Secured vs. Unsecured Credit Cards: When Each Makes Sense

Secured and unsecured credit cards serve different needs, depending on your financial situation. A secured card requires a refundable deposit, making it ideal for building or rebuilding credit. In contrast, an unsecured card doesn’t need a deposit and often comes with better perks, like rewards and higher limits, but requires a stronger credit profile.

Key Takeaways:

- Secured Cards: Great for credit-building with deposits ranging from $200–$5,000. Higher approval chances but often have higher fees and interest rates.

- Unsecured Cards: Better for those with fair to excellent credit, offering rewards, higher limits, and no deposit requirement.

Quick Tip: Start with a secured card if you’re new to credit or recovering from financial setbacks. Transition to an unsecured card as your credit improves.

Here’s how to decide which type is right for you and how they compare in terms of costs, benefits, and risks.

How Secured Credit Cards Work

Security Deposit and Approval Basics

Secured credit cards operate on a straightforward concept: you provide a deposit that acts as collateral, which usually determines your credit limit. For instance, issuers might require deposits ranging from $200 to $5,000. A good example is Capital One's Platinum Secured card, which offers deposit options of $49, $99, or $200 to establish a $200 credit line [1][3].

Because the deposit minimizes risk for lenders, these cards are often easier to get approved for compared to traditional credit cards. This makes them a good option for individuals with limited or poor credit histories. Keep in mind, though, that the deposit is not used to pay monthly bills - it simply acts as security. You’ll still need to make on-time minimum payments to avoid penalties.

Rates, Fees, and Credit Building

Secured cards often come with higher costs, such as annual percentage rates (APRs) ranging from 23.89% to 29.74%, along with varying annual fees. For example, the OpenSky® Secured Visa® charges a $35 annual fee and has a 23.89% variable APR. On the other hand, the Credit One Bank® Secured card has no annual fee but comes with a higher variable APR of 29.74% [3].

The Federal Trade Commission explains:

"Secured credit cards generally (but not always) have higher annual percentage rates and higher annual fees than unsecured cards." [1]

Despite the costs, secured cards can help build credit. By reporting your payment history to the three major credit bureaus - Experian, Equifax, and TransUnion - these cards can help you establish or improve your credit score. Many users see a credit score start to develop within six months, as long as balances are paid in full [4].

Practical Benefits of Secured Cards

The credit limit on a secured card, tied to your deposit, naturally helps control spending. If you use the card responsibly, many issuers will review your account after 6–12 months. This could lead to an upgrade to an unsecured card and the return of your deposit [3]. In this way, secured credit cards act as a stepping stone, paving the way for access to better credit products in the future.

sbb-itb-5d40823

How Unsecured Credit Cards Work

No Deposit Required and Who Qualifies

Unsecured credit cards stand out because they don't require a security deposit. As personal finance writer Tim Maxwell explains:

"An unsecured credit card is simply one that doesn't require a security deposit as collateral." [7]

Instead of relying on a deposit, issuers determine your eligibility by examining your credit report, FICO score, income, and current debt levels. While approval often starts with a minimum FICO score of 580, the most competitive rates and rewards are typically reserved for those with scores of 670 or higher [5][7].

For applicants under 21, proof of independent income is a must. Those 21 and older, however, can include household income - such as a spouse's salary - when applying [2]. Students with little to no credit history may also qualify for cards designed with relaxed approval criteria [2][3]. This reliance on credit evaluation, rather than a deposit, opens the door to a variety of spending and reward opportunities.

Rates, Rewards, and Credit Limits

Unsecured credit cards often provide higher spending limits since they're not tied to a deposit. These limits can range anywhere from $200 to over $50,000, depending on your credit profile and income [7]. As of February 2026, the average APR for unsecured cards is 25.27%, which is generally lower than the rates for most secured cards [5].

Many unsecured cards also feature rewards programs, offering benefits like cash back, travel miles, or points. Additional perks may include travel insurance or extended warranties. However, annual fees can vary widely, ranging from $0 to as much as $895 [7]. These features make unsecured cards attractive but also come with varying costs and conditions.

Greater Flexibility and the Risks That Come With It

Unsecured cards offer more spending power, but that flexibility can come with risks. As Tim Maxwell points out:

"With higher credit limits comes a greater temptation to spend. You may carry a larger balance than you would with a secured card, which could cost you more in interest charges." [7]

Carrying a balance month to month leads to daily interest accrual, which can quickly add up given the high average APR. To avoid interest charges, always pay your full statement balance each billing cycle. Additionally, keeping your balance well below your credit limit is crucial. Since payment history and credit utilization together make up 65% of your FICO score [7], responsible card use is key to maintaining or improving your credit health.

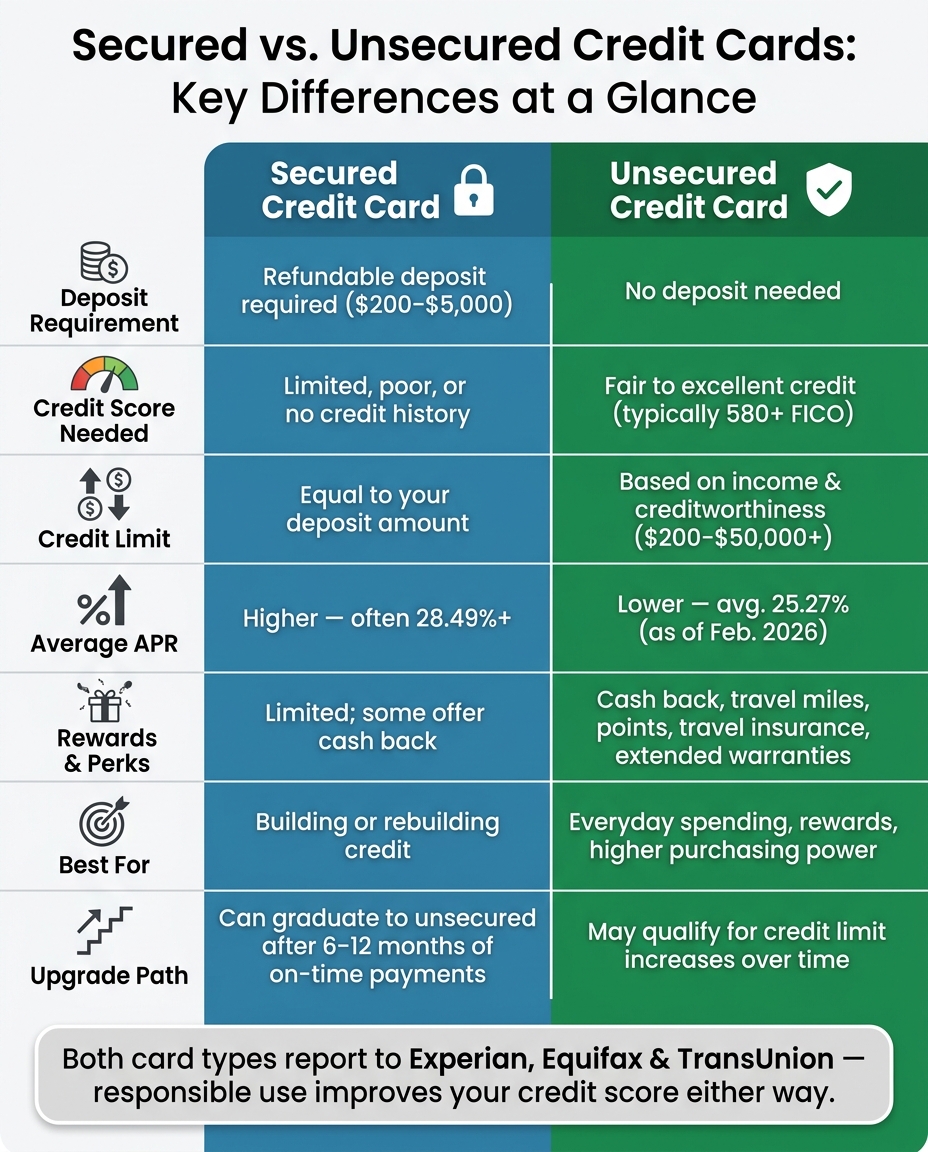

Secured vs. Unsecured Credit Cards: Differences Explained

Key Differences Between Secured and Unsecured Cards

Secured vs. Unsecured Credit Cards: Side-by-Side Comparison

Grasping the differences between secured and unsecured cards can help you pick the one that aligns with your financial goals.

Comparison Table: Secured vs. Unsecured Cards

Here’s a quick breakdown of how these two types of cards stack up:

| Feature | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Deposit Requirement | Requires a refundable deposit ($200–$5,000) | No deposit needed |

| Credit Score Range | Designed for limited, poor, or no credit history | Geared toward fair to excellent credit (typically 580+) |

| Credit Limit | Matches your deposit amount | Determined by income and creditworthiness |

| APR | Higher on average (often 28.49% or more) | Generally lower (avg. 25.27% as of Feb. 2026) |

| Fees | May include annual and late fees | May include annual and late fees |

| Rewards | Increasingly offers perks like cash back | Often provides rewards like points, miles, or cash back |

| Ideal Use Case | Best for building or rebuilding credit | Suited for everyday spending and earning rewards |

This table highlights the major distinctions. For instance, the higher APRs on secured cards emphasize the importance of comparing rates before committing [3].

As Brooke Joly, a financial writer, explains:

"The key difference between secured and unsecured credit cards is that secured credit cards require a refundable security deposit and may be available to those with a more limited credit history." [4]

Features Both Card Types Share

Despite their differences, both secured and unsecured cards have some common ground. They report your activity to major credit bureaus and include essential consumer protections like billing error dispute rights and grace periods [3][5]. These shared features mean that no matter which card you choose, responsible credit management is essential.

Keeping an eye on your transactions not only helps you manage your finances but also ensures you can catch and address any errors quickly.

Now, let’s dive into which card type might be better suited for your financial needs.

When a Secured Card Is the Right Choice

A secured card can be a smart financial tool in specific situations. Here’s when it might be the best option for you.

Building Credit for the First Time

If you’re a student, a recent immigrant, or a young adult with no credit history, you might be labeled a "thin-file" borrower - someone with fewer than five active credit accounts. This isn’t about mistakes; it’s simply because there’s not enough credit history for lenders to assess. Secured cards are designed to bridge this gap. Since your deposit reduces the lender’s risk, approval is much easier to obtain.

Once approved, consider using the card for a small recurring expense, like a streaming subscription, and always pay it off in full each month. Keeping your utilization under 10% is key. It generally takes about six months of responsible use to generate your first FICO® Score [8]. This approach sets the stage for eventually qualifying for unsecured cards.

"A secured credit card is one of the easiest and quickest ways to build credit, provided you use it responsibly." - NerdWallet [6]

For immigrants without a Social Security number, some issuers accept an Individual Taxpayer Identification Number (ITIN), making secured cards a practical option for establishing a U.S. credit profile [8].

Rebuilding Credit After Financial Setbacks

If you’ve faced financial challenges like late payments, collections, or even bankruptcy, a secured card offers a chance to start fresh. Since the deposit lowers the lender’s risk, issuers are often willing to approve applicants with less-than-perfect credit [8][3].

To rebuild successfully, focus on responsible use. Setting up automatic payments for at least the minimum amount ensures you never miss a due date, which is the most important factor in your credit score [8][3]. Paying your balance in full each month is even better, especially since secured cards often come with high APRs. Some issuers, like Discover, review accounts after eight months and may upgrade you to an unsecured card without closing your account. This keeps your credit history intact and helps improve your credit standing [9].

Keeping Spending in Check

With a secured card, your credit limit is tied to your deposit - usually between $200 and $5,000. This setup naturally limits how much you can spend [3]. For those who struggle with overspending, this structure can be incredibly helpful. Instead of seeing it as a restriction, think of it as a tool to build disciplined spending habits.

When an Unsecured Card Is the Right Choice

Once you've built up your credit with a secured card, transitioning to an unsecured card can unlock new opportunities. These cards don't require a deposit, often come with lower rates, and include perks that can elevate your overall experience.

Earning Rewards on Everyday Purchases

Unsecured rewards cards make it easy to earn cash back on the things you already spend money on, like groceries, gas, or streaming services. Take the American Express Blue Cash Preferred® Card, for instance. It offers 6% cash back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%) and another 6% on select U.S. streaming subscriptions [4]. By using a rewards card for your everyday purchases, you can accumulate valuable cash back - just make sure to pay off your balance in full each month. Otherwise, interest charges could wipe out the rewards you've earned.

Getting Access to Higher Credit Limits

With unsecured cards, your credit limit is determined by your income and credit history, not a cash deposit. If you have a strong credit profile, you might qualify for limits of $5,000 or more [10]. Compare this to secured cards, where limits are capped by your deposit, usually between $200 and $5,000 [3]. Higher credit limits can also improve your credit score by lowering your credit utilization ratio. For example, if your limit increases from $500 to $5,000 and your balance stays the same, your utilization drops significantly. Over time, responsible use of your card may even allow you to request a credit limit increase, further improving your financial standing [3].

Travel and Online Purchase Protections

Unsecured cards often come with a range of protections that secured cards typically lack. These can include travel accident insurance, car rental coverage, purchase protection for theft or damage, and extended warranties on retail items [5][3]. Whether you're traveling or making a big purchase, these benefits can save you money by covering costs that you'd otherwise have to pay for out of pocket. Before your next trip or major buy, take a moment to review your card's benefits guide - you might already have coverage you didn't know about. These added perks make unsecured cards stand out as a practical choice when deciding which card best matches your needs.

How to Choose the Right Card for Your Situation

Check Your Credit Score and Income First

Before diving into card options, take a moment to assess your financial situation. Start by checking your credit score and determining how much cash you can set aside for a potential deposit. If your score is on the lower side, secured cards are often the better choice. On the other hand, stronger credit profiles open the door to unsecured cards. Just make sure the deposit for a secured card doesn’t eat into your emergency savings.

Card issuers also evaluate your income for both secured and unsecured cards. Be ready to show you can handle monthly payments [4]. Once you’ve got a clear picture of your finances, think about what you need from a credit card to narrow down your options.

Define What You Want From a Credit Card

What’s your goal with this card? Whether you’re looking to build credit, earn rewards, or control your spending, the right card depends on your priorities.

- Building or repairing credit: A secured card is a great starting point. As American Express explains, "A secured credit card may be viewed as a building block on the way to qualifying for an unsecured credit card" [4].

- Earning rewards or accessing higher limits: If your credit qualifies, an unsecured card is often the better fit.

- Controlling spending: A secured card can help here too. Its deposit-based limit acts as a natural spending cap, keeping your budget in check.

Whatever card you choose, confirm that the issuer reports your activity to all three major credit bureaus. This ensures your responsible usage translates into a stronger credit history [3].

Using Both Card Types Together

Once you’ve evaluated your credit score and defined your needs, think about combining both card types for a more balanced approach. For example, you could use a secured card for small, recurring expenses - like a streaming subscription - to build your payment history. At the same time, an unsecured rewards card can be your go-to for larger purchases, such as groceries or travel, helping you earn perks while managing your credit [3].

Keeping your secured card open also helps maintain your credit history. If your issuer doesn’t automatically review your account for an upgrade after 6 to 12 months of on-time payments, reach out and request a manual review. Successfully upgrading to an unsecured card and getting your deposit refunded is a big step forward in strengthening your credit. By taking these thoughtful steps, you can choose a card that aligns with your financial goals and sets you up for success.

Conclusion

Deciding between a secured and an unsecured credit card boils down to one key factor: your current financial situation. If your credit history is limited or damaged, a secured card offers a safer way to build or rebuild your credit. On the other hand, if your credit is already in decent shape, an unsecured card provides access to better rates, higher limits, and rewards that can make a difference.

Here’s the main difference: secured cards require a refundable deposit - usually ranging from $200 to $5,000 - which also serves as your credit limit. Unsecured cards skip the deposit altogether, setting your limit based on your creditworthiness [3][5]. Both types report to the major credit bureaus - Experian, Equifax, and TransUnion - so responsible use of either card can help improve your credit profile.

One important thing to watch out for: both secured and unsecured cards often come with high APRs. As of February 2026, the average APR for unsecured cards is 25.27%, while secured cards can go even higher, often exceeding 28.49% [5]. The best way to sidestep these charges? Pay your balance in full every month.

Keep in mind, a secured card is meant to be temporary - a stepping stone. With consistent, on-time payments for six to twelve months, many issuers will review your account for an upgrade. This could mean refunding your deposit and transitioning you to an unsecured card [3]. That upgrade is the ultimate goal.

No matter which type of card you choose, make sure it aligns with your current financial reality - not where you hope to be in the future. Start with what works for you now, use the card responsibly, and let good habits pave the way forward.

FAQs

Will I get my secured card deposit back?

Yes, the deposit for your secured card is refundable. You'll get it back when you close the account or pay off the balance and then close the card, depending on the policies set by your card issuer. Make sure to review your issuer's terms for the exact details.

How long until a secured card helps my credit score?

A secured credit card can help improve your credit score in as little as 3 to 6 months, provided you use it responsibly. The key is to consistently pay your balance on time and keep your credit utilization low. These habits signal to lenders that you’re a reliable borrower, which can lead to positive changes in your credit profile.

When should I switch from a secured card to an unsecured card?

After 6–12 months of using your secured card responsibly - like consistently making on-time payments and boosting your credit score - it might be time to switch to an unsecured card. The exact timing will depend on your credit profile and the policies of your card issuer. Reach out to your issuer to find out if you're eligible for an upgrade.