How Credit Utilization Is Actually Calculated by Issuers

Credit utilization is the percentage of your available revolving credit that you're using, and it directly impacts your credit score. Issuers calculate it by dividing your reported balance (from your billing statement) by your credit limit and multiplying by 100. Both overall utilization (all accounts combined) and per-card utilization (individual accounts) are considered. High utilization signals financial strain to lenders, while low utilization - ideally under 10% - can boost your score.

Key points to manage utilization:

- Pay balances before the statement closing date.

- Keep old credit cards open to maintain higher limits.

- Request credit limit increases periodically.

- Avoid maxing out a single card, even if overall usage is low.

Understanding how issuers report balances and the timing of their updates is crucial to keeping your utilization low and your credit score healthy.

How Credit Issuers Calculate Credit Utilization

The Basic Credit Utilization Formula

To figure out your credit utilization, divide your current balance by your credit limit, then multiply the result by 100.

| Utilization Type | Formula |

|---|---|

| Per-Card Utilization | (Individual Card Balance ÷ Individual Card Limit) × 100 |

| Overall Utilization | (Sum of All Revolving Balances ÷ Sum of All Credit Limits) × 100 |

For example, if you have a $500 balance on a card with a $2,000 limit, your utilization is 25%. Interestingly, a 0% utilization might actually hurt your score, as credit scoring models prefer to see a small positive balance (around 1%) to demonstrate active credit use.

Per-Card Utilization vs. Overall Utilization

Credit scoring models consider both your total credit usage across all cards and the utilization of each individual card.

- Per-card utilization reflects the risk associated with a specific account.

- Overall utilization measures your total debt compared to your total available credit.

Both are critical. Let’s break it down with an example:

| Account | Credit Limit | Balance | Utilization Rate |

|---|---|---|---|

| Card 1 | $1,000 | $200 | 20% |

| Card 2 | $2,000 | $500 | 25% |

| Card 3 | $5,000 | $2,000 | 40% |

| Total/Overall | $8,000 | $2,700 | 33.75% |

While your overall utilization is 33.75%, Card 3's individual utilization of 40% could negatively affect your score.

"A FICO Score considers your overall utilization rate and the highest utilization rates on specific revolving credit accounts." - Louis DeNicola, Finance Writer [4]

This is why maxing out even one card can hurt your credit score, even if your other cards have zero balances. Scoring models are designed to catch those high-risk patterns.

Edge Cases in Utilization Calculations

Some accounts don’t follow the standard credit utilization formula. Here are a few exceptions:

- No Preset Spending Limit (NPSL) Cards: Cards like certain high-tier American Express products don’t report a fixed credit limit to credit bureaus. Without a defined limit, some scoring models exclude these cards from utilization calculations. However, your payment history on these accounts still matters [1].

- Closed Accounts with Balances: If you close an account but still owe money, the balance is included in your utilization. Since the account no longer has an available limit, the balance increases your utilization ratio [4].

- Home Equity Lines of Credit (HELOCs): Although HELOCs are revolving accounts, FICO Scores typically exclude them from utilization calculations because they’re secured by your home [4][2].

- Unsecured Personal Lines of Credit: These accounts are treated the same as credit cards and included in utilization calculations.

- Authorized User Accounts: If you’re an authorized user on someone else’s credit card, that account’s balance and limit are usually factored into your own utilization ratio [3][4].

Next, we’ll explore how credit issuers report these details to credit bureaus.

Credit Card Utilization Explained

How Issuers Report Data to Credit Bureaus

Understanding how issuers report your account information to credit bureaus can help you better manage your credit utilization.

What Data Issuers Send to Credit Bureaus

Every month, issuers send a snapshot of your account to the major credit bureaus - Equifax, Experian, and TransUnion. This snapshot includes details like your statement balance, credit limit, account status, and payment history. These elements are what determine your reported utilization ratio.

Here’s a key detail: issuers report the statement balance, which is the amount owed at the end of your billing cycle. As Emily Starbuck Gerson, a freelance writer for Experian, clarifies:

"Your credit report typically reflects the information from your last billing statement, so it is unlikely to match your current balance when you check it." [8]

How Reporting Timing Affects Your Utilization

Issuers generally report account data to the bureaus within 1 to 3 days of your statement closing date [11]. Federal law requires a minimum 21-day grace period between the statement closing date and the payment due date [11], creating a window where timing can impact how your utilization is reported.

For example, imagine you have a $1,500 balance on a credit card with a $3,000 limit, and your statement closes on the 5th of the month. That 50% utilization is sent to the bureaus soon after the closing date. Even if you pay off the balance in full by the due date on the 26th, your credit report will still show 50% utilization until the next statement cycle. To avoid this, consider reducing your balance a few days before the statement closes.

Since every card reports on its own schedule, your overall credit utilization is essentially a collection of snapshots taken at different times [8][9].

Reporting Errors and Special Account Situations

Sometimes, errors in reporting can inflate your utilization ratio. Two common problems include:

- Outdated credit limits: If your issuer hasn’t updated your credit limit after an increase, the reported utilization may be higher than it should be.

- Incorrect balances: Fraudulent or disputed charges can also skew the reported balance [10][1].

If you’ve recently opened a new credit card, keep in mind that it can take 30 to 60 days for the account to appear on your credit report [8]. Until then, the new card’s credit limit won’t help lower your utilization. For cards with no preset spending limit (NPSL), scoring models may use your highest historical balance as a substitute for a limit, which can artificially inflate your utilization [1].

Lastly, for authorized user and joint accounts, both the balance and the limit are factored into utilization for all users. If you’re added to an account with a high balance, it could increase your reported utilization - even if you didn’t make any charges on that account [4].

sbb-itb-5d40823

How Credit Scores Use Utilization Data

FICO vs. VantageScore: How Credit Utilization Is Calculated

Utilization in FICO and VantageScore Models

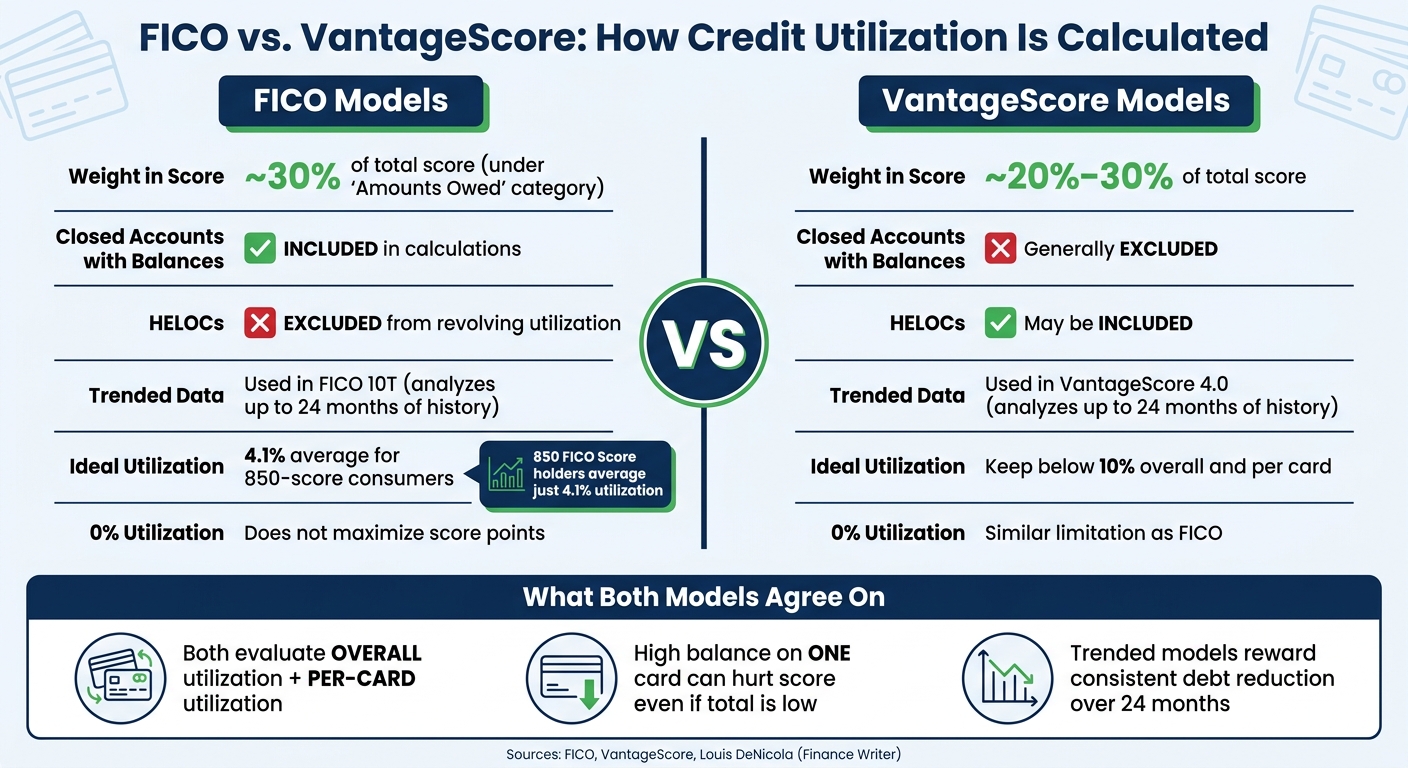

Credit scoring models like FICO® and VantageScore approach utilization data in slightly different ways, but both place significant weight on this factor. Credit utilization - essentially how much of your available credit you're using - makes up about 30% of your FICO® Score under the "Amounts Owed" category [4]. For VantageScore, it accounts for roughly 20% to 30% of your score [3]. These percentages highlight just how much influence utilization has on your overall credit score.

Both scoring systems evaluate utilization on two levels: your overall utilization across all cards and the utilization on each individual card. This means that even if your total utilization is low, a high balance on just one card can negatively impact your score [7].

Interestingly, having 0% utilization - no reported balances at all - might not be ideal. Carrying a very small balance can slightly boost your score. As finance writer Louis DeNicola explains:

"While a 0% utilization ratio won't cause your FICO® Scores to drop significantly, it can prevent you from achieving maximum points for the amounts owed score ingredient." [12]

In fact, data shows that individuals with a perfect 850 FICO® Score typically maintain an average overall utilization of just 4.1% [4].

There are also technical differences between the two scoring models:

| Feature | FICO Models | VantageScore Models |

|---|---|---|

| Weight | ~30% of total score [4] | ~20%–30% of total score [3] |

| Closed Accounts with Balances | Included in calculations [4] | Generally excluded [7] |

| HELOCs | Excluded from revolving utilization [4] | May be included [7] |

| Trended Data | Used in FICO 10T [4] | Used in VantageScore 4.0 [3] |

Why Your Reported Utilization May Look Different

Sometimes, the utilization percentage on your credit report might not match your own calculations. This discrepancy often comes down to timing. Credit card issuers typically report your statement balance rather than your current balance. As Louis DeNicola explains:

"Your credit card utilization calculations don't use your card's current balance - they depend on the credit card's statement balance as it appears in your credit report." [5]

Other factors can also affect these numbers. For example, FICO generally excludes HELOCs (home equity lines of credit) from revolving utilization calculations, while VantageScore excludes closed accounts with balances [7]. Additionally, authorized user accounts may contribute to your reported balances, and scoring models round percentages to the nearest whole number [7].

How Trended Data Is Changing Credit Scoring

Recent updates to credit scoring models, like FICO 10T and VantageScore 4.0, have introduced trended data into the mix. Unlike traditional models that rely on a single snapshot of your most recent balance, these newer models analyze utilization trends over the past 24 months [4][3]. This shift provides a more dynamic view of your credit habits.

Trended data distinguishes between "transactors" (who pay off balances in full each month) and "revolvers" (who carry balances over time). It rewards consistent debt reduction, offering a more comprehensive picture of financial responsibility.

| Feature | Traditional Models (FICO 8, VantageScore 3.0) | Trended Models (FICO 10T, VantageScore 4.0) |

|---|---|---|

| Data Scope | Most recent reported balance only | Up to 24 months of history |

| Utilization View | Single point-in-time percentage | Average utilization and balance trajectory |

| Impact of a Spike | Immediate high impact, quickly corrected | Smoothed over time; seen as part of a trend |

This evolution in credit scoring reflects a growing emphasis on long-term financial patterns rather than short-term fluctuations.

How to Manage Your Credit Utilization

Steps to Keep Your Utilization Low

Knowing how credit utilization is calculated gives you a real edge in managing your reported balance. One of the easiest tricks? Pay your balance before the statement closing date. This is when most issuers report your balance to the credit bureaus. Financial writer Ben Luthi from Experian emphasizes:

"Maintaining a low credit utilization ratio is one of the most effective strategies for improving your credit score." [13]

Besides timing your payments, there are other habits that can help. Consider requesting regular credit limit increases or updating your income with your card issuer - this can lower your utilization ratio without changing your spending. If you’re planning a large purchase, split the cost across multiple cards to avoid any single card hitting a high utilization percentage.

Another important tip: don’t close unused credit cards. When you close a card, its credit limit disappears from your total available credit. This can cause your overall utilization to spike overnight, even if your balances stay the same.

The sweet spot? Aim to keep your utilization below 10% overall and on each individual card.

Next, ensure the data being reported about your accounts is accurate.

How to Spot and Fix Utilization Errors with Issuers

Since your utilization depends on what issuers report, it’s important to double-check your credit report for errors. Even small inaccuracies, like outdated credit limits or balances, can increase your utilization ratio and hurt your credit score.

Start by pulling your credit reports from all three major bureaus - Experian, TransUnion, and Equifax - at AnnualCreditReport.com. Compare the reported balances and credit limits with your actual billing statements. Pay close attention to cards with no preset spending limit (NPSL). Sometimes issuers report your highest-ever balance as your credit limit, which can make your utilization look worse than it really is [6].

If you spot an error, here’s what to do:

-

Contact your card issuer to confirm if they’ve sent updated data to the bureaus. As LaToya Irby from The Balance advises:

"If the debt level still seems inaccurate after more than a month, check with your credit card company to see whether it has updated your account with the credit bureaus. If it has, then you will need to dispute the information with each credit bureau." [6]

- If the issuer confirms the data is correct but your report still shows the wrong numbers, file a dispute with each credit bureau individually. Use their online dispute portals to submit your claim. Corrections typically take one to two billing cycles to reflect on your report.

Using DidIBuyIt to Dispute Charges That Inflate Your Utilization

Sometimes, the problem isn’t a reporting delay - it’s a charge that shouldn’t be there in the first place. Fraudulent transactions or billing errors can inflate your reported balance, pushing up your utilization ratio even though you didn’t make those purchases.

This is where DidIBuyIt comes in. The platform uses AI to analyze disputed transactions and generate detailed, bank-ready documentation that meets the standards of major payment networks like Visa, Mastercard, and Amex. By streamlining the dispute process, it helps you resolve issues faster.

Removing fraudulent or incorrect charges not only corrects your balance but also improves your credit score. If you spot an unrecognized charge or a billing error, using a structured dispute process like this is the quickest way to get your utilization back on track.

Key Takeaways on Credit Utilization Calculations

What to Remember About How Issuers Calculate Utilization

Credit utilization is determined by dividing the balance reported on your credit card statement by your total credit limit, then multiplying that result by 100. It's important to note that issuers report your balance as of the statement closing date - not your current balance - so your credit report reflects that figure.

Credit scoring models look at both the utilization of individual cards and your overall utilization across all revolving accounts. This means even if your total utilization is low, a high balance on just one card can still hurt your credit score.

To put things into perspective, data shows that lower utilization typically leads to higher credit scores. For instance, consumers with an 850 FICO® Score - the highest possible - average a utilization rate of just 4.1% [4].

Managing your utilization effectively requires taking proactive steps and addressing any disputed charges promptly.

How to Take Control of Your Utilization and Disputes

Here are some practical ways to keep your utilization in check:

- Pay off your balance a few days before your statement closing date to ensure a lower balance is reported.

- Keep older credit cards open to maintain a higher overall credit limit.

- Request periodic increases to your credit limit.

- Set up mobile alerts to notify you when your balance approaches 20–25% of your credit limit.

Disputed charges can also artificially inflate your balance and, in turn, your utilization rate. Tools like DidIBuyIt can simplify the dispute process by generating bank-ready documentation that aligns with major payment network standards, helping ensure any corrections are accurately reflected on your credit report.

FAQs

Why does my utilization stay high after I pay my card off?

Your credit utilization might stay elevated because issuers typically report your balances to credit bureaus at a specific point in your billing cycle - often before your payment is applied. If you make your payment after this reporting date, the higher balance is what gets recorded. To help reduce your utilization, consider paying down your balance a few days before your statement closing date. This way, a lower balance is reported to the credit bureaus.

What utilization percent is best for my credit score?

Keeping your credit utilization under 30% is usually ideal for maintaining a good credit score. However, for the best results, many experts suggest keeping it below 10%. A lower utilization rate reflects responsible use of credit, which can have a positive effect on your credit score.

Do charge cards and HELOCs count in utilization?

Charge cards typically don’t impact your credit utilization since they aren’t classified as revolving credit accounts. On the other hand, HELOCs (Home Equity Lines of Credit) are considered revolving credit and do influence your utilization ratio. Knowing the difference between these two can help you make smarter decisions when managing your credit score.