Why Refund Abuse Is the New Chargeback Problem

Refund abuse is becoming a major issue for businesses, costing U.S. retailers $101 billion in 2023 alone. Unlike filing a chargeback, refund abuse happens directly between customers and merchants, making it harder to detect. Fraudsters exploit return policies using tactics like fake claims, damaged returns, or empty boxes. Social media tutorials and economic pressures are fueling this trend, leaving businesses vulnerable to financial losses and operational challenges.

Key Takeaways:

- What it is: Refund abuse involves dishonest returns or refund claims, bypassing banks and card networks.

- Why it’s growing: Social media spreads refund scams; rising costs push more people toward these schemes.

- Impact: Businesses lose revenue, face inventory issues, and strain customer service teams.

- Prevention: Tighten refund policies, monitor patterns, and train staff to spot fraud.

Refund abuse is a growing threat that requires businesses to act quickly to protect their bottom line.

Retailers turn to AI to combat growing return fraud problem

sbb-itb-5d40823

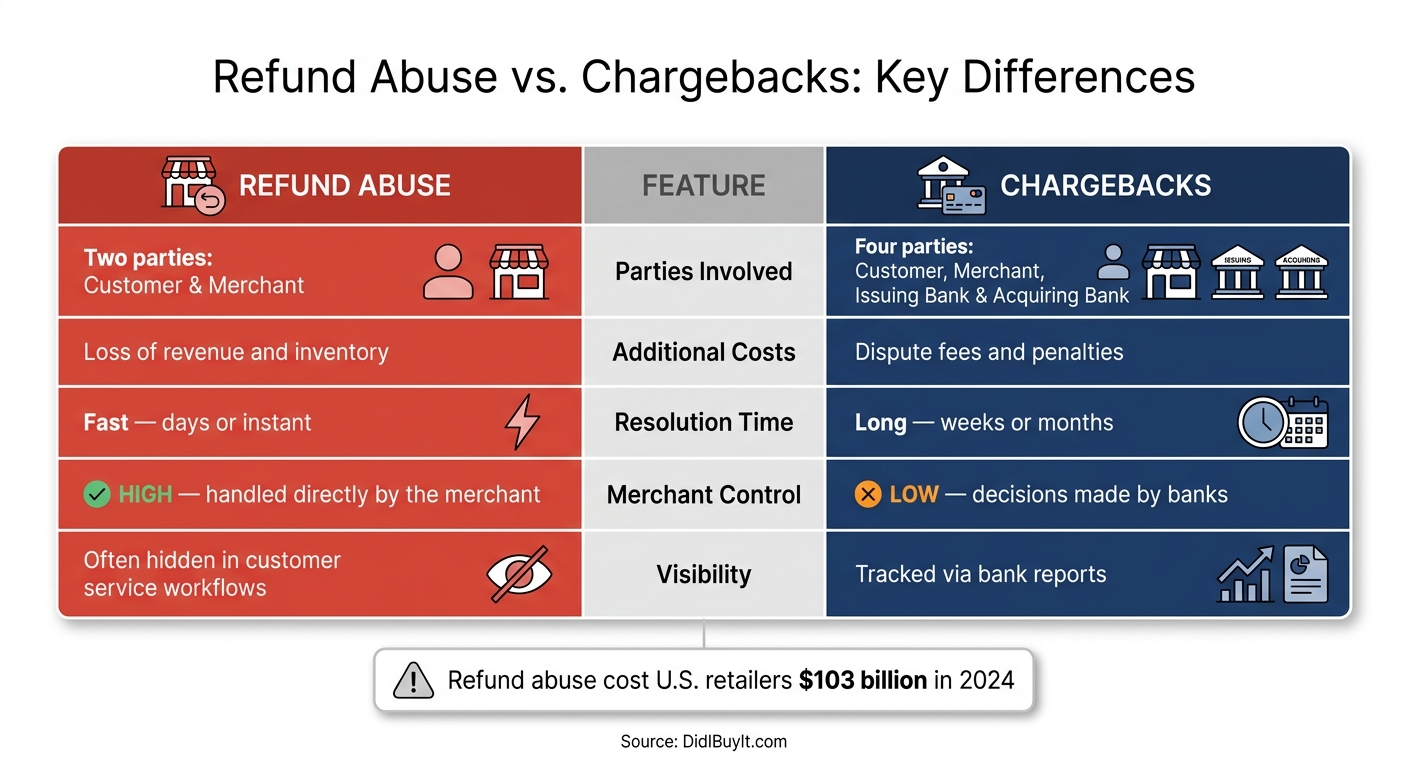

Refund Abuse vs. Chargebacks: What You Need to Know

Refund Abuse vs. Chargebacks: Key Differences Explained

What Refund Abuse Looks Like in Practice

Refund abuse comes in many forms, and some of the tactics are surprisingly creative. One example is wardrobing - where customers purchase clothing, wear it (often for a single occasion or even just for a social media post), and then return it as if it were unused. In 2025, a striking 27% of shoppers admitted to this behavior, with the number climbing to 49% among Gen Z consumers [4].

Another method is bricking, where fraudsters deliberately damage a device’s hardware or software to make it appear defective, allowing them to claim a refund. Then there’s the unusual case of dry ice returns: scammers pack a box with dry ice to match the correct weight when shipping it back. By the time the package reaches its destination, the dry ice has evaporated, leaving the box empty [1].

What’s more, refund abuse has become a business in itself. Refund Fraud‐as‐a-Service groups now operate openly, offering "menus" of fraudulent services on social media and online forums. They take a percentage of each successful refund scam [1]. Adding to the problem, some fraudsters use AI tools to create fake photos or documents to strengthen their claims.

How Refund Abuse and Chargebacks Are Similar

At first glance, refund abuse and chargebacks might seem like entirely separate issues. However, both fall under the category of fraud often referred to as friendly or first-party fraud, where customers intentionally exploit the system. The main distinction lies in how they’re processed:

- Chargebacks involve multiple parties - customer, merchant, issuing bank, and acquiring bank - and follow a formal dispute process with strict deadlines.

- Refund abuse, on the other hand, is managed directly between the customer and the merchant, with no external oversight [3].

Here’s a quick comparison to highlight the differences:

| Feature | Chargebacks | Refund Abuse |

|---|---|---|

| Parties Involved | Four (Customer, Merchant, Issuing Bank, Acquiring Bank) | Two (Customer, Merchant) |

| Additional Costs | Dispute fees and penalties | Loss of revenue and inventory |

| Resolution Time | Typically long (weeks or months) | Often fast (days or instant) |

| Merchant Control | Low - decisions are made by banks | High - handled directly by the merchant |

| Visibility | Tracked via bank reports | Often hidden in customer service workflows |

Why Refund Abuse Is Increasing

Refund abuse is on the rise for several reasons. Social media platforms like TikTok (34%) and Facebook (29%) have played a big role in normalizing these practices by hosting "refund hack" tutorials [2]. When fraud is framed as a clever trick rather than a crime, it lowers the psychological hurdle for people to engage in it.

Economic pressures are another major driver. Over half (51%) of consumers who admit to first-party fraud say the rising cost of living is a key motivator [1]. Compounding the issue, many merchants opt to issue refunds rather than risk the costs associated with fighting chargebacks, which include dispute fees, processing penalties, and even the potential loss of card processing privileges [7]. Fraudsters have quickly learned to take advantage of this preference.

"Refund/Policy Abuse and Real-Time Payment Fraud represent a fundamental shift in the fraud landscape. Refund abuse is a post-purchase attack that eats into merchant margins."

This mix of social media influence, economic strain, and merchant practices creates a vicious cycle. By making refunds easier, businesses unintentionally encourage more abuse, leading to even greater financial losses. As tactics evolve and external pressures mount, the operational and financial impact of refund abuse continues to grow.

How Refund Abuse Affects Your Business

Refund abuse doesn’t just echo the challenges of chargeback windows - it brings its own set of financial and operational headaches that can seriously impact your bottom line.

The Direct Financial Cost

In 2024, U.S. retailers lost over $103 billion to refund abuse [10]. On average, refund abuse eats up $10.30 for every $100 in returned merchandise [9]. And even when merchants recover items, the costs don’t stop there. Restocking, handling, and logistics can add up to 60% of the original price of the item [1].

But that’s not all. Returns often come with hidden expenses. Inefficient return processes tack on an extra $5 to $6 per item, covering shipping, inspections, and other handling costs [10]. Fraudulent claims about lost or damaged items also contributed to $35 billion in losses in 2024, with 10.5% flagged as fraudulent [10].

Day-to-Day Operational Disruptions

Refund abuse doesn’t just drain money - it wreaks havoc on daily operations. For instance, when fraudsters return empty boxes or swap out items, inventory systems may mistakenly log these as sellable products. This “phantom inventory” can lead to stockouts and supply chain issues [9].

Customer service teams also feel the strain. Investigating suspicious claims, validating orders, and managing returns eats up time and resources. This problem becomes even worse during peak seasons - November and December alone account for 31% of annual refund claims [5]. Overwhelmed teams often approve questionable requests just to keep up, creating opportunities for repeat abuse.

And the threat isn’t always external. In 2024, 39% of refund abuse cases involved employee collusion [3], proving that internal risks can be just as damaging as external fraud.

Long-Term Business Risks

The dangers of refund abuse go far beyond immediate financial and operational losses - they can erode your business’s stability and reputation over time.

Lenient refund policies often attract repeat offenders, especially with the rise of organized fraud rings offering “refund fraud-as-a-service” [1]. What starts as a manageable issue can quickly spiral into a systemic problem.

Refund abuse also impacts customer trust. Studies show that 62% of consumers are less likely to shop with a brand after fraud occurs, and 21% stop shopping there altogether [2].

"As disputes and chargebacks continue to rise, and first-party fraud becomes an increasingly significant part of overall dispute volume, businesses face growing operational and financial pressures. Leveraging proactive fraud prevention... helps companies reduce losses, protect revenue, and maintain long-term customer trust." - Alexander Hall, Trust and Safety Architect, Sift [2]

With nearly one in four refunded dollars tied to abusive claims [5], businesses face shrinking margins and overburdened teams. Without active measures, these challenges can quickly become unsustainable.

How to Spot Refund Abuse Early

Catching refund abuse early is crucial to safeguarding your business from this growing problem. Often, refund abuse hides within normal return patterns, making it tricky to detect without a closer look.

Warning Signs in Return and Refund Activity

One of the biggest red flags is an unusual frequency of refunds. For instance, if a customer is returning five out of every six orders while the average in that category is closer to one in ten, it’s not just bad luck - it’s a pattern that needs attention [3]. Another clue? Refund requests that consistently come in at the very last minute of your return window. This timing could signal someone deliberately gaming your policy [3].

High-value items are especially at risk. Electronics and apparel, for example, are common targets because verifying their condition remotely can be challenging. Scammers may exploit this by returning counterfeit or damaged items instead of the original product - a tactic known as "item swapping" [3][1]. Looking ahead, fraudsters are starting to use AI-generated photos and fake documents to back up their bogus refund claims, adding a new layer of complexity to the issue [1].

Organized refund abuse leaves an even clearer trail. Watch for multiple accounts that share the same device fingerprint, IP address, shipping address, or payment method. These shared details could point to a "refund cycling" operation, where scammers work together to bypass account limits [3][4]. Orders placed through VPNs, proxies, or freight-forwarding addresses are also worth a second look [3].

"A common and reliable signal of refund abuse is repeated patterns of behavior across accounts that share infrastructure, identity attributes, or device fingerprints." - Stripe Radar [3]

Tools and Metrics for Tracking Refund Abuse

Since refund abuse doesn’t go through card networks or banks, traditional chargeback data won’t help you here. Instead, you’ll need to track refund activity using specific metrics designed for this purpose.

Here are four metrics to monitor regularly:

| Metric | What It Tracks | Warning Threshold |

|---|---|---|

| Refund Rate by Cohort | Refunds by channel, category, or geography | Rates much higher than the category average (e.g., >20%) |

| Repeat Refunder Rate | Customers filing multiple claims within 90 days | More than 3 claims per account in 90 days |

| Identity Linkage | Shared device fingerprints, IPs, or payment methods across accounts | Any confirmed match across accounts |

| False Positive Rate | Legitimate claims flagged incorrectly | High manual overrides on flagged claims |

Anomaly detection is another powerful tool. By comparing a customer's refund activity to the average for their cohort - say, a 40% refund rate versus an 8% baseline - you can quickly spot irregular behavior [3]. Combine this with threshold rules, like flagging accounts with more than three claims in 90 days, to catch both one-off scammers and organized groups [3].

For high-risk or high-value claims, physical verification can add an extra layer of security. Tools like serial number scanning and comparing the weight of shipped and returned packages can help identify empty-box fraud before a refund is issued [12]. Keeping a close eye on these metrics allows you to move smoothly from detection to prevention.

How to Prevent Refund Abuse

Once you've spotted the warning signs, the next step is to take action. Protecting your business boils down to three key strategies: tightening your policies, leveraging data effectively, and equipping your staff with the right tools and training.

Tightening Your Return and Refund Policies

Start by revisiting your refund policies. Overly lenient rules can open the door to abuse. Set clear timelines - like a 30-day limit - and require the original proof of purchase for returns. For items that have been opened or used, consider offering store credit instead of cash refunds. This discourages those who repeatedly return items with no intent to keep them [13][6].

For high-value or commonly abused products, implement stricter measures. Requiring an RMA (Return Merchandise Authorization) number linked to the original order ensures each return is tracked and inspected [13]. In the case of "Item Not Received" claims - which are 25% more likely to involve abuse than other missing-item reports [5] - ask customers to submit a formal affidavit of non-receipt before issuing a refund [13][6].

Additionally, rethink universal free returns. Instead, make unlimited returns a perk for loyal customers with a proven track record. This approach not only prevents fraud but also helps safeguard your profits.

Using Data to Detect Fraud Patterns

Strong policies are a great start, but data is your best ally in enforcing them. Historical refund data can help you establish benchmarks and set up automated alerts for unusual activity.

One powerful tool here is identity linkage. By analyzing transaction data for shared details - like IP addresses, device fingerprints, billing addresses, or payment methods across accounts - you can uncover patterns that might otherwise go unnoticed [11][3]. Pair this with threshold rules, such as flagging accounts with more than three refund claims in 90 days, and pay extra attention to orders over $2,000, which are 2.5 times more likely to result in refund claims [5].

Staff Training and Process Improvements

While technology helps identify patterns, human judgment is crucial for understanding context. Your customer service team plays a vital role in this. Equip them to not only resolve claims efficiently but also recognize suspicious behavior.

"Fraud teams focus on payment fraud, while customer service teams are incentivized to resolve claims, not flag them. Refund abuse needs an owner with visibility into both sides." - Stripe [3]

Train staff to spot behavioral warning signs, such as customers who become defensive when asked standard questions about a return or those who contact different agents hoping for a different outcome [13][14]. Use verification checklists, establish clear escalation procedures for high-risk cases, and automate approvals for low-risk, low-value refunds. For flagged cases, ensure they’re routed to a manual review process [3]. Together, these steps create a strong defense that pairs well with a data-driven strategy.

How DidIBuyIt Helps You Fight Refund Abuse

Refund abuse can be a tough challenge for merchants, but DidIBuyIt steps in with a smart, AI-powered platform to make the process smoother and more effective. By combining technology with streamlined processes, DidIBuyIt helps merchants detect fraudulent refund claims and handle disputes with confidence. Here's how it works.

AI Dispute Analysis and Fraud Detection

When a refund claim is submitted, DidIBuyIt's AI gets to work instantly. It cross-checks the claim against merchant policies, bank regulations, and past cases to create a tailored action plan. By analyzing reason codes and estimating the likelihood of success, the system ensures you're prepared for the dispute. It even provides a detailed evidence checklist to make sure you have all the necessary documentation ready to go [15].

But it doesn’t stop there. The platform also simplifies how you gather and organize this documentation, saving you time and effort.

Bank-Ready Documents and Dispute Support

One of the biggest hurdles in fighting refund abuse is dealing with complicated paperwork. DidIBuyIt takes care of this by automating the creation of professional, bank-compliant documents. These documents meet the standards set by major payment networks, including Visa, Mastercard, Amex, and PayPal. Plus, data is securely encrypted to protect sensitive information.

With real-time tracking, you can monitor the status of your disputes without constantly checking in, making the process even more seamless.

Pricing and Plan Options

DidIBuyIt offers two simple, flat-fee plans so you can choose the level of support that fits your needs. Both plans are built to reduce manual work and focus on evidence-based solutions.

| Plan | Features | Best For |

|---|---|---|

| Basic Recovery | AI-driven dispute analysis, bank-ready documents, step-by-step guidance, and data encryption | Straightforward refund abuse cases on supported platforms |

| Advanced Support | Includes all Basic features, plus priority support and advanced evidence preparation | Complex or high-value disputes needing extra attention |

Whether you're dealing with routine refund claims or tackling more challenging cases, DidIBuyIt ensures you're equipped with the tools and support to succeed.

Conclusion: Take Control of Refund Abuse Before It Costs You More

Refund abuse is a growing financial problem, costing U.S. merchants an estimated $101 billion in 2023 [6]. Unlike chargebacks, which often come with clear warnings, refund abuse quietly takes advantage of internal processes, draining revenue without raising immediate alarms. Shockingly, nearly 1 in 4 refunded dollars stems from an abusive claim [5].

The longer businesses wait to address this issue, the worse it gets. Fraudsters are becoming more advanced, using tools like AI-generated fake evidence, organized refund schemes, and even social media tutorials to manipulate refund policies. This evolving threat requires equally sophisticated prevention strategies.

As first-party fraud continues to grow as a share of overall disputes, the pressure on businesses - both operationally and financially - intensifies. Tackling refund abuse not only protects revenue but also preserves customer trust in the long run. The good news? Practical solutions exist. Strategies like segmenting customers based on risk, automating claim reviews, and maintaining detailed evidence can help merchants stay ahead of these schemes. Tools like DidIBuyIt take it a step further by combining AI-driven fraud detection with bank-ready dispute documentation, ensuring you’re ready to respond when abuse occurs.

Refund abuse won’t disappear on its own. Merchants who treat it with the same urgency as chargebacks and invest in robust systems will be in the strongest position to safeguard their bottom line.

FAQs

How can I tell refund abuse from normal returns?

Refund abuse is often detectable through key warning signs like repeated returns from a single customer, claims that don’t align with their purchase history, or unusually frequent returns made shortly after buying. Unlike honest returns, refund abuse typically involves taking advantage of return policies for personal benefit - this might include false damage claims or even coordinated fraud schemes. To address this, merchants can track patterns, verify claims more thoroughly, and leverage AI tools to separate genuine returns from abusive practices.

What KPIs should I track to catch refund abuse early?

To spot refund abuse early, keep an eye on these important metrics:

- Refunds as a Percentage of Total Orders: Sudden increases, especially after holiday sales, can be a red flag.

- Frequent Refund Requests by the Same Customer: If a customer repeatedly files refund claims within a short period, it could point to abuse.

- Time Between Purchase and Refund Request: Claims made unusually quickly or after an extended delay might signal fraudulent activity.

- Inconsistent Shipping and Delivery Data: Discrepancies between courier records and refund claims should raise suspicion.

By monitoring these patterns, you can identify potential fraud and reduce financial losses.

How do I tighten refunds without losing good customers?

Clear, fair refund policies are essential for protecting your business while maintaining strong customer relationships. To tackle refund abuse, consider using AI tools to spot unusual patterns, like frequent refund requests. Keep an eye on refund trends and introduce verification steps for transactions that seem high-risk. At the same time, make sure your customers are well-informed about your policies. By combining these measures with top-notch customer service, you can safeguard your profits without losing the trust of loyal shoppers.