The Real Cost of Payment Processing Fees for Small Businesses

Payment processing fees can quietly erode a small business's revenue, often ranking among the highest operating costs. These fees - typically 2.5% to 3.5% per transaction - are unavoidable in a world where cashless payments dominate 87% of transactions (as of 2024) and are expected to reach 94% by 2027. Here's what you need to know:

- Main Fees: Interchange fees (1.5%–3.5%), assessment fees (0.13%–0.15%), and processor markups (0.1%–2.0%).

- Hidden Costs: Chargebacks ($20–$100 each), PCI compliance fees ($60–$150 annually), and batch settlement fees ($0.10–$0.30 daily).

- Payment Method Impact: Premium credit cards cost up to $35 per $1,000 sale, while ACH transfers cost as little as $0.25.

- Small Businesses Pay More: Limited transaction volume and lack of negotiation power lead to higher rates compared to large companies.

To cut costs:

- Switch to interchange-plus pricing for transparency and lower rates.

- Encourage ACH transfers or debit card payments for big transactions.

- Automate chargeback management with AI tools to save time and reduce losses.

Every percentage saved on processing fees directly improves profitability. For example, lowering your effective rate from 3.5% to 2.5% on $500,000 in sales could save $5,000 annually.

Merchant Fees Explained: Credit Card Processing Costs for Businesses

sbb-itb-5d40823

What You're Actually Paying in Processing Fees

Payment Processing Costs by Method: ACH vs Debit vs Credit Cards

Direct Costs: Interchange, Assessments, and Processor Markups

Every card transaction comes with three main fee components. First, interchange fees - the largest portion - are paid to the bank that issued your customer's card. These typically range between 1.5% and 3.5% per transaction [3][1]. The rate varies based on factors like the type of card used. For example, a rewards credit card costs more to process than a basic debit card because the issuing bank funds perks like cashback. Online transactions also tend to cost 0.2% to 0.5% more than in-person ones due to the higher risk of fraud [2].

Next are assessment fees, charged by card networks like Visa, Mastercard, and Discover for using their infrastructure. These fees are a small percentage of your monthly volume, typically between 0.13% and 0.15% [2]. As of January 1, 2026, Mastercard increased its Undefined Authorization Fee to 0.30% [2]. These fees are non-negotiable and apply uniformly to all merchants.

Finally, there's the processor markup, which covers your payment processor's service, support, and technology. This fee adds another 0.1% to 2.0% to each transaction [1][2]. Unlike interchange and assessment fees, the processor markup is negotiable. For example, on a $100 transaction processed at 2.9% + $0.30, you’d pay $3.20 total - but only about $0.40 of that goes to your processor [1].

On top of these direct costs, hidden fees can quietly increase your overall expenses.

Hidden Costs: Chargebacks, Penalties, and Extra Fees

Hidden fees can chip away at your profits in ways that aren't always obvious. Chargeback fees, for instance, apply whether you win or lose the dispute. Each chargeback can cost you between $20 and $100 [3][1]. If your business isn’t PCI compliant, you might face penalties ranging from $10 to $30 per month, annual compliance fees of $60 to $150, or fines up to $300 per year [3][2].

Other common fees include batch settlement fees of $0.10 to $0.30 every time you close out your terminal for the day [3][2]. Monthly statement or account maintenance fees can add another $5 to $50, while payment gateway access typically costs $25 to $50 per month [3]. Additionally, if you terminate a contract early, you could face fees ranging from $300 to over $500 [3][2].

Then there are downgrade fees, which occur when transactions are processed in higher-risk categories. For example, manually entering a card number instead of swiping or tapping it can trigger these higher rates [1][3]. Equipment leasing is another potential pitfall. A terminal that costs $200 to buy outright might end up costing $2,000 to $4,000 over a 48-month lease [3].

Fee Differences by Payment Method

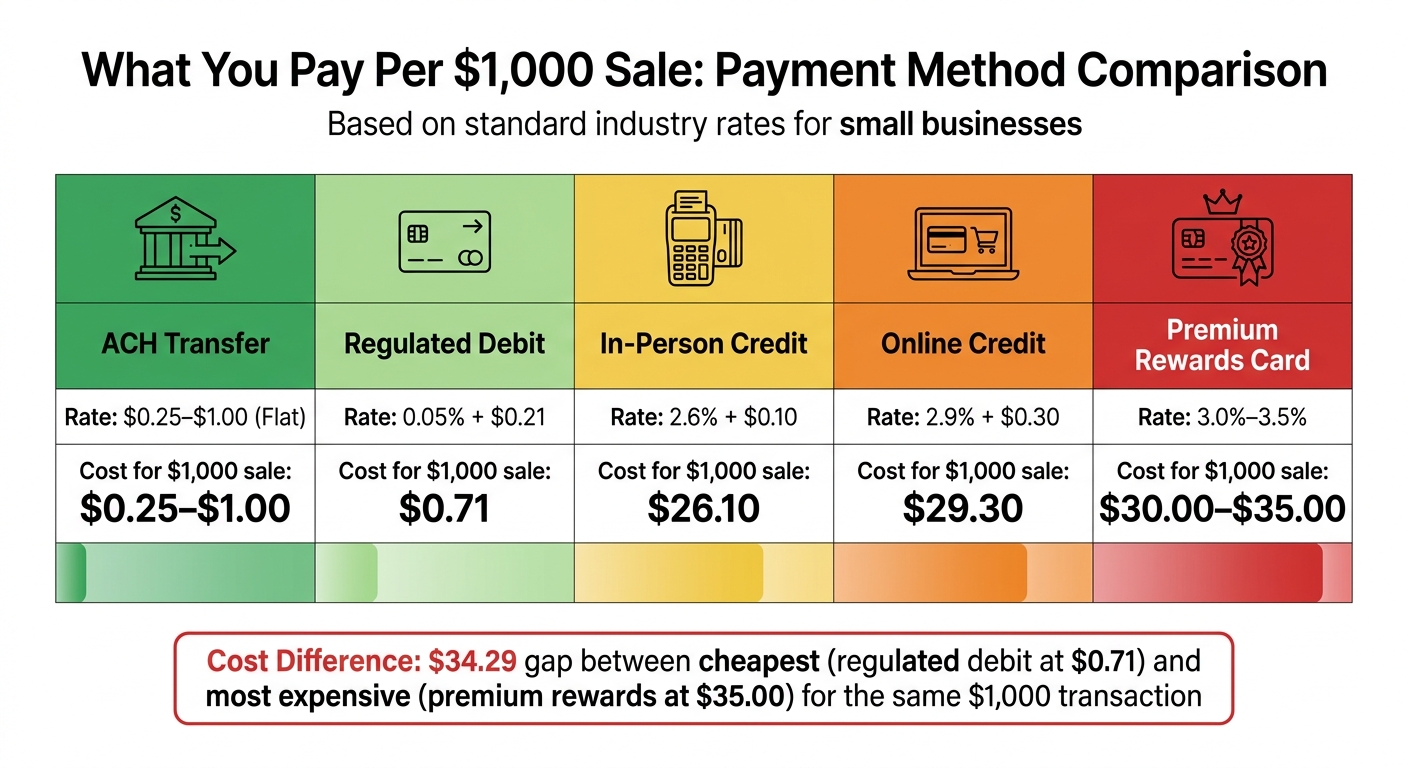

The payment method your customer uses significantly affects your processing costs. ACH transfers, for instance, are highly cost-effective for large transactions, with flat fees between $0.25 and $1.00 [1][2]. Regulated debit cards, governed by the Durbin Amendment, have capped fees of roughly 0.05% + $0.21 [2]. Credit cards, especially premium rewards cards, are the most expensive due to the high interchange fees that fund customer benefits.

Here’s a breakdown of how fees vary by payment method:

| Payment Method | Average Rate/Fee | Cost for $1,000 Sale |

|---|---|---|

| ACH Transfer | $0.25–$1.00 (Flat) | $0.25–$1.00 |

| Regulated Debit | 0.05% + $0.21 | $0.71 |

| In-Person Credit | 2.6% + $0.10 | $26.10 |

| Online Credit | 2.9% + $0.30 | $29.30 |

| Premium Rewards Card | 3.0%–3.5% | $30.00–$35.00 |

For a $1,000 sale, the cost difference is striking: a regulated debit card costs about $0.71, while a premium rewards card could cost as much as $35. That’s a $34.29 gap for the same transaction.

How Payment Fees and Disputes Affect Daily Operations

Payment disputes and chargebacks don’t just hit your wallet - they also disrupt your daily workflow, pulling valuable time and resources away from essential business activities.

Time Lost on Manual Dispute Management

Every chargeback demands attention, requiring staff to gather documentation and respond to the dispute. This process takes about 40–60 minutes per case and costs between $20 and $30 when calculated at a loaded hourly rate of $30. For a small business facing 10 disputes a month, that’s around 10 hours of productivity lost - time that could be better spent on customer service, product development, or driving revenue. Adding to the challenge is friendly fraud, which makes up 50% to 70% of all chargebacks [6]. This not only disrupts operations but also sets the stage for long-term financial challenges.

Money Lost from Unresolved Chargebacks

The financial toll of a chargeback is far greater than the initial transaction amount. For example, a $100 chargeback can result in total losses of $231 to $291 when factoring in fees, labor, lost product costs, and other related expenses. That’s nearly three times the original sale amount. In 2025, U.S. merchants lost $4.61 for every dollar of fraud - a staggering 37% increase compared to five years earlier.

On top of that, if your chargeback ratio exceeds 0.9%, payment processors may impose costly monitoring programs. These programs can lead to monthly fees between $500 and $5,000, higher processing rates (an increase of 0.5 to 2 percentage points on all transactions), and even withholding 5% to 20% of your settlement in reserve. Such measures can severely restrict your cash flow, making it harder to keep operations running smoothly [6][3].

"The visible transaction reversal represents just 20-25% of true cost. Merchandise not recovered, marketing dollars wasted, operational expenses, fees associated with reversed transactions, and systematic rate increases add up to costs 4-5 times the disputed amount." - Amrit Mohanty [6]

How to Lower Your Payment Processing Fees

Did you know you can take steps to reduce your payment processing costs? While some fees are fixed, the processor markup - typically 10–15% of your total bill - is negotiable [1]. Here are some practical ways to cut down on those expenses and keep more of your revenue.

Negotiate Better Rates with Your Processor

Switching to an interchange-plus pricing model can save you a significant amount compared to flat-rate pricing. This model breaks down your charges into two components: the base interchange fee and a transparent processor markup. Competitive markups usually fall between 0.15% and 0.50% [3]. For instance, on a $100 debit card transaction, interchange-plus pricing might cost you just $0.75, compared to around $3.20 with flat-rate pricing - potentially saving you 75% [1].

To negotiate effectively, start by reviewing three to six months of processing statements. Calculate your effective rate using this formula: (Total Fees Paid ÷ Total Volume) × 100 [1]. This data can help you pinpoint unnecessary fees. Request waivers for specific charges like PCI compliance, gateway, or chargeback fees instead of vague discounts. Mentioning that you're considering other providers can also encourage your current processor to offer better terms [7].

Use Lower-Cost Payment Methods

Payment methods aren’t all created equal when it comes to fees. ACH transfers offer a much cheaper alternative, costing a flat $0.25–$0.75 per transaction or about 0.8%, capped at $5. A $5,000 transaction via ACH might cost just $0.50, compared to $150 or more in credit card fees [3][9][1]. For everyday payments, debit cards are also a lower-cost option, with fees ranging from 1% to 2%, compared to credit cards, which typically charge between 1.5% and 3.5% [3].

If you handle B2B transactions, providing Level 2 and Level 3 data (like tax amounts and customer codes) for corporate cards can lower interchange rates by 0.5% to 1.5% [1]. Settling batches within 24 hours can also help you avoid costly "downgrades" that place transactions in higher-risk categories [1][8]. Additionally, offering cash discounts or steering customers toward ACH for larger purchases is legal in all 50 states and can shift some processing costs away from your business [3][7].

Use AI-Powered Tools Like DidIBuyIt

Manual processes for managing disputes can drain both time and money, making automation a valuable solution. AI-powered tools like DidIBuyIt simplify dispute management by analyzing cases, generating bank-ready documents, and tracking resolutions in real time. This tool supports major payment networks, including Visa, Mastercard, Amex, and PayPal.

AI-driven receipt scanning can improve accuracy by up to 90% and cut processing time by as much as 75% [10]. These systems can achieve 99.7% zero-touch reconciliation [13], reducing the need for manual involvement. By automating chargeback workflows, you can quickly spot trends, respond efficiently, and minimize revenue loss without pulling your staff away from other important tasks [11].

Monitor and Automate Chargeback Management

Chargebacks can be a major headache, but real-time monitoring tools can help you stay ahead of potential issues. Keeping your chargeback ratio below 1% is critical - exceeding this threshold could lead to account termination [3]. By integrating your payment processor's API, you can track disputes as they arise and respond immediately [11]. This proactive approach can prevent your account from being categorized as high-risk, which often comes with higher fees [3].

Set up automated alerts to detect unusual transactions or patterns that might indicate fraud before they escalate into chargebacks. With fees for chargebacks ranging from $15 to $100 per dispute [12][3], maintaining tight control is essential. AI tools can process up to 40 exceptions per hour - double the industry standard [14] - giving you the speed and precision needed to resolve disputes efficiently. These strategies not only reduce costs but also improve your financial stability.

How to Track Your Fee Reduction Results

Cost-cutting strategies are only effective if you monitor their outcomes. Without regular checks, you might overlook overcharges, unexpected rate hikes, or strategies that fail to deliver the savings you anticipated. Here’s how you can keep tabs on your fee reduction efforts.

Monthly Fee Analysis and Audits

Set aside just 30 minutes each month to review your processing statements. This small investment of time can help you spot hidden fees, such as PCI non-compliance penalties (typically $10–$30 per month), unexpected statement fees, or transactions that were "downgraded" to higher-risk categories because they weren’t settled within 24 hours [1][3].

Another useful metric to track is your effective rate, calculated as:

(Total Fees Paid ÷ Total Processing Volume) × 100 [1].

For instance, if you paid $2,500 in fees on $100,000 in sales, your effective rate is 2.5%. Compare this monthly to the industry average of around 2.35% [3]. If your rate is consistently higher, it’s a sign you could negotiate better terms or make adjustments.

Break down costs by payment method to uncover potential overcharges. Analyze how much you're spending on credit cards versus debit cards, and check if more transactions could have been processed through ACH. This breakdown can reveal trends, such as whether small transactions under $20 are disproportionately increasing your fees due to flat per-transaction charges [5].

Once you’ve established your baseline metrics, you’ll have a solid foundation for measuring the impact of your cost-saving strategies.

Calculate Your Savings by Strategy

To confirm your strategies are working, compare your effective rate from a three-month baseline period (before implementing changes) to your rate after the strategy has been active for at least one full billing cycle [15]. This comparison will clearly show whether your efforts are paying off.

Here’s an estimate of potential annual savings on $100,000 in revenue for different strategies:

| Strategy | Estimated Annual Savings | Implementation Time |

|---|---|---|

| Switch to Interchange-Plus | $300 – $800 | 1–2 weeks |

| Optimize B2B (Level 2/3 Data) | $500 – $1,500 | 2–4 weeks |

| Shift 20% of Volume to ACH | $1,000 – $2,000 | 1–4 weeks |

| Eliminate Equipment Leases | $500 – $1,000 | 1 week |

| Daily Batching/Settlement | $500 – $1,000 | Immediate |

For businesses processing more than $100,000 annually, these savings grow proportionally. For example, a company handling $500,000 could save between $1,500 and $4,000 by switching to interchange-plus pricing alone [3]. The key is to evaluate each strategy independently so you can identify which changes yield the best results for your business.

Conclusion: Take Control of Your Payment Processing Costs

What You Need to Remember

Payment processing fees can have a big impact on your profits. With the average net profit margin for small businesses hovering around 7.5%, a typical 2%–3% processing fee could eat up as much as 25% of your profit per sale[16]. That’s a chunk no business can afford to overlook.

The first step is understanding where your money is going. Around 85% to 90% of your processing costs come from interchange and assessment fees set by banks and card networks[1]. These are non-negotiable. However, the remaining 10%–15% - the processor's markup - is where you have room to negotiate. Be proactive about this. Also, keep an eye out for hidden charges like PCI non-compliance penalties or fees from transactions being "downgraded" to higher-cost categories because they weren’t settled within 24 hours.

"Active management separates businesses that merely process payments from those that optimize them." - Finix Resources[4]

With this knowledge, you can start making smarter decisions about your payment processes.

What to Do Next

Start by reviewing your fee metrics. If your effective rate is over 3.5%, you’re likely paying too much[2]. Take a closer look at your statements for any unexpected charges or errors. Since the majority of fees are fixed, focus on negotiating the portion you can control.

For businesses processing more than $10,000 monthly, request quotes for interchange-plus pricing. Encourage customers to use ACH or debit cards for larger invoices to save 1% to 2% compared to premium credit cards. Batch transactions daily to avoid downgrades, and if you handle B2B sales, submit Level 2/3 data to qualify for lower rates[1][2].

To handle disputes and reduce chargebacks, consider using tools like DidIBuyIt, which automates evidence preparation for disputed transactions. This can save you time and recover money that would otherwise be lost, adding hundreds - or even thousands - of dollars to your annual revenue. Don’t let unnecessary fees eat into your profits - take action now.

FAQs

What’s the fastest way to calculate my effective processing rate?

To figure out your effective processing rate in no time, take the total processing fees you've paid over a specific period and divide that by the total transaction volume for the same timeframe. The result is a percentage that shows how much you're spending per dollar processed. Be sure to review your payout statements carefully to account for all fee components - this gives you a clearer picture of your actual costs and can help you spot chances to negotiate lower rates.

Which fees can I actually negotiate with my payment processor?

To potentially lower costs, you can try negotiating fees like interchange rates, transaction fees, and even chargeback or reconciliation expenses. Begin by carefully examining your processor's fee structure. Once you understand what you're currently paying, reach out to discuss ways to reduce those charges. Knowing your existing rates gives you a stronger position to negotiate better terms.

How can I reduce chargebacks without adding more staff time?

To keep chargebacks under control, consider using automated fraud prevention tools. These tools can monitor transactions in real-time and flag anything that looks suspicious, saving you time and effort. Another smart move is encouraging customers to opt for lower-risk payment methods, such as ACH transfers or debit cards, as these tend to have fewer disputes compared to credit cards.

On top of that, make sure your refund and dispute policies are crystal clear and easy to find. Communicating these policies upfront helps avoid confusion and reduces the chances of disputes arising. Together, these steps can significantly cut down on chargeback risks while reducing the need for manual intervention.