The Rise of Embedded Finance: What It Means for Online Businesses

Embedded finance is transforming how businesses operate by integrating financial services like payments, lending, and insurance directly into platforms where users already interact. This approach eliminates friction, boosts revenue, and strengthens customer loyalty. Here’s why it matters:

- Market Growth: U.S. embedded finance transaction value is projected to hit $7 trillion by 2026, up from $2.6 trillion in 2021.

- Business Impact: Retailers using point-of-sale credit see 20-30% higher cart conversion rates. SaaS platforms can earn 10-25% more revenue by embedding payments.

- Adoption: By 2025, 99% of tech companies will offer at least one embedded finance feature.

- Consumer Demand: Features like Buy Now, Pay Later (BNPL) reduce cart abandonment and increase average order values by up to 37%.

Businesses like Shopify and Delta Air Lines have already seen billions in revenue from embedded finance. Whether through payments, lending, or AI-driven tools, integrating financial services directly into platforms is becoming the standard for growth and retention.

Key takeaway: Embedded finance is no longer optional. It’s a must-have for businesses looking to thrive in a competitive digital landscape.

What’s Working in Embedded Finance and What Isn’t with Adyen's Head of Strategic Accounts

sbb-itb-5d40823

The Growth of Embedded Finance

Embedded Finance Market Growth Statistics 2021-2031

Market Statistics

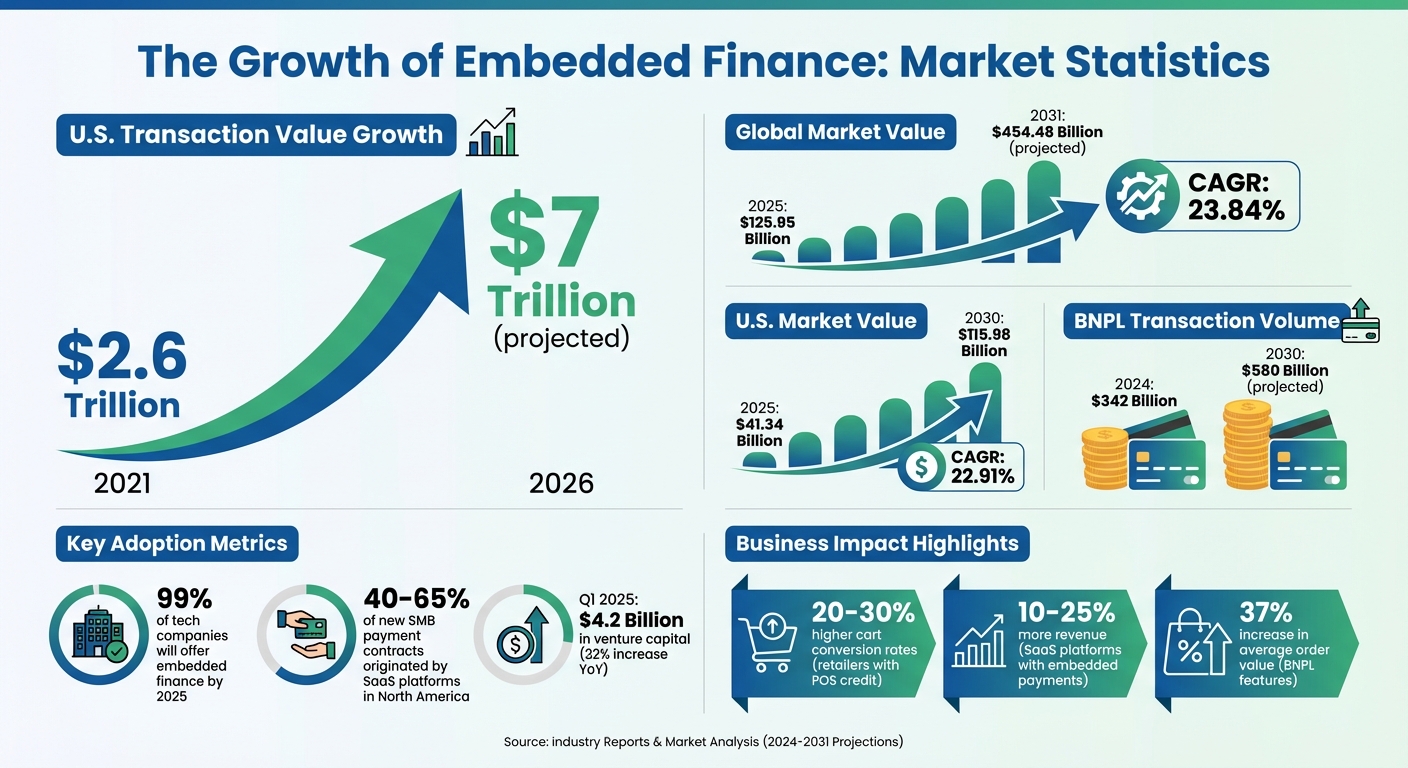

The embedded finance market is experiencing an impressive surge. Globally, projections show it climbing from $125.95 billion in 2025 to $454.48 billion by 2031, with a compound annual growth rate (CAGR) of 23.84%. In the U.S., the growth is equally striking, with the market expected to expand from $41.34 billion in 2025 to $115.98 billion by 2030, reflecting a CAGR of 22.91%.

By 2030, global embedded finance transactions are forecasted to exceed $7 trillion annually. Buy Now, Pay Later (BNPL) services alone are expected to grow from $342 billion in transaction volume in 2024 to $580 billion by 2030.

Adoption rates among technology companies are astonishing, with 99% of tech and software firms expected to offer at least one embedded finance feature by 2025. SaaS platforms are playing a pivotal role, originating between 40% and 65% of new small and medium-sized business payment contracts in North America. In Q1 2025, embedded finance startups secured $4.2 billion in venture capital, showing a 22% increase compared to the previous year.

Major partnerships are also shaping the landscape. For instance, in March 2025, JPMorgan Chase and Walmart introduced a joint embedded finance solution for marketplace sellers, integrating payments, lending, and cash management into Walmart's seller ecosystem. Similarly, in April 2025, Fiserv teamed up with Klarna to enable installment payments on Clover POS devices, marking Klarna's first nationwide in-store rollout.

These numbers highlight the momentum behind embedded finance and the factors driving its adoption.

What's Driving This Growth

Several factors are fueling the rapid adoption of embedded finance. One major driver is API-first banking, which allows non-financial companies to offer banking services without the need to build complex systems or obtain banking charters. This innovation alone is expected to contribute 5.8% to the U.S. market's long-term CAGR.

Changing consumer behavior is another critical factor. In healthcare, for example, 79% of users prefer a unified digital platform to pay their bills, and 72% would switch providers for such a seamless experience. The demand for "invisible" finance - where payments and credit are seamlessly integrated into apps - has been shown to reduce cart abandonment and improve conversion rates. Frictionless checkout alone is projected to add 3.9% to short-term CAGR growth.

Regulatory shifts are also playing a role. The CFPB's Section 1033 rule is standardizing data sharing, making it easier for software firms to access consumer account information. This is expected to add 4.1% to long-term growth. Additionally, artificial intelligence is becoming central to embedded finance, powering real-time fraud detection, automated underwriting, and personalized financial offers.

The business-to-business (B2B) sector is growing quickly as well. Although consumer adoption still accounts for 65.1% of the U.S. market, B2B adoption is expanding at a CAGR of 25.71% as companies digitize tasks like accounts payable and supplier credit. A notable example is ITS Logistics' "QuickPay" tool, introduced in 2024, which approved 1,000 carriers and saved an average of $0.45 per gallon on fuel by leveraging float and credit products.

These factors not only explain the market's rapid growth but also demonstrate the tangible benefits embedded finance offers to businesses.

"Embedded finance is not just an enhancement - it is becoming the standard way digital commerce functions."

Benefits of Embedded Finance for Online Businesses

New Revenue Streams

Embedded finance opens up fresh ways for businesses to generate income beyond their primary sales. By integrating financial services, platforms can earn transaction fees through interchange - small percentages from card transactions handled by financial infrastructure providers - and gain additional revenue from lending products like inventory financing or working capital loans via interest and service fees.

The numbers speak for themselves. Platforms that offer embedded lending often experience 15% to 25% higher conversion rates at checkout. Take Bella & Duke as an example: after introducing embedded credit options through Stripe in 2023, the company saw a 37% increase in average order value. This setup allowed customers to pay in installments while the merchant received full payment upfront.

The potential for growth is immense. By 2026, embedded finance transactions are projected to make up 10% of all financial transactions in the U.S., amounting to approximately $7 trillion. In the B2B payments sector alone, these transactions are expected to grow from $0.7 trillion in 2021 to $2.6 trillion by 2026.

Consider Shopify's success: in March 2023, the company reported $1.1 billion in revenue from embedded financial services, nearly tripling its software-only revenue of $384 million, which grew at a slower pace of 11% year-over-year. Another example is Delta Air Lines, which, in 2025, earned $8.2 billion from its American Express co-branded card program - representing over 13% of its total annual revenue of $63.4 billion.

Financial services also enable businesses to charge premium prices and increase recurring revenue. In fact, 88% of companies using embedded finance reported higher customer engagement, while 85% noted it helped them attract new customers. These benefits naturally strengthen customer loyalty and drive long-term growth.

Better Customer Retention

Embedded finance doesn’t just boost conversions - it also fosters stronger customer relationships. By integrating payments, lending, and other financial services directly into a platform, businesses eliminate unnecessary friction, making it easier for customers to stay put. This seamless experience turns the platform into a vital part of their operations.

Once customers rely on these built-in financial tools, switching to a different platform becomes a hassle. They would need to rebuild workflows, transfer financial data, and train employees - making the idea of leaving far less appealing.

"Sometimes the product that wins isn't the one with the most features - it's the one that removes the most friction." - Finix

Embedded finance also strengthens retention through contextual lending. Unlike traditional loans that rely solely on credit scores, embedded lending uses real-time data like sales history, order frequency, and return rates to make instant credit decisions - often approving users in under 30 seconds. Features like Buy Now, Pay Later and point-of-sale financing make products more affordable, attracting a wider audience and reducing cart abandonment.

Data-Driven Decision Making

Beyond revenue and retention, embedded finance provides businesses with valuable insights through integrated financial data. This data includes cash flow trends, purchasing behaviors, payment preferences, and credit usage, helping businesses better understand their customers.

Such insights lead to faster, more informed credit decisions. Platforms can analyze sales patterns, order histories, and return rates to approve credit instantly while simultaneously monitoring transactions for fraud. This streamlined access to data not only supports lending but also enhances security. For instance, a construction company facing seasonal cash flow challenges might receive tailored financing exactly when it’s needed.

"SaaS providers have access to real-time cashflow data allowing them to underwrite more thoughtfully and... they are well-positioned to cater to previously underserved SME niches." - BCG

How Businesses Use Embedded Finance

Embedded Payments

Embedded payments streamline the checkout process by processing transactions directly within a platform using APIs. This eliminates the need for customers to navigate to external payment gateways, keeping the entire experience within the app or site - whether it’s a marketplace, SaaS dashboard, or mobile app. By reducing checkout friction, online retailers have reported 20% to 30% higher conversion rates.

"Embedded payments aren't just payments inside software. They're software turning money movement into a product." - Alex Johnson, Fintech Takes

Take Walmart, for example. In 2026, the retail giant partnered with JPMorgan Chase to embed banking and cash management tools into its online marketplace. This allowed third-party sellers to accept payments and manage cash flow directly on the platform. Similarly, Klarna doubled its quarterly transaction volumes by early 2026 through its use of Marqeta's embedded technology, a partnership that began in 2019.

Modern embedded payment systems go beyond simple transactions. They can handle intricate workflows like escrow services, multi-party payment splitting, and instant payouts for sellers. These advanced features not only simplify operations but also pave the way for businesses to integrate financing solutions directly at the point of sale.

Embedded Lending and Buy Now, Pay Later

Embedded lending takes customer convenience to the next level by offering financing options directly at the point of sale. Unlike traditional credit checks, these solutions often rely on real-time data. For instance, Wolt Capital introduced pre-approved financing within its merchant dashboard across 20 markets. With a simple three-click onboarding process and payouts available within minutes, the program achieved an impressive 85% merchant return rate for additional financing and an NPS score exceeding 80.

Another example is Pillow Cube, which implemented Shop Pay Installments in June 2025. This feature accounted for 6.5% of the company’s total gross merchandise value, while also boosting average order values.

"We integrated financing directly into the Boatzon marketplace because we realized boat buyers didn't want to leave the site to get approved elsewhere... This removes friction from the buying process and converts browsers into buyers at significantly higher rates." - Michael Muchnick, Founder, Boatzon

Repayment options are often designed to be flexible, with payments automatically deducted as a percentage of future sales. This structure allows businesses to align repayments with their cash flow. Notably, global Buy Now, Pay Later (BNPL) payments are projected to exceed $560 billion by the end of 2025.

AI-Powered Dispute Resolution

Efficient payments and lending are further supported by AI-powered dispute resolution tools, which ensure any issues are addressed quickly to maintain a smooth customer experience. These tools use card-network alerts to identify potential disputes, giving businesses a 24-hour window to resolve them before they escalate.

Platforms like DidIBuyIt automate the chargeback and refund process for online businesses. By using AI to analyze disputes, they generate professional, bank-ready documents and provide step-by-step guidance. Some systems even auto-refund transactions that meet specific criteria, such as being below a certain price threshold, helping to prevent disputes from escalating into formal chargebacks.

These tools not only protect businesses from chargeback fees and money holds but also minimize the risk of processor account restrictions. Setting up automated dispute alerts can be surprisingly quick, taking as little as 12 hours for Ethoca/CDRN and approximately 7 business days for RDR.

How to Implement Embedded Finance

Partner with SaaS Providers

Building financial infrastructure from scratch isn’t necessary for most online businesses. Banking-as-a-Service (BaaS) providers and specialized SaaS platforms offer ready-to-use APIs that handle essential functions like payment processing, lending, and dispute management. The trick is finding a partner that fits your business model and growth goals.

You can launch quickly using hosted integrations or opt for a white-labeled interface to maintain your branding. Before committing, thoroughly vet your BaaS partner’s regulatory compliance and financial stability - this helps avoid risks tied to past middleware collapses.

Take platforms like DidIBuyIt, for example. They showcase how SaaS tools can simplify financial workflows. By integrating AI-powered dispute resolution, you can manage chargebacks and refunds without building that technology yourself. It’s also wise to prioritize providers that offer tokenization via hosted payment fields. This ensures your platform doesn’t handle raw card data, significantly easing the burden of PCI compliance.

Once you’ve chosen a partner, make sure your compliance and security measures are solid.

Compliance and Security Requirements

Embedded finance operates on a shared responsibility model. While your BaaS partner holds the banking licenses, you’re still responsible for critical compliance elements like customer onboarding, fraud detection in the user interface, and addressing complaints. New regulations also need attention. Starting April 2026, CFPB rules will require free consumer access to financial data while limiting retention periods. Additionally, Nacha rules effective March 20, 2026, mandate risk-based processes to monitor fraudulent ACH "credit-push" entries.

Your platform must comply with PCI DSS for payment security and the Gramm-Leach-Bliley Act (GLBA) for financial privacy, along with state laws like the CCPA. Failing to meet PCI DSS standards can lead to fines from acquiring banks, ranging from $5,000 to $100,000 per month. To streamline compliance, incorporate automated KYC (Know Your Customer) and AML (Anti-Money Laundering) processes into your onboarding systems, ensuring you meet Bank Secrecy Act requirements.

Strong compliance and security measures aren’t just about avoiding penalties - they also build customer trust, which is essential for success in embedded finance.

"Regulators want proof that controls operate inside transaction flows and AI-driven systems before harm occurs." - Zahra Timsah, CEO, i-GENTIC AI

Start Small and Scale Up

Once you’ve secured the right partner and compliance framework, start by solving your most immediate financial challenges. Payments are often the easiest entry point into embedded finance, so begin there before tackling more complex areas like lending or insurance. Pinpoint where users face financial friction in their experience and choose a solution that addresses it. For instance, if abandoned carts are a problem due to limited financing options, consider embedding a Buy Now, Pay Later feature. If disputes are consuming resources, start with automated chargeback management.

Test your solution with a small user group to ensure it works effectively. Keep in mind that BaaS setup costs for full banking products typically range from $50,000 to $200,000, with monthly platform fees between $1 and $5 per account. Once your model proves successful, you can expand into other areas like embedded lending, insurance, or even business banking services.

Conclusion

Embedded finance is transforming the way online businesses operate. With market transactions climbing steadily, the trend is impossible to ignore. Businesses that embed financial services into their platforms experience 20% faster growth and 70% lower churn, compared to those that don't.

By integrating services like payments, lending, or dispute resolution, companies create higher switching costs, which in turn strengthen customer loyalty. As InvestSuite aptly puts it, "Embedded finance may become the default architecture for financial distribution by the end of the decade, forcing incumbents to adapt or cede ground".

The good news? Entry barriers are minimal. Businesses don't need to build banking infrastructure from the ground up or navigate regulatory complexities alone. Tools like DidIBuyIt show how specialized solutions - such as AI-driven dispute resolution - can address specific challenges without requiring expertise in financial services. Whether it's reducing cart abandonment with Buy Now, Pay Later options or improving chargeback management, the technology to deploy these solutions is readily available and can be implemented in weeks.

The data makes it clear: embedded finance isn't just an optional feature - it’s a strategic necessity. With obvious benefits and relatively low hurdles to entry, now is the time to act. Start small by addressing a specific pain point, like checkout friction or cash flow issues, and expand from there. The businesses thriving in 2026 are those embedding finance into their platforms today, learning and evolving as they go.

With 97% of online marketplaces already offering at least one embedded finance product, the real challenge is how quickly you can adapt to stay competitive in this rapidly evolving landscape.

FAQs

What’s the fastest embedded finance feature to launch?

Embedded payments are often the quickest embedded finance feature to roll out. With the help of pre-built components or APIs, businesses can implement these systems in just a few weeks. This streamlined process makes embedded payments an efficient first step for companies aiming to integrate financial services without delay.

How do I stay compliant when I embed payments or lending?

To ensure compliance, it’s crucial to follow US regulations, establish solid risk management practices, and collaborate with licensed financial institutions. Incorporate compliance tools within your platform to track transactions and identify any unusual activity. Keep up with regulatory updates and seek advice from legal professionals to stay aligned with changing laws. These efforts safeguard your business and build trust with your users.

What KPIs should I track to prove embedded finance ROI?

To gauge the ROI of embedded finance, focus on tracking KPIs that showcase both financial outcomes and customer engagement. Key metrics to watch include transaction volume, customer lifetime value (LTV), and adoption rates for features like buy now, pay later (BNPL). Additionally, keep an eye on conversion rates, reductions in payment friction, and customer satisfaction scores - these provide insight into user experience improvements and loyalty. For B2B businesses, metrics like average order value and cash flow improvements are also essential to evaluate performance.