Credit Reports Explained: What Lenders Actually See

Credit reports are like financial report cards lenders use to decide if you're a reliable borrower. They show your payment history, current debts, credit utilization, and even public records like bankruptcies. Lenders rely on this data to determine loan approvals, interest rates, and terms. Here’s what you need to know:

- Payment History (35% of your FICO® Score): Late payments can stay on your report for 7 years and heavily impact your score.

- Credit Utilization (30%): High balances on credit cards signal financial strain; aim to keep usage below 30%.

- Account History: Longer credit history helps; closing old accounts might hurt your score.

- Public Records: Bankruptcies and derogatory items like collections or charge-offs can lower your creditworthiness for years.

- Inquiries: Hard inquiries from applying for credit stay on your report for 2 years.

Lenders may see different scores than you, as they often use specialized scoring models tailored to specific loans. To improve your credit, focus on paying bills on time, keeping balances low, and disputing any errors on your report.

What Do Lenders See When They Check My Credit? | Experian Credit 101 Express

sbb-itb-5d40823

What Lenders See on Your Credit Report

Getting a handle on what lenders see in your credit report can help you better manage your finances and even secure better loan terms. Credit reports offer lenders a detailed snapshot of your financial habits, focusing on your identity, payment history, and current debts.

Personal Details Used for Identification

Your credit report starts with basic personal information like your full name, date of birth, and both current and past addresses. If you’ve applied jointly for credit, the other applicant’s name might also appear here.

This section doesn’t influence your credit score. As myFICO explains:

"Personally Identifiable Information (PII) is used to identify you... This information is not used to calculate FICO® Scores." [1]

Lenders use this data simply to make sure they’re reviewing the correct credit file. Still, it’s worth checking for accuracy. An unfamiliar address or a misspelled name could signal a mixed file or even identity theft. As Experian warns:

"Unfamiliar names or addresses may be a sign that someone stole your identity or is using some of your information to commit credit fraud." [5]

Once lenders confirm your identity, they dive into your account history to assess your financial behavior.

Account History and Payment Records

This section lists all your credit accounts - open or closed - such as credit cards, auto loans, and mortgages. It includes details like account opening dates, credit limits, balances, and payment status.

Lenders pay close attention to your payment history, as it makes up 35% of your FICO® Score, the single largest factor. [7] Even one late payment (30 days or more) can stay on your report for 7 years, impacting your score. [6]

Your payment record is often coded using MOP (Method of Payment) codes, which indicate how timely your payments are:

| MOP Code | What It Means |

|---|---|

| 0 or 1 | Paid as agreed |

| 2 | 30–59 days past due |

| 3 | 60–89 days past due |

| 4 | 90–119 days past due |

| 5 | 120+ days overdue |

| 9 | Bad debt / placed for collection |

Interestingly, accounts closed in good standing can still benefit you. These remain on your report for up to 10 years and continue to reflect positive financial behavior. [4][8]

Outstanding Debt and Credit Utilization

Beyond payment history, lenders also evaluate your outstanding debt. This section highlights your total balances and, for credit cards, your credit utilization ratio - the percentage of your available credit you’re using.

If your credit utilization is high, lenders may view it as a sign of financial strain, even if you’re making payments on time. Since utilization accounts for 30% of your FICO® Score [4], keeping balances low is key to maintaining a strong score.

After reviewing your debt, lenders also look at public records and other negative marks to gauge additional risks.

Public Records and Negative Items

Bankruptcies are the primary public records included in credit reports from the three major bureaus. [3][8][9] While tax liens and civil judgments no longer appear on these reports, they may still be accessible through other public databases.

Lenders also see derogatory items like collection accounts, charge-offs, foreclosures, and repossessions. These negative marks can significantly affect your ability to borrow, often leading to higher interest rates, stricter loan terms, or outright denials. Here’s how long these items stay on your report:

| Negative Item | Time on Report | Lender Impact |

|---|---|---|

| Chapter 7 Bankruptcy | 10 years | Severe - often leads to denial or very high rates |

| Chapter 13 Bankruptcy | 7 years | Severe |

| Late Payments | 7 years | Moderate to high |

| Collection Accounts | 7 years | High - indicates unresolved past debt |

| Charge-offs | 7 years | High - debt was never fully repaid |

| Hard Inquiries | 2 years | Low - suggests active credit-seeking |

Keep in mind that the age of a negative mark matters. For example, a charge-off from six years ago will weigh less heavily on your credit score than one from six months ago. While time doesn’t erase these blemishes, it does soften their impact over the years.

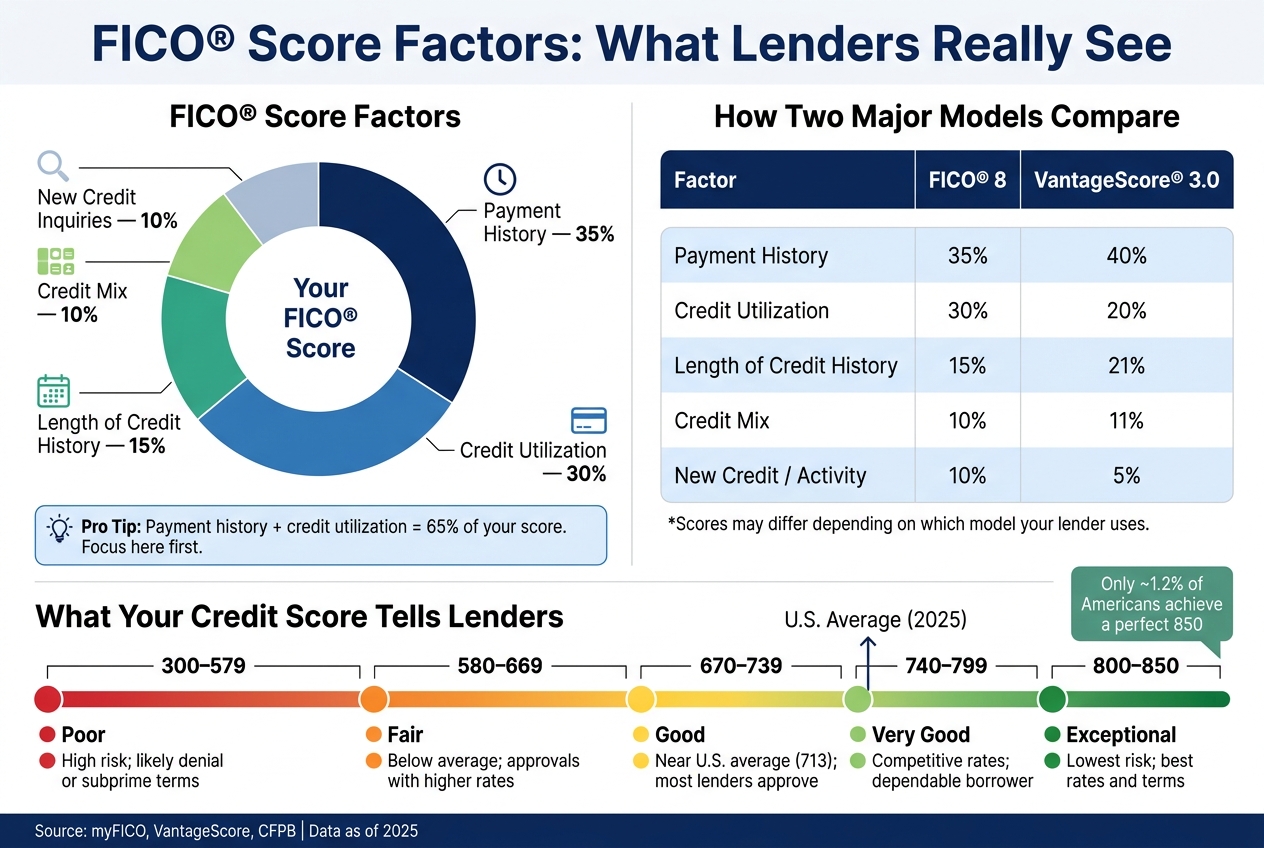

The Five Factors That Shape Your Credit Score

FICO® Score Factors: What Lenders Really See

Your credit score is built around five key elements, each with its own level of importance. These factors, derived from your credit report, help lenders assess your reliability. Knowing how they work can help you better manage your credit and secure more favorable loan terms.

Payment History (35%)

Payment history carries the most weight, accounting for 35% of your FICO® Score[4]. As myFICO explains:

"The first thing any lender wants to know is whether you've paid past credit accounts on time. This helps a lender figure out the amount of risk it will take on when extending credit." [11]

This factor tracks whether you pay on time, the severity of any late payments, and major issues like collections or bankruptcies. To keep this in good standing, consider setting up autopay so you never miss a due date.

Credit Utilization (30%)

Credit utilization - what percentage of your available revolving credit you're using - makes up 30% of your score[4]. High utilization can suggest financial strain. While keeping this under 30% is a general guideline, top scorers often aim for less than 10%. A helpful tip is to pay your credit card balance before the statement closing date, as issuers typically report balances at the end of the billing cycle[10].

Length of Credit History (15%)

This factor looks at the age of your oldest account, the newest one, and the average age of all your accounts[11]. A longer history gives lenders more data to evaluate your reliability. Closing older accounts - even those you rarely use - can negatively impact this factor by lowering your average account age and potentially increasing your utilization ratio[13][12].

New Credit Inquiries (10%)

Hard inquiries, such as those from applying for new credit, can slightly lower your score and remain on your report for two years[4]. Soft inquiries, like checking your own score, have no impact[1]. If you're shopping for a mortgage or auto loan, submitting all applications within a 14-to-45-day period ensures most scoring models treat multiple inquiries as one[4].

Credit Mix (10%)

The final factor looks at the variety of credit types you manage, such as revolving accounts (credit cards) and installment loans (like mortgages or car loans)[4]. Lenders appreciate seeing that you can handle different types of credit responsibly. However, opening new accounts solely to diversify your credit mix is unnecessary.

| Factor | FICO® 8 Weight | VantageScore® 3.0 Weight |

|---|---|---|

| Payment History | 35% | 40% |

| Credit Utilization | 30% | 20% |

| Length of Credit History | 15% | 21% |

| Credit Mix | 10% | 11% |

| New Credit / Activity | 10% | 5% |

Though the weightings differ slightly between FICO® and VantageScore® models, the overall priorities stay consistent: pay your bills on time, keep balances low, and avoid opening unnecessary accounts.

Credit Scores: What the Numbers Mean to Lenders

Your credit score boils down all the details in your credit report into a single number, giving lenders a quick snapshot of your risk level. This number, ranging from 300 to 850, plays a major role in determining the terms of any loan you apply for. As of September 2025, the average FICO® score in the U.S. stood at 713 [10]. That’s considered "Good", but it’s not quite high enough to unlock the most favorable rates.

Credit Score Ranges Explained

Each range of FICO® scores tells lenders something different about your reliability as a borrower. These ranges directly influence the interest rates and terms you’ll be offered.

| FICO® Score Range | Rating | Lender Assessment |

|---|---|---|

| 800–850 | Exceptional | Lowest risk; qualifies for the best rates and terms |

| 740–799 | Very Good | Dependable borrower; highly competitive rates |

| 670–739 | Good | Near or slightly above the U.S. average; most lenders approve |

| 580–669 | Fair | Below average; approvals possible but with higher rates |

| 300–579 | Poor | High risk; likely denial or subprime terms |

Only around 1.2% of Americans ever achieve a perfect 850 [16]. However, hitting a score above 740 can put you in a strong position with lenders, often qualifying you for some of the best rates available.

How Your Credit Score Affects Loan Terms

Your credit score isn’t just a number - it’s a key factor that determines how much a loan will cost you. Better scores mean better deals, plain and simple. As Louis DeNicola, a credit expert at Experian, explains:

"A higher score can help you get: Higher loan and credit limits, lower interest rates, [and] lower or fewer fees." [10]

Let’s look at an example. In April 2025, a borrower in Texas with a 750 credit score qualified for a 6.625% interest rate on a $400,000 30-year mortgage. Meanwhile, someone with a 650 score was offered a 7.125% rate. That half-point difference added up to $48,100 more in interest over the life of the loan [15].

Your credit score also affects how much credit you can access. A March 2026 report from the CFPB on the 2025 credit card market highlighted this disparity. Borrowers with "Superprime" scores (800+) had an average credit limit of $13,200 per card, while those in the "Deep subprime" range (579 and under) were limited to just $2,200 [14]. A lower score doesn’t just mean higher costs - it can also restrict your financial flexibility.

What You See on Your Credit Report vs. What Lenders See

Your credit report might look one way to you and another way to lenders. This difference is crucial when it comes to managing your credit effectively.

Consumer Reports vs. Lender Reports

When you check your credit report using free tools or your bank's app, you're usually looking at an educational score. As Equifax explains:

"When you check your own credit scores... what you generally see are educational credit scores, meaning they are intended to give you a close idea of your scores for informational and monitoring purposes." [17]

Lenders, however, rely on industry-specific scoring models that are tailored to the type of loan you're applying for. For instance, a mortgage lender might use an older FICO® Score version, such as FICO® Score 2 or 4, as required by regulations. Meanwhile, an auto lender could use the FICO® Auto Score, which has a range of 250 to 900, instead of the standard 300 to 850 [18]. This is why the score you see online can differ from what a lender sees.

Here’s a quick comparison of the differences:

| Feature | Consumer View | Lender View |

|---|---|---|

| Score Type | Educational (e.g., VantageScore 3.0) | Industry-specific (e.g., FICO® Auto Score) |

| Inquiries Shown | Displays both hard and soft inquiries | Hard inquiries only |

| Purpose | Informational and monitoring | Risk assessment and loan pricing |

| External Data | Limited to credit file | Includes income, assets, and collateral |

Lenders may also request a tri-merge report, which combines data from Experian, TransUnion, and Equifax. Alternatively, they might only use data from one bureau, depending on the type of loan [17]. Since not all creditors report to all three bureaus, your credit score can vary. As freelance journalist Brianna McGurran points out:

"If those reports differ, a credit score based on one report will not be identical to a score based on another. They can differ because lenders are not required to report debt accounts to all three bureaus." [18]

On top of that, delays in reporting can further complicate how your financial situation appears to lenders.

How Reporting Delays Affect Your Credit File

Your credit report is more like a snapshot than a real-time update. Creditors typically update account information monthly, which means recent changes - like paying off a large balance - might not show up right away. To ensure lenders see the most accurate picture, it’s a good idea to wait a few billing cycles before applying for new credit. As Experian explains:

"If you've recently paid down card balances to reduce your credit utilization, it may take a few billing cycles for your score to fully reflect that change." [3]

Steps to Strengthen Your Credit Profile

If you’re looking to improve your credit file and secure better loan terms, there are specific steps you can take to make your profile more appealing to lenders. These actions can directly shape how lenders perceive your creditworthiness.

Check Your Credit Reports Regularly

Begin by reviewing your credit reports from all three major bureaus: Equifax, Experian, and TransUnion. You can access these reports for free once a week through AnnualCreditReport.com [19][2]. Additionally, Equifax offers six extra free reports each year [19][2]. Since lenders might use any one of these bureaus, it’s crucial to examine all three reports.

The Federal Trade Commission emphasizes:

"The strength of your credit history also affects how much you will have to pay to borrow money." [19]

A 2024 study revealed that 27% of consumers found errors in their credit reports that could negatively impact their scores [21]. That’s more than one in four people potentially facing unfair challenges when applying for loans. If you spot inaccuracies, address them immediately to prevent them from harming your financial opportunities.

Dispute Errors and Address Negative Items

Once you’ve reviewed your credit reports, take action to dispute any inaccuracies that could hurt your score. Errors like an on-time payment marked as late, unfamiliar accounts, or incorrect balances should be challenged right away. File disputes directly with both the credit bureau and the furnisher (the bank or lender that provided the data). By law, credit bureaus must investigate disputes within 30 days, and the process is free [19][2].

To dispute effectively, send a detailed letter via certified mail, including copies of any supporting documents. Clearly outline the errors to make the investigation process smoother. If a bureau refuses to correct a verified mistake, you can escalate the issue by filing a complaint at consumerfinance.gov/complaint, which brings federal oversight into the matter [20][21].

Eric Croak, CFP and Founder of Croak Capital, highlights the importance of this step:

"Submitting a complaint to CFPB is free and takes about 20 minutes. Creditors seem to respond faster because you've now opened a federal complaint." [21]

After resolving a dispute, monitor your credit reports again in a few months to ensure the error doesn’t reappear.

Lower Your Credit Utilization and Limit New Applications

Keeping your credit utilization ratio low is one of the most effective ways to improve your credit score. Individuals with top-tier scores often maintain utilization rates below 10% [22][4][23]. According to Experian’s Jim Akin:

"Paying down high balances... can be one of the quickest ways to improve your credit scores." [4]

To lower your utilization, try paying off balances before your statement closing date so that a smaller balance is reported. You can also request a credit limit increase, which reduces your utilization ratio without additional spending [23].

When it comes to new credit, avoid applying for multiple accounts unnecessarily, as this can result in hard inquiries that may temporarily lower your score [4][23]. If you’re rate-shopping for a mortgage or car loan, aim to submit all applications within a 14-day window so they count as a single inquiry [4]. Additionally, avoid opening new accounts in the months leading up to a significant loan application - this short-term dip in your score could make a difference.

Conclusion: Taking Control of Your Credit Profile

Your credit report plays a crucial role in how lenders assess your reliability. As myFICO explains:

"Your credit report is key to your financial well-being - don't leave it to chance." [1]

Two major factors - payment history and credit utilization - make up almost two-thirds of your FICO® Score [24][1]. The good news? These are areas you can directly manage. Staying on top of payments and keeping your credit balances low are two of the most impactful habits you can adopt. This knowledge gives you the power to take meaningful steps toward improving your credit.

Beyond your credit report, lenders also consider other factors like your income, employment history, and assets [24][3]. A strong credit profile, combined with stable financials, often leads to better loan terms.

Regularly checking your credit and addressing inaccuracies promptly are essential habits for maintaining a good credit standing. You can access free credit reports from all three major bureaus at AnnualCreditReport.com, available weekly at no cost [2]. Keep an eye on your credit utilization and be mindful about applying for new credit. Over time, small, consistent efforts can lead to noticeable improvements in your credit. As Ben Luthi from Experian puts it:

"While building excellent credit takes time, focusing on consistent on-time payments, low credit utilization and responsible credit management will put you on the right path." [23]

FAQs

Which credit score will a lender use for my application?

Lenders often rely on your FICO score when evaluating your application. This score is calculated using information from your credit report, such as your payment history, amounts owed, length of credit history, new credit, and credit mix.

How fast do credit report updates show after I pay down debt?

When you pay down debt, updates to your credit report typically show up within 1–2 months. This delay occurs because lenders need to report the updated information to the credit bureaus, and then the bureaus must process and include it in your report. The exact timing depends on when your lender submits the data and how often the credit bureau updates its records.

What’s the best way to fix errors on my credit report?

To correct mistakes on your credit report, you can dispute them directly with the credit bureaus for free. Start by obtaining your free credit reports from Experian, Equifax, and TransUnion. Carefully review these reports for any inaccuracies, such as incorrect personal information or account details. If you spot an error, file a dispute with the appropriate bureau and include any necessary supporting documents. Additionally, reaching out to the creditor responsible for the error can help expedite the correction process.