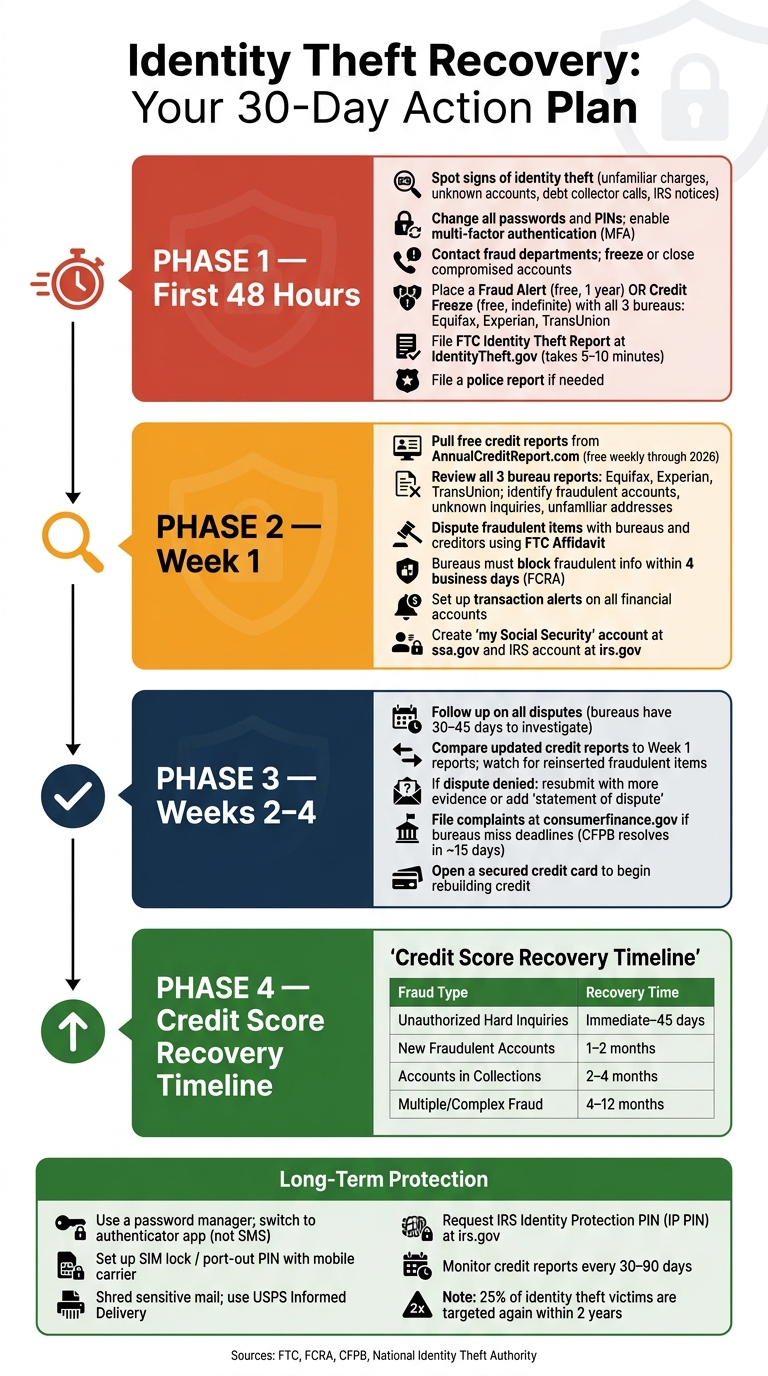

Identity Theft Recovery: A 30-Day Action Plan

Identity theft can disrupt your life, but taking quick, strategic actions can limit the damage and help you recover. This 30-day plan divides the recovery process into clear steps:

- First 48 Hours: Secure your accounts, place fraud alerts or credit freezes, and file an official identity theft report.

- Week 1: Review your credit reports, identify fraudulent activity, and dispute false accounts with creditors.

- Weeks 2-4: Rebuild your credit, track dispute outcomes, and implement safeguards to prevent future incidents.

Key tools include IdentityTheft.gov for filing reports, free credit reports from AnnualCreditReport.com, and AI tools like DidIBuyIt to simplify disputes. With this plan, you can regain control and protect your information moving forward.

Identity Theft Recovery: 30-Day Action Plan Timeline

Identity Theft Protection: 5 Essential Steps to Safeguard Your Finances | TIAA

sbb-itb-5d40823

First 48 Hours: Steps to Take Right Away

Time is critical. Colleen Tressler from the FTC emphasizes that acting quickly can significantly reduce the damage caused by identity theft [1]. The steps you take in the first 48 hours are crucial for securing your identity and limiting further harm. Here's what you need to do immediately.

How to Spot Identity Theft

Before locking down your accounts, confirm any signs of unauthorized activity. Look for these red flags:

- Unfamiliar charges on your bank or credit card statements.

- Bills or accounts in your name that you didn’t open.

- Unexpected calls from debt collectors.

- IRS notices about duplicate tax filings.

If you notice anything suspicious, call your bank immediately using the number on the back of your card. For credit cards, your liability is capped at $50. For debit cards, acting within two business days also limits your liability to $50 [3]. Quick action is vital.

Securing Your Financial Accounts

Once you’ve identified suspicious activity, secure your accounts right away:

- Change passwords and PINs for all financial accounts.

- Enable multi-factor authentication (MFA) using an app like Google Authenticator or Authy.

- Contact the fraud departments of affected companies to freeze or close compromised accounts. Request written confirmation of account closures and charge reversals.

- Set up a SIM PIN or port-out freeze with your mobile carrier to protect against phone-related fraud.

- If you suspect unauthorized checking account activity, request a free ChexSystems report to check for accounts opened in your name.

Placing Fraud Alerts and Credit Freezes

After securing your accounts, take steps to protect your credit file. You can either place a fraud alert or a credit freeze - here’s how they compare:

| Feature | Fraud Alert | Credit Freeze |

|---|---|---|

| What it does | Requires lenders to verify your identity before issuing new credit | Blocks new creditors from accessing your credit file |

| How to place it | Contact one bureau (they notify the other two) | Contact all three bureaus individually |

| Duration | 1 year (initial) or 7 years (extended) | Indefinite until you lift it |

| Cost | Free | Free |

To place a credit freeze or fraud alert, contact the credit bureaus directly:

| Credit Bureau | Phone | Website |

|---|---|---|

| Equifax | 800-685-1111 | equifax.com/personal/credit-report-services |

| Experian | 888-397-3742 | experian.com/help |

| TransUnion | 888-909-8872 | transunion.com/credit-help |

Make sure to save any PINs or passwords provided by the bureaus, as you’ll need them to temporarily lift the freeze when applying for credit.

Filing an Official Identity Theft Report

To formalize your case, file an FTC Identity Theft Report at IdentityTheft.gov. The website will generate an Identity Theft Affidavit in just 5–10 minutes [5]. Print this affidavit immediately - it’s essential for disputing fraudulent charges.

If a police report is needed, bring the following:

- Your FTC Identity Theft Affidavit.

- A government-issued ID.

- Proof of your current address.

- Any evidence of theft.

Request a copy of the police report or at least the report number. Keep detailed records of every call, noting the date, time, and representative’s name to stay organized throughout the process.

Week 1: Stopping Further Damage and Reviewing Your Credit

Once you’ve secured your accounts and filed an FTC Identity Theft Report, the next step in Week 1 is to assess the damage and take action to stop any further fraud.

How to Review Your Credit Reports

Start by visiting AnnualCreditReport.com, the only federally authorized website for free credit reports. Through 2026, every U.S. consumer is entitled to access a free credit report from each of the three major bureaus - Equifax, Experian, and TransUnion - once a week[6]. Additionally, Equifax offers six extra free reports per year[6][7].

Carefully go through each report and look for anything that seems off. This includes unknown accounts, unexpected credit inquiries, unfamiliar addresses, or signs of delinquency that don’t match your history. Make a list of every suspicious item, as you’ll need to address these through disputes.

"The sooner you spot this fraud, the sooner you can take action to stop the harm and correct the errors." - Seena Gressin, Attorney, FTC[8]

If you’re not comfortable using the website, you can call 1-877-322-8228 or send a request form by mail to P.O. Box 105281, Atlanta, GA 30348-5281.

Disputing Fraudulent Accounts with Creditors

Your FTC Identity Theft Report is your key tool for disputing fraudulent accounts. Use it to file disputes with both the credit bureau and the creditor involved[6]. According to the Fair Credit Reporting Act (FCRA), once you submit this report, credit bureaus must block fraudulent information within 4 business days, bypassing the usual 30-day investigation period[9].

When sending disputes by mail, always use certified mail with a return receipt to confirm delivery[6]. Include copies (not originals) of your FTC Identity Theft Report, a government-issued ID, and your credit report with the fraudulent items clearly marked. Once a creditor closes a fraudulent account, ask for a written confirmation that the account is closed and the balance is zero[9].

Here’s how to contact the major credit bureaus for disputes:

| Credit Bureau | Dispute Phone | Dispute Mailing Address |

|---|---|---|

| Equifax | 866-349-5191 | P.O. Box 740256, Atlanta, GA 30348 |

| Experian | 888-397-3742 | P.O. Box 4500, Allen, TX 75013 |

| TransUnion | 800-916-8800 | P.O. Box 2000, Chester, PA 19016 |

DidIBuyIt's AI-powered platform simplifies this process by generating dispute documents tailored to each creditor, helping you avoid unnecessary delays. Once disputes are underway, it’s time to focus on preventing future fraud.

Setting Up Alerts to Catch New Fraud

Identifying and stopping existing fraud is just the beginning. You’ll also need to stay vigilant for any new fraudulent activity. Set up alerts on all your financial accounts to notify you of every transaction, no matter how small. Many banks allow you to configure these alerts directly through their mobile apps[9].

Additionally, create a "my Social Security" account at ssa.gov and an IRS online account at irs.gov. This prevents fraudsters from opening accounts in your name or intercepting your benefits and tax information[4].

Using your FTC Identity Theft Report, you can also request an extended 7-year fraud alert, which will remove your name from pre-screened marketing lists for five years[2][9].

For added security, DidIBuyIt's real-time tracking tools can help you monitor for recurring or new fraudulent charges, giving you peace of mind while you work on resolving any disputes.

Weeks 2 to 4: Rebuilding Credit and Protecting Against Future Theft

After handling the initial steps in Week 1, the next phase focuses on repairing your credit and putting safeguards in place to prevent identity theft from happening again.

Checking and Following Up on Dispute Outcomes

In Week 2, it’s time to follow up on any disputes you’ve filed. Credit bureaus are required to investigate disputes within 30 days, though this can extend to 45 days if you provide additional documentation[10]. If you submitted an official FTC Identity Theft Report, the bureaus must block fraudulent information within four business days[11][9].

Once you receive responses, compare the updated credit report with the one from Week 1. Look for any reinserted items that were previously removed. Continue reviewing your credit report at 30-day and 90-day intervals to catch any discrepancies[11].

If a dispute is denied, don’t stop there - resubmit with additional evidence or add a "statement of dispute" to your credit file. This ensures the dispute is noted in future credit reports[6]. If a bureau or creditor fails to meet deadlines or refuses to act, file a complaint at consumerfinance.gov. The Consumer Financial Protection Bureau (CFPB) typically resolves credit reporting complaints within about 15 days[9].

"You want your credit report to be accurate because it affects whether you can borrow money - and how much you'll pay - to borrow money." - Federal Trade Commission[6]

Keep a detailed log of your disputes. Include the filing date, the bureau or creditor contacted, the specific item disputed, any reference numbers, and the expected response deadlines[9].

Steps to Rebuild Your Credit

Once fraudulent accounts and unauthorized inquiries are removed, your credit score will start to recover. The recovery timeline depends on the type of fraud that was reported:

| Fraud Type | Score Recovery Timeline After Fraud Removal |

|---|---|

| Unauthorized Hard Inquiries | Immediate to 45 days |

| New Fraudulent Accounts | 1–2 months |

| Accounts in Collections | 2–4 months |

| Multiple/Complex Fraud | 4–12 months |

To rebuild your credit, consider opening a secured credit card. These cards are backed by a cash deposit and are ideal for making small purchases. Be sure to pay off the balance in full and on time - setting up autopay can help ensure you never miss a payment[12].

If you’ve placed a credit freeze, remember to temporarily lift it while applying for a secured card. Once your application is processed, reapply the freeze for continued protection[11].

Long-Term Steps to Protect Your Identity

With your credit back on track, the focus should shift to strengthening your digital and physical security to prevent future identity theft. This is especially important because 25% of identity theft victims are targeted again within two years[9].

Start by improving your online security. Use a password manager to create unique, strong passwords for all your accounts. Switch from SMS-based two-factor authentication to an authenticator app, as SMS methods are vulnerable to SIM-swapping attacks[2]. Additionally, contact your mobile carrier to set up a port-out PIN or enable a SIM lock for added protection[2].

On the physical side, shred any mail containing sensitive information before throwing it away. Sign up for USPS Informed Delivery at informeddelivery.usps.com to preview your incoming mail and detect potential fraud early[9]. You can also request an IRS Identity Protection PIN (IP PIN) at irs.gov. This six-digit number must be used when filing your federal tax return, significantly reducing the risk of someone filing fraudulent taxes in your name[9].

Continue monitoring your credit reports through AnnualCreditReport.com[6]. For added vigilance, tools like DidIBuyIt can help track suspicious recurring charges and generate dispute documents quickly if new fraudulent activity is detected.

Conclusion: Taking Back Control and Staying Alert

Recovering from identity theft is a process that can span several weeks, but the first 48 hours are absolutely crucial. During this time, you should freeze your credit, file an official Identity Theft Report through IdentityTheft.gov, and secure your financial accounts. By Week 1, your focus should shift to reviewing credit reports and disputing any fraudulent accounts. From Weeks 2 to 4, it’s all about following up, rebuilding your credit, and strengthening your defenses. This step-by-step approach helps you regain control while laying the groundwork for long-term security.

Time is of the essence.

"The severity and duration of recovery correlates directly with the lag between theft occurrence and detection." - National Identity Theft Authority [13]

Keeping detailed records is key to navigating this process. Every dispute, communication, and resolution should be documented thoroughly. These records are not only vital for staying organized but also serve as legal protection if a creditor or credit bureau fails to take appropriate action.

Even after recovery, the risk isn't entirely gone. Identity theft can happen again, which makes adopting strong protective habits a must. Set up real-time alerts, review your credit regularly, use an IRS IP PIN, and enable strong multi-factor authentication to protect your personal information.

Tools like DidIBuyIt can make this process smoother. If suspicious charges pop up after your recovery, its AI-powered features can analyze disputes and generate bank-ready documents, saving you from starting over. Armed with this 30-day plan, you can reclaim your identity and take steps to secure your future.

FAQs

Should I choose a fraud alert or a credit freeze?

When deciding between the two, it all comes down to what you need. A fraud alert acts as a signal to lenders, urging them to confirm your identity before approving any new accounts. It stays active for one year but can be renewed. This is a good option if you're looking for temporary protection while keeping an eye on your credit.

On the other hand, a credit freeze takes things a step further by completely restricting access to your credit report. This is a stronger safeguard, especially if your personal information has been seriously compromised. For the highest level of protection, you can even combine both measures.

What paperwork should I keep for disputes and a police report?

When dealing with identity theft disputes and filing a police report, staying organized is crucial. Here’s what you should hold on to:

- Correspondence Records: Keep copies of all communication with banks, credit bureaus, or any companies involved in the dispute.

- FTC Identity Theft Affidavit: Retain this affidavit along with any official reports you’ve filed.

- Mail and Confirmation Receipts: Save certified mail receipts and confirmation letters for proof of your actions.

- Credit Reports: Keep copies of your credit reports, especially those with notes highlighting suspicious activity.

- Police Report: Always have a copy of your police report and note the case number for reference.

Having these documents organized can make the resolution process much smoother and help with accurate reporting.

How can I rebuild my credit while my case is still open?

To start rebuilding your credit while dealing with an identity theft case, here’s what you can do:

- Set up a credit freeze or fraud alert: This prevents anyone from opening new accounts in your name.

- Check your credit reports often: Look for any accounts or charges you don’t recognize and address them promptly.

- Dispute fraudulent charges: Work with credit bureaus and creditors, providing proof to remove unauthorized activity.

- Keep an eye on your credit activity: Use monitoring tools to catch any unusual changes and act quickly.

Taking these steps can help you regain control of your credit over time.