How Open Banking APIs Are Changing Customer Onboarding

Open Banking APIs are transforming how financial institutions onboard customers. Here's why they matter:

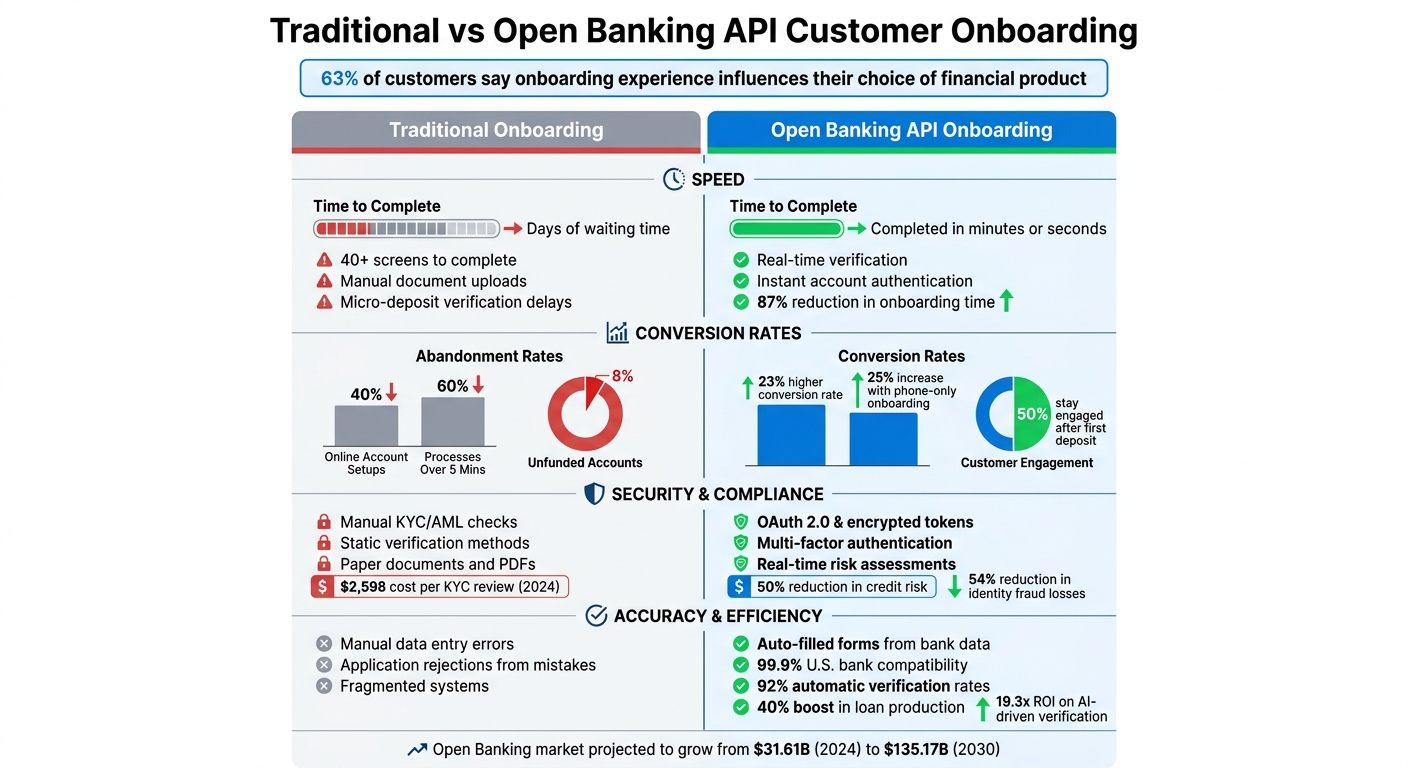

- Faster Onboarding: Traditional processes with 40+ screens and days of waiting are replaced by API-driven methods, completing tasks in minutes or seconds.

- Improved User Experience: APIs enable pre-filled forms, real-time account verification, and biometric authentication, reducing drop-off rates (60% of users abandon processes over five minutes).

- Enhanced Security: OAuth 2.0, encrypted tokens, and multi-factor authentication ensure data is accessed securely with customer consent.

- Automated Compliance: APIs streamline Know Your Customer (KYC) and Anti-Money Laundering (AML) checks by accessing bank-verified data, cutting costs and manual effort.

- Personalization: Real-time financial data allows businesses to tailor services, boosting engagement and retention.

These APIs are reshaping the U.S. market by meeting consumer demand for seamless digital experiences. With innovations like AI-powered automation and embedded finance, the future of onboarding is faster, safer, and more tailored than ever.

Traditional vs Open Banking API Customer Onboarding Comparison

How to open and fund an account using the US Open Banking APIs

sbb-itb-5d40823

How Open Banking APIs Simplify Identity Verification and Data Sharing

Open Banking APIs have transformed the way businesses handle identity verification and data sharing, making the process faster and more efficient for everyone involved.

Instead of relying on outdated methods like manually uploading documents, these APIs connect directly to a customer’s bank - a trusted source of financial identity data. This means customers no longer need to provide physical documents. Instead, they can authenticate themselves in seconds using their bank login credentials.

Here’s how it works: Customers are securely redirected to their banking app, where they can log in, often using biometric verification like fingerprint or face ID. Since banks already conduct thorough Know Your Customer (KYC) checks, businesses can access pre-verified data - like names, addresses, phone numbers, and email addresses - without requiring customers to fill out forms. This creates a faster and smoother signup process.

Security is prioritized at every step. Open Banking APIs use OAuth 2.0 and encrypted tokens to ensure that only the specific data a customer consents to share is accessed. Many APIs also use single-use tokens for added security during onboarding. Strong Customer Authentication (SCA) adds another layer of protection by requiring multi-factor verification, such as something the user knows (a PIN), something they have (a mobile device), or something they are (biometrics). Andre Reina, Group Product Manager at TrueLayer, highlights the benefits:

Open banking can give you that permissioned, direct and secure connection to the customer's bank. It avoids things like having to ask someone to scan and upload their bank statements, which is both insecure and a pain for customers.

Instant Account Authentication

With Open Banking APIs, verifying account ownership happens in real time. This eliminates the delays of traditional methods, like waiting for micro-deposits to clear. When a user connects their bank account, the API instantly confirms ownership and retrieves current balance details, completing the process in seconds.

This speed has a direct impact on business performance. Platforms using instant bank account verification report a 23% higher conversion rate compared to older methods, showing how faster verification can enhance the onboarding experience. Moreover, leading API providers now support 99.9% of U.S. banks and credit unions, offering broad compatibility. For example, in February 2023, Tiger Brokers UK implemented TrueLayer’s Signup+ solution, which combined bank-sourced identity verification with open banking data. This streamlined KYC-compliant onboarding and initial deposits into a single flow, cutting down onboarding time and boosting signup conversion rates.

App-to-app authentication further simplifies the process. Customers are redirected from a merchant app to their banking app for biometric approval and then returned to complete their signup - all within seconds. This approach is replacing less secure methods like screen scraping, pushing the U.S. market toward regulated, API-based data sharing.

Auto-Filled Applications Using Bank Data

Open Banking APIs go beyond verification by simplifying applications through auto-filled forms.

These APIs pull verified data directly from bank records to populate application fields automatically. Instead of manually entering details like account numbers, addresses, or contact information, customers authenticate with their bank, and the system fills in the required fields - such as name, address, date of birth, and phone number - on their behalf.

This automation reduces errors and minimizes customer drop-off, as users no longer face the frustration of repetitive data entry. It also cuts down on application rejections caused by mistakes. Adebayo Familusi, CEO of Remitise, explains the value:

By obtaining customer data sourced from their bank, Signup+ streamlines the onboarding process and saves time and resources for our company and our customers.

Standardized API responses provide essential details like full name, account type, and contact information. Some APIs even include identity risk scores based on activity patterns, helping businesses identify potential fraud during account setup. By combining speed, accuracy, and security, Open Banking APIs transform onboarding into a seamless experience that keeps customers engaged from the start.

Automating KYC and AML Compliance Processes

Open Banking APIs are changing the game when it comes to regulatory compliance, particularly for Know Your Customer (KYC), Know Your Business (KYB), and Anti-Money Laundering (AML) checks. These APIs replace outdated, manual processes by providing direct access to bank-verified data. This eliminates the need for unreliable PDFs or scanned documents, streamlining the entire process.

But these APIs do more than just verify identities. They can also analyze the Source of Funds (SoF) by reviewing historical transaction data, which helps businesses meet AML requirements and identify suspicious activities early on. For business onboarding, KYB processes can integrate directly with official registries, instantly pulling company and administrative information. This shift is critical, especially as the cost of a single KYC review globally hit $2,598 in 2024 - a 17% jump from 2022.

Take Diligent AI, for example. In April 2026, this fintech infrastructure company leveraged Open Banking APIs to automate KYB and merchant onboarding in Italy. Using IT-start and IT-full endpoints to access the Italian business registry, Diligent AI instantly identified about 70% of analyzed companies. This straight-through processing reduced manual work, cut operational costs, and allowed banks and payment service providers to onboard clients faster. The benefits extend beyond onboarding, enabling real-time risk management as well.

Real-Time Risk Assessments

Open Banking APIs excel at real-time risk analysis, offering access to detailed transactional data for continuous monitoring. This approach not only strengthens compliance efforts but also eliminates delays during account setup. Unlike traditional methods that rely on outdated, static checks, these APIs provide ongoing monitoring of financial behavior for up to 90 days in the UK and 180 days in the EEA.

This real-time capability is especially useful for flagging anomalies, such as frequent transactions just below reporting thresholds or activity tied to high-risk jurisdictions. Features like transaction enrichment further enhance the process by categorizing spending and standardizing merchant names, enabling automated systems to detect irregularities more effectively. The result? More accurate risk scoring, allowing compliance teams to make faster, better-informed decisions without the need for manual reviews.

Faster Onboarding Times

The enhanced risk assessments provided by Open Banking APIs directly lead to quicker onboarding. While traditional KYC processes can drag on for days or even weeks, Open Banking APIs can complete verification in mere seconds or minutes. And speed matters - a lot. Around 60% of consumers will abandon an account setup or loan application if it takes longer than five minutes.

By automating data retrieval and verification, businesses can significantly reduce customer drop-off rates, onboard more clients, and still maintain strict compliance standards. Summer Xu, COO of UK business at Tiger Brokers, highlights this advantage:

By shortening the time it takes to onboard a customer, and making deposits and withdrawals simple, Signup+ has the potential to improve signup conversion rates and control the cost per acquisition.

The combination of speed and precision gives businesses a competitive edge. They can lower operational costs while delivering a smoother, more efficient customer experience.

Creating Personalized and Frictionless User Experiences

Open Banking APIs have revolutionized the onboarding process, turning it into a customized experience that aligns with each customer's financial situation. By leveraging real-time data, businesses can create tailored interactions right from the start. High abandonment rates in 2021 underscore how critical it is to offer fast and efficient onboarding processes.

When manual data entry is removed, customer retention improves significantly. In fact, half of new customers stay engaged after making their first deposit. This shows that speed and simplicity aren't just conveniences - they're essential for building trust and delivering a smooth experience. Personalization, supported by real-time insights, is now a cornerstone of modern onboarding.

Behavior-Based Profiling for Custom Services

Open Banking APIs unlock detailed transaction data, offering a window into spending patterns, cash flow, and income consistency. This information fuels machine learning models that go beyond traditional rules-based systems, using behavioral data to segment customers more effectively. Data enrichment tools further enhance this process, transforming raw data into over 4,500 actionable financial attributes. The result? Businesses can create real-time, in-depth financial health profiles.

Take the example of Algoan, a French credit expert that launched an API-driven solution in 2018. By integrating real-time bank transaction data into lenders' workflows, Algoan has helped reduce credit risk by 50% while boosting loan production by 40% and cutting processing costs.

This use of behavioral insights doesn't just refine customer profiles; it also complements faster verification and smoother onboarding processes. Together, these improvements have a direct impact on conversion rates.

Improved Conversion Rates Through Simplified Processes

Lengthy setups are a major turnoff, with about 60% of consumers abandoning them midway. Open Banking APIs fix this by auto-filling forms with bank-provided data, eliminating the need for manual input and speeding up onboarding. This approach helps customers complete the process quickly, increasing conversion rates.

Nationwide, a UK building society, tackled a similar issue in 2022. They found that 8% of new savings accounts remained unfunded. By embedding an Open Banking–powered payment initiation step into the account confirmation screen, customers could fund their accounts instantly during onboarding. This integration dramatically reduced the number of unfunded accounts.

Adebayo Familusi, CEO of Remitise, highlighted the broader benefits of such solutions:

By obtaining customer data sourced from their bank, Signup+ streamlines the onboarding process and saves time and resources for our company and our customers. This improves the overall customer experience and increases new user conversion by removing manual data entry.

And it matters - 63% of customers say the onboarding experience plays a key role in their decision to choose a financial product. When businesses simplify processes and offer personalized experiences using Open Banking APIs, they create trust and loyalty right from the first interaction.

Practical Applications of Open Banking APIs

Open Banking APIs are changing the game for financial platforms in the U.S., offering faster, more efficient ways to onboard customers. From speeding up verification to enhancing user satisfaction, these APIs are making a noticeable difference. Let’s dive into some real-world examples to see how they work in practice.

Case Study: DidIBuyIt's Fast Dispute Recovery Onboarding

DidIBuyIt uses Open Banking APIs to simplify its dispute resolution process during signup. Instead of tedious manual steps, users log in with their bank credentials to verify accounts instantly. This process automatically fills in key details like names, phone numbers, addresses, and emails, cutting down on errors and saving time. Real-time balance checks also confirm if users have enough funds. By skipping manual data entry and micro-deposit verifications, DidIBuyIt allows users to focus on resolving their disputes faster.

And it’s not just DidIBuyIt - other major platforms are also reaping the rewards of Open Banking APIs.

Examples from Major US Platforms

- Plaid: A leader in Open Banking, Plaid connects over 100 million American adults to their bank accounts via Plaid Link. Its Layer product takes things further by enabling phone-only onboarding. Users can sign up with just a phone number, reducing onboarding time by 87% and increasing conversion rates by up to 25%.

- Dwolla: By integrating Plaid through its Exchange Sessions API, Dwolla simplifies bank-to-bank payments with instant account verification. This speeds up the process and makes onboarding smoother.

- Trustly: Trustly's tools - Connect, Insights, and ID - use bank-grade data to automate KYC and AML checks. This eliminates the hassle of micro-deposits and manual document reviews, reducing friction while staying compliant. Additionally, Plaid’s Identity API adds another layer of security by cross-checking user-provided information with bank records.

These applications highlight how Open Banking APIs are transforming onboarding processes, making them faster, more accurate, and less stressful for users.

What's Next for Open Banking in Customer Onboarding

Open Banking APIs are evolving at a rapid pace, with AI-powered automation, embedded finance, and advanced fraud prevention leading the way. These innovations are reshaping customer onboarding by making it faster, more secure, and accessible to a broader audience.

AI is already revolutionizing identity verification and risk assessment. For instance, in April 2026, Customers Bank announced a partnership with OpenAI, aiming to become "AI-native" by the end of 2026. Currently, 75% of their team uses AI tools to streamline tasks like document collection and account setup. Sam Sidhu, President and CEO of Customers Bancorp, shared:

This strategic collaboration with OpenAI gives us the frontier models, engineering expertise, and ability to co-create a roadmap toward becoming an AI-native bank. By the end of 2026, our bankers will spend more of their time on the work that creates value for clients.

The impact of AI in banking is already measurable. One digital bank saw its automatic verification rates climb from 79% to 92% after adopting AI-driven identity verification. This change reduced identity fraud losses by 54% and boosted annual value by $24 million - a return on investment of 19.3x.

Embedded finance is also opening doors for underserved communities. By integrating banking services into platforms like retail websites and ride-sharing apps, real-time transaction data is used to approve applications, bypassing traditional credit scores. This approach benefits gig workers and those with limited credit histories, enabling faster approvals. The global open banking market is projected to grow from $31.61 billion in 2024 to $135.17 billion by 2030, reflecting a 27.6% annual growth rate. The CFPB’s Section 1033 rule is accelerating this trend by formalizing consumer data rights and eliminating outdated practices like screen scraping.

Fraud prevention is becoming smarter with AI-driven behavioral biometrics. These systems analyze factors like typing speed and navigation patterns to detect fraud in real time. Yigit Yildirim, SVP of Data & AI at Socure, explains:

The fraud prevention landscape has undergone a revolutionary shift, moving from fragmented, static systems to a unified, real-time approach that offers a comprehensive view of customer identity.

With an estimated 2.5 million synthetic identities currently in U.S. bank accounts, these advancements are critical for safeguarding both consumers and businesses.

Looking ahead, Open Banking APIs are set to handle even more of the onboarding journey, from automated risk assessments to personalized product recommendations. As AI becomes more sophisticated and embedded finance gains traction, onboarding will continue to become faster, safer, and more inclusive for Americans.

Conclusion

Open Banking APIs have revolutionized customer onboarding by transforming outdated, error-prone manual processes into fast, bank-verified data sharing. Tasks that once required manual document uploads or micro-deposit verifications, stretching onboarding times, are now completed in minutes or even seconds. This improvement addresses a major issue: about 60% of consumers abandon account setups or loan applications if the process drags on too long.

Speed isn't the only benefit. These APIs have also strengthened compliance by enabling real-time KYC (Know Your Customer) and AML (Anti-Money Laundering) checks, reducing both risk and administrative effort. The impact is clear: Open Banking data has contributed to a 50% drop in credit risk and a 40% boost in loan production. Faster processes are proving to be more secure as well.

On top of security, personalization has reached new levels. By analyzing real-time transaction data, financial institutions can tailor offerings from the start - whether it’s personalized credit options or budgeting tools based on actual spending habits. This dynamic insight goes far beyond what static credit reports can provide.

The results speak for themselves. For instance, in 2022, the UK’s Nationwide integrated Open Banking-powered payment initiation directly into its account confirmation screen. This step significantly reduced the 8% drop-off rate caused by unfunded accounts. Similarly, platforms now use these APIs to auto-fill forms, instantly verify user identities, and remove the friction that leads to 4 in 10 customers abandoning online account setups.

For DidIBuyIt, these advancements are shaping the future of customer onboarding. By leveraging API-driven tools, they provide an onboarding experience that is not only secure and fast but also highly personalized for their users. As automated systems and embedded finance continue to grow, Open Banking APIs are becoming an essential part of the process. The future of financial services is heading toward a world where opening accounts, applying for loans, or accessing new services feels as effortless as shopping online - secure, tailored, and hassle-free.

FAQs

Is it safe to connect my bank account during onboarding?

Yes, linking your bank account during onboarding is typically safe when secure APIs are involved. These APIs use encryption and advanced security protocols to protect your financial information. With these measures in place, your account details remain protected throughout the process.

What data can a company access from my bank, and for how long?

When a company uses Open Banking APIs to access your bank data, they generally retrieve information such as your account balance, transaction history, account holder details, and occasionally your account number. This allows them to securely confirm your identity and assess your financial status.

Your data is only accessed for the time necessary to complete the verification or provide the service, and always with your explicit consent. Strict regulations are in place to protect your privacy and ensure the data isn't used beyond the agreed purpose.

What if my bank isn’t supported or the connection fails?

If your bank isn’t supported or the connection doesn’t work, Open Banking APIs might not be able to access your data. When this happens, you can rely on alternatives like manual onboarding or other verification methods to finish the setup. These solutions help ensure you can move forward without any interruptions.