, corporate treasury teams are now tailoring their payment strategies by region. For emerging markets, stablecoins are becoming the go-to choice, while SWIFT remains the preferred option for transactions between major OECD countries.

Risk Management Tip: Since blockchain transactions are irreversible, implement multi-signature approvals and always test transfers before sending significant amounts.

Best Scenarios for Wire Transfers

While stablecoins are excellent for fast and cost-efficient transactions, wire transfers remain the gold standard in certain high-value scenarios. For large institutional payments, where regulatory compliance and detailed audit trails are critical, wire transfers are still the preferred method.

Wire transfers are best suited for:

- High-value transactions between Fortune 500 companies

- One-time domestic payments where same-day settlement suffices

- Payment corridors lacking mature stablecoin off-ramp infrastructure

In short, wire transfers are reliable for situations requiring strict compliance or when working within the traditional banking ecosystem.

Final Comparison Table

Here’s a side-by-side look at the key features of both methods:

| Feature | Stablecoins | Wire Transfers |

|---|---|---|

| Settlement Speed | Seconds to minutes | Same-day (domestic); 1–5 days (international) |

| Availability | 24/7/365 | Banking hours only |

| Transaction Cost | $0.01–$1.00 (plus ramp fees) | $25–$50 (plus FX/intermediary fees) |

| FX Spreads | 5–25 basis points | 50–200+ basis points |

| Reversibility | Final/Irreversible | Generally final |

| Best For | Cross-border, 24/7 needs, cost-sensitive transfers | High-value institutional transfers, strict compliance |

FAQs

How do I cash out stablecoins to my bank account?

To turn your stablecoins into cash, choose a reliable platform or exchange that allows stablecoin-to-fiat conversions. Start by transferring your stablecoins to the platform, then sell them in exchange for your local currency (like USD). Once that's done, you can withdraw the funds directly to your bank account. Make sure the platform you use is secure, follows regulations, and clearly discloses any fees and processing times. Keep in mind, you might need to complete identity verification depending on the provider's requirements.

What happens if I send stablecoins to the wrong wallet address?

If you accidentally send stablecoins to the wrong wallet address and the transaction has already gone through, there's little chance of recovering the funds - it’s generally irreversible. However, if the transaction is still pending, you might have a slim chance to cancel it by contacting the platform’s support team immediately. To avoid such costly mistakes, always double-check wallet addresses before initiating any transfer.

Which stablecoin networks are cheapest and fastest to use?

The most affordable and quickest stablecoin networks for cross-border payments are those that can handle transactions in just minutes while keeping fees low. Stablecoins like USDC and USDT are popular due to their reliability and widespread use. Although Ethereum remains a common choice, newer networks like Solana and Avalanche stand out by offering reduced fees and faster transaction speeds, making them practical alternatives for stablecoin transfers.