Embedded Finance: What It Means for Non-Bank Brands

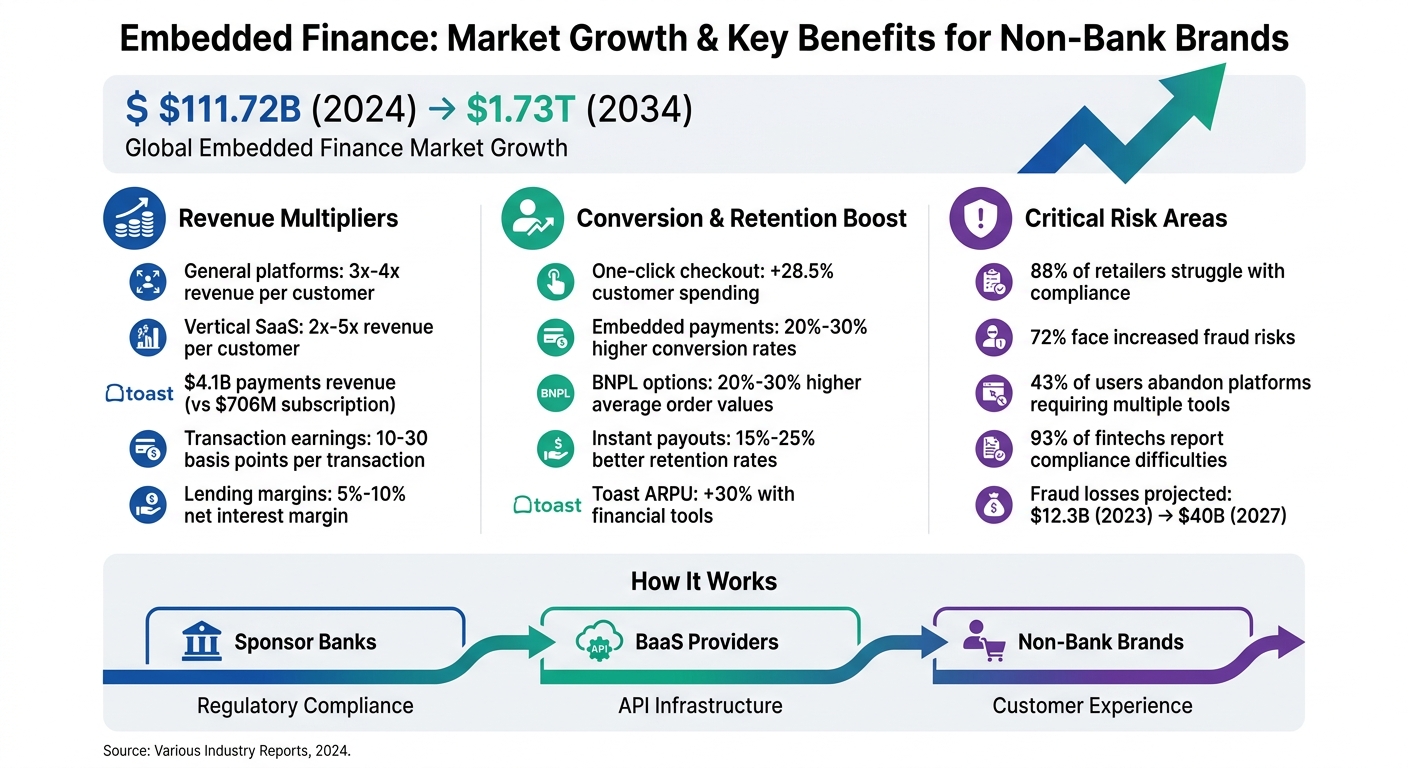

Embedded finance lets non-bank brands integrate financial services - like payments, lending, and insurance - directly into their platforms. This simplifies transactions, boosts customer loyalty, and creates new revenue opportunities. By 2034, the global embedded finance market is expected to grow from $111.72 billion in 2024 to $1.73 trillion, driven by its ability to deliver financial services where and when users need them.

Key takeaways:

- What it is: Embedded finance integrates financial services into non-financial platforms using APIs.

- How it works: A three-layer model involves sponsor banks (regulatory compliance), BaaS providers (API infrastructure), and brands (customer experience).

- Why it matters: It reduces friction, increases revenue, and improves customer retention. For example, Shopify Capital and Amazon Lending have issued billions in loans through embedded finance.

- Benefits: Higher conversion rates (up to 50%), personalized offers using customer data, and seamless user experiences.

- Challenges: Regulatory compliance, fraud prevention, and dispute management require careful planning and strong partnerships.

Embedded finance is reshaping how brands interact with customers, offering convenience and financial flexibility while opening doors to significant growth and revenue potential.

Embedded Finance Market Growth and Key Benefits for Non-Bank Brands

Benefits of Embedded Finance for Non-Bank Brands

Higher Revenue and Customer Retention

Embedded finance can significantly boost revenue. Platforms that integrate financial services often see their revenue per customer multiply by 3x to 4x. For vertical SaaS companies, this number jumps to 2x to 5x [7]. The revenue streams are diverse: brands earn 10–30 basis points per transaction on embedded payments, while embedded lending typically generates net interest margins of 5% to 10% [7].

Take Toast, a restaurant-focused platform, as an example. In 2024, it generated $4.1 billion in payments revenue, far surpassing its subscription revenue of $706 million. Customers using its financial tools also delivered 30% higher ARPU and were less likely to churn [7].

Embedded finance also encourages more spending and better conversion. Features like one-click checkout can increase customer spending by 28.5% [3]. Retailers offering Buy Now, Pay Later (BNPL) options report 20% to 30% higher average order values, while gig platforms providing instant payouts achieve 15% to 25% better retention rates compared to weekly pay cycles [4].

When a platform integrates deeply into a customer's financial life - whether through payroll, working capital, or daily transactions - switching to a competitor becomes far less appealing. This creates loyalty without relying on restrictive tactics [6][3].

These financial gains are just the beginning. Embedded finance also transforms the user experience in ways that keep customers coming back.

Simplified User Experience

Friction in financial processes often leads to lost customers. A staggering 43% of users abandon software platforms because they’re forced to juggle multiple tools for financial tasks [7].

Embedded finance removes these pain points by keeping all transactions within a single interface. For example, offering travel insurance during flight booking or financing at checkout ensures customers get what they need without leaving the platform.

The results speak for themselves. Retailers that reduce checkout friction with embedded payments see 20% to 30% higher conversion rates [4]. Shopify Capital is a prime example. In 2025, it originated $4.2 billion in merchant cash advances and loans, achieving 43% year-over-year growth in gross loans receivable by embedding the entire application process into the merchant dashboard [7]. This approach eliminates the need for merchants to navigate external workflows or deal with lengthy bank applications.

"Customers want a seamless, Netflix-like experience in every facet of their lives... They don't want to tell you more than once who they are or what services they require. And they want speed." – Sabrina Dar, Chief of Staff at Mambu [1]

By reducing friction and streamlining processes, embedded finance not only simplifies transactions but also unlocks opportunities for better personalization.

Better Personalization Through Data

Embedded finance builds on its seamless nature by leveraging customer data for highly tailored financial services. Non-bank brands often have access to rich behavioral data - like sales volume, inventory turnover, and purchase history - that traditional banks don’t. This allows for more precise risk assessments and personalized offers [5].

This data advantage enables more inclusive lending. AI models using proprietary platform data can outperform traditional FICO-based models by 30% to 50%, helping brands extend credit to thin-file borrowers who might otherwise be rejected [9]. Instead of relying solely on credit scores, platforms can base lending decisions on actual revenue patterns, opening doors for underserved customers.

Personalization isn’t limited to lending. Platforms can deliver contextual financial offers triggered by specific user actions. For instance, if a repeat customer’s card payment fails, the system could offer a one-time BNPL option [1]. British Airways uses a similar approach, embedding travel insurance into its booking process and dynamically adjusting pricing based on factors like destination, trip length, and traveler age through API connections [4].

For B2C brands, 29.7% cite access to richer behavioral and financial data as a key reason for adopting embedded finance [2]. This data doesn’t just enhance financial products - it creates a feedback loop that improves the overall customer experience across the platform.

sbb-itb-5d40823

Real Examples of Embedded Finance

Embedded Payments

Embedded payments streamline transactions by removing the need for users to switch platforms or repeatedly input payment details.

Take Ace Hardware, for example. They introduced PayPal's "Pay Monthly" 0% APR option on their website in Q4 2024 to help customers finance bigger-ticket items like grills and lawnmowers. Spearheaded by Ecommerce Operations Manager Laura Beleganski, this move had an impressive impact: purchases made with this payment option saw an average order value seven times higher than standard orders. On top of that, Ace Hardware experienced a 29% year-over-year boost in total PayPal sales and a 35% jump in Pay Later sales during the same quarter [13].

"Giving customers the ability to purchase items they need and pay them off over time has allowed us to be even more helpful." – Laura Beleganski, Ecommerce Operations Manager, AceHardware.com [13]

Similarly, Simba Sleep, a UK-based mattress company, partnered with Snap Finance in May 2026 to embed flexible payment options into its Shopify checkout system. Jon Moore led the integration, which took just three weeks to complete. By utilizing open banking and advanced credit decisioning, Simba Sleep was able to approve over 35% of applicants who would typically be turned down by traditional lenders, broadening its customer reach [10].

Now, let’s look at how embedded lending simplifies access to credit, making it more inclusive.

Embedded Lending and Buy Now Pay Later (BNPL)

Embedded lending integrates credit decisions directly into platforms, eliminating the need for separate loan applications or trips to the bank.

For instance, 360 Payments launched "360 Capital" in October 2025, an embedded financing program aimed at independent auto repair shops. Under the leadership of COO Anita Gibbs, the program worked with Parafin to provide over $100 million in loans to more than 900 small businesses. Funds were made accessible within three days, and 85% of eligible businesses returned for additional loans [12].

Another example is Alibaba.com, which rolled out "Pay Later for Business" in October 2024. Led by Head of Customer Retention Strategy Yiran Li, this program offers revolving credit limits with up to 90 days to pay, directly integrated into the "My Alibaba" dashboard. This approach not only helped reactivate dormant customers but also increased order sizes by removing cash flow constraints [11].

"Balance helps us solve one of the biggest challenges that we have in the B2B marketplace. Giving buyers the payment flexibility they need without adding any risk or friction." – Yiran Li, Head of Customer Retention Strategy, Alibaba.com [11]

In Poland, Allegro, the country’s largest marketplace, reported that in Q2 2025, "Allegro Pay" accounted for 15.3% of its gross merchandise volume (GMV), funding PLN 3.3 billion in loans in just one quarter. Data from Q4 2024 also revealed that 52% of loans originated by Allegro Pay directly boosted marketplace transactions [14].

Beyond payments and lending, embedded insurance is transforming how customers access tailored protection.

Embedded Insurance

Embedded insurance integrates coverage options directly into the purchase process, offering protection exactly when customers need it most.

In the travel sector, insurers now include coverage for trip cancellations, medical emergencies, and lost baggage as part of the booking process. This seamless integration enhances customer experience by providing instant, on-demand protection. Similarly, in e-commerce, retailers are embedding extended warranties and product protection plans for high-value items like electronics and appliances at checkout. The embedded insurance market is projected to grow at a compound annual rate of over 35% between 2025 and 2033 [16]. In the UK, 60% of adults have already encountered embedded financial services, including insurance, during online checkouts [17].

The automotive industry is also embracing embedded insurance. For example, Flexicar, a leading used car retailer in Spain, launched a mobility-as-a-service model using Basikon’s low-code platform. This system, which integrates with over 10 external APIs for credit scoring and insurance, reduced human error rates by 90% [15].

What’s Working in Embedded Finance and What Isn’t with Adyen's Head of Strategic Accounts

How to Add Embedded Finance to Your Brand

Adding embedded finance to your brand involves weaving financial services into your existing offerings through strategic partnerships. The key to success lies in selecting the right collaborators, adhering to strict compliance guidelines, and leveraging advanced AI and API tools. These steps ensure a seamless experience for your users. With the embedded finance market expanding rapidly, this is the perfect opportunity to take action.

Start by identifying your customers' financial pain points. Are they abandoning their carts because they can't split payments? Do they require working capital to place larger orders? Understanding these challenges will help you choose the right financial product, whether it's instant payments, embedded lending, or insurance [18]. Once you've pinpointed the need, focus on building the partnerships necessary to make it happen.

Working with Banking-as-a-Service Providers

The first step is finding the right partners to power your embedded finance solutions. You'll need two key players: a sponsor bank and a Banking-as-a-Service (BaaS) provider [1]. The sponsor bank grants access to payment networks like Fedwire, ACH, and card systems, while the BaaS provider handles card issuance, payment processing, and user-facing interfaces.

Choosing the right partner is critical. Alyssa Folickman from Alloy emphasizes:

"Part of it is really just finding somebody that's a good match. Don't just reach out to everybody and see who's there. Select a partner experienced in your target market and product area" [1].

Look for partners with proven expertise in your industry and conduct thorough checks on their regulatory history. This is especially important because sponsor banks are nine times more likely to face regulatory enforcement actions than non-partner banks [1].

You'll also need to decide on an operational model. In a "Compliance-as-a-Service" setup, the sponsor bank handles all risk and compliance infrastructure. Alternatively, a "Program Management" model relies on a middleware platform to manage compliance tasks [1]. Each approach has its own trade-offs in terms of control, cost, and speed.

Meeting Compliance and Security Requirements

Compliance isn't optional when it comes to embedded finance. You must implement Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols to verify users and monitor for suspicious activity. Key U.S. regulations to follow include the Bank Secrecy Act, Truth in Lending Act (TILA) for credit products, Electronic Fund Transfer Act (EFTA) for digital payments, Gramm-Leach-Bliley Act (GLBA), and state laws like the California Consumer Privacy Act (CCPA) [21].

As mobile fraud continues to rise - growing 7% between 2024 and 2025 [1] - identity verification must go beyond basic methods. Multi-layered digital verification tools, powered by AI, can automate KYC and AML processes, cutting onboarding times from days to minutes [18].

Define roles clearly in your partnership agreements. Specify which party - your brand, the BaaS provider, or the sponsor bank - is responsible for tasks like filing Suspicious Activity Reports (SARs), managing KYC flows, and handling regulatory audits [1]. Also, have an exit strategy in place in case your primary BaaS provider encounters regulatory issues or service interruptions [21].

Using AI and APIs for Integration

APIs are the backbone of embedded finance, connecting your platform to banking systems. They enable financial actions - such as payments, lending, or insurance - to happen directly within your app or website. This eliminates the need to redirect users to external platforms, boosting conversion rates from an average of 15% to 50% or more [20].

AI further enhances the process by automating back-office tasks and analyzing real-time data. This allows for personalized financial offers, such as tailored buy-now-pay-later (BNPL) plans or contextual insurance [19]. AI also speeds up credit decisions, often delivering results in under 30 seconds by using platform-specific data like a merchant's sales history rather than traditional credit scores [4].

William Morales, Founder of FinTechtris, predicts:

"In 2026, expect every successful embedded finance product to be AI-native, not just AI-enhanced" [19].

To speed up implementation, consider using codeless Software Development Kits (SDKs) and standardized APIs. These tools make it easier to integrate financial modules into your platform [20]. Start with a pilot program to test adoption rates and identify any friction points before scaling [18][19].

When integrating, ensure your engineering and design teams collaborate closely. APIs should feel like a natural part of your app's user experience, not an afterthought. Conduct extensive testing to ensure the financial features blend seamlessly into your interface [18][19]. This attention to detail can lead to a 28.5% increase in customer spending, thanks to smoother one-click checkout experiences [3].

Managing Challenges and Risks in Embedded Finance

Embedded finance presents immense opportunities, but it also comes with serious risks. With U.S. transaction values expected to hit $7 trillion by 2026 [21], and over 25% of FDIC enforcement actions since early 2024 targeting sponsor banks [22], non-bank brands must focus on managing these risks effectively.

The primary challenges fall into three areas: regulatory compliance, fraud prevention, and dispute resolution. Ignoring these risks can lead to financial losses, damaged customer trust, and even the loss of key partnerships. Tackling these issues requires strong technological solutions and operational strategies.

Regulatory and Compliance Challenges

Navigating U.S. regulations is a major hurdle for non-bank brands. While sponsor banks carry the ultimate responsibility for funds and compliance, your brand still needs to adhere to the bank's regulatory charter [22][1]. In fact, 88% of retailers using embedded finance report difficulties with compliance [25].

One critical issue is maintaining real-time visibility into For Benefit Of (FBO) accounts. Gaps in data-sharing between tech partners and banks can lead to unaccounted funds, as seen in the 2024 Synapse collapse [22]. Sheetal Parikh, General Counsel & Chief Compliance Officer at Treasury Prime, emphasizes:

"Banks engaging in fintech partnerships will need to strengthen their investment and oversight in assessing their partners' operational risk" [22].

Brands offering credit products also face challenges under the "true lender" doctrine, which examines which party is responsible for credit decisions and financial risk [23]. Additionally, the CFPB's Personal Financial Data Rights rule (Open Banking) requires compliance by April 1, 2026 [23]. This means building robust authorization systems and audit trails.

To stay compliant:

- Use real-time reconciliation technology for continuous ledger visibility, rather than end-of-day settlement [22].

- Embed KYC processes and transaction limits directly into your systems.

- Prepare defensible audit trails for AI-driven transactions, as regulators are paying closer attention to AI governance [23].

- Partner with BaaS providers that have strong compliance records, not just competitive pricing [2][24].

Fraud Prevention and Data Privacy

Fraud prevention is another critical challenge in embedded finance. Banking fraud losses in the U.S. are projected to rise from $12.3 billion in 2023 to $40 billion by 2027, fueled in part by advancements in generative AI [29]. For brands offering embedded credit products, 72% face increased fraud risks, and financial institutions lose an average of $98.5 million annually to fraud, cyberthreats, and compliance issues [25][26].

The key to combating fraud is stopping it before it happens. As Eric Frankovic, President of Corporate Payments at WEX, explains:

"The best fraud strategy remains simple. It's don't let the bad transaction happen" [28].

AI-powered tools are essential for this. Graph Neural Networks (GNNs) can analyze payment networks and identify nearly twice as many money-laundering networks as traditional methods [27]. Behavioral biometrics, like voice and facial recognition, also enhance security with minimal customer friction [26][30].

For data privacy, federated learning is a promising approach. This technology trains AI models locally, sharing only mathematical parameters instead of raw customer data [27]. It allows collaboration with banks and partners while complying with data protection rules.

To strengthen fraud prevention:

- Deploy virtual cards for payouts, limiting usage by merchant, timeframe, and amount with AI [28].

- Use AI for real-time, pre-transaction fraud detection, especially for faster, irrevocable payment rails [28][30].

- Replace manual reviews with automated systems - 80% of financial organizations report better fraud detection after adopting AI [26].

Resolving Embedded Payment Disputes

Efficient dispute resolution is vital for maintaining customer trust. Under Regulation E, which governs electronic fund transfers, specific timelines and liability limits apply to error resolution [32]. Consumers must report errors within 60 days for full protection, and if investigations take more than 10 business days, provisional credit must be issued [32].

However, 93% of fintechs report difficulties staying compliant with financial regulations, and 55% cite a lack of automation in compliance processes [31]. To address this, integrate user-friendly dispute reporting tools directly into your platform, avoiding external redirects [32]. Keep detailed records of communications, investigation notes, and disclosures for at least two years [32].

Platforms like DidIBuyIt can simplify this process. By offering AI-powered dispute analysis and generating professional, bank-ready documents, DidIBuyIt helps brands manage disputes efficiently while maintaining a positive customer experience. It supports major payment platforms like Visa, Mastercard, Amex, and PayPal and ensures encrypted data handling with 24/7 support.

To handle disputes effectively:

- Develop a detailed "exceptions and dispute playbook" to address scenarios like failed payments, refunds, and duplicate payouts [31].

- Use automated systems to track investigation timelines and prevent regulatory violations [32].

- Clearly define roles with sponsor banks for managing disclosures and records [32].

It's also worth noting that under Regulation E, disputes cannot be dismissed solely because of customer negligence. Protections depend on reporting timelines, not user behavior [32].

Conclusion: New Opportunities with Embedded Finance

Embedded finance is changing the way non-bank brands enhance their offerings. By weaving payments, lending, and insurance into their platforms, businesses can reduce friction, boost customer loyalty, and open up new revenue channels. Retailers have seen 20–30% higher conversion rates, while platforms report 15–25% better retention rates - clear indications of its potential impact [4]. The global market is expected to hit $320 billion by 2026, with revenues possibly surpassing $7 trillion by 2030 [4][19]. This growth, however, hinges on effective risk management and seamless technology integration.

But success in this space demands more than speed. Trust, compliance, and operational excellence are non-negotiable. As Renata Caine, General Manager of Banking as a Service at Green Dot, puts it:

"Embedded finance is fundamental to how businesses create value and build customer loyalty" [2].

The market now calls for innovation that balances creativity with compliance [2]. Brands must establish regulatory safeguards from the start and work with partners who have a proven track record in navigating regulations [2][19].

As platforms grow, dispute management becomes a key focus. DidIBuyIt steps in here with its AI-powered tools that create bank-ready documentation, building customer confidence by supporting major payment platforms like Visa, Mastercard, Amex, and PayPal, while maintaining strict data security.

To succeed, identify your friction points, leverage AI for personalization and risk management, and partner with companies that prioritize compliance and transparency [8][19]. Embedded finance isn’t about replacing banks - it’s about rethinking how financial services are delivered [3]. Brands that combine AI-driven personalization with strong compliance measures will set the standard for the next wave of customer engagement [19].

FAQs

How do I choose between embedded payments, lending, or insurance first?

Choosing the right embedded financial service - whether it's payments, lending, or insurance - comes down to your business objectives and what your customers value most.

- If creating smooth, hassle-free transactions is your top goal, embedded payments are the way to go. They enhance the checkout process and improve the overall customer experience.

- Want to help customers with credit or financing options while increasing sales and loyalty? Embedded lending can do just that by offering flexible payment solutions.

- For businesses where risk management and tailored coverage are essential, embedded insurance is the better fit. It provides customers with protection that feels personalized.

The key is to align your decision with your company’s strategic priorities and current capabilities.

What should my brand own vs. what should the sponsor bank or BaaS provider handle?

In embedded finance, your brand takes charge of the customer experience - this includes your branding, the user interface, and maintaining customer relationships. Meanwhile, the sponsor bank or Banking-as-a-Service (BaaS) provider handles the heavy lifting, such as core financial operations, compliance, and managing risks.

This arrangement allows your brand to concentrate on building engagement and loyalty while offering financial services seamlessly. You can skip the challenges of becoming a licensed bank or navigating regulatory hurdles yourself.

What do I need in place to handle disputes and stay compliant in the U.S.?

To navigate disputes and remain compliant in the U.S., companies need to have solid frameworks for risk management and regulatory adherence. This means implementing clear processes for resolving disputes, following both federal and state financial regulations, and putting strong anti-fraud measures in place.

Using AI tools can make compliance tasks, fraud prevention, and dispute handling more efficient. Additionally, collaborating with regulated financial institutions and keeping communication with customers open and transparent are key steps to reducing risks and maintaining trust.