The Difference Between FICO and VantageScore Models

When it comes to your credit score, two main models dominate: FICO and VantageScore. Both use a 300–850 range to assess your creditworthiness, but they differ in how they evaluate your financial behavior, their eligibility criteria, and how lenders use them. Here's a quick breakdown:

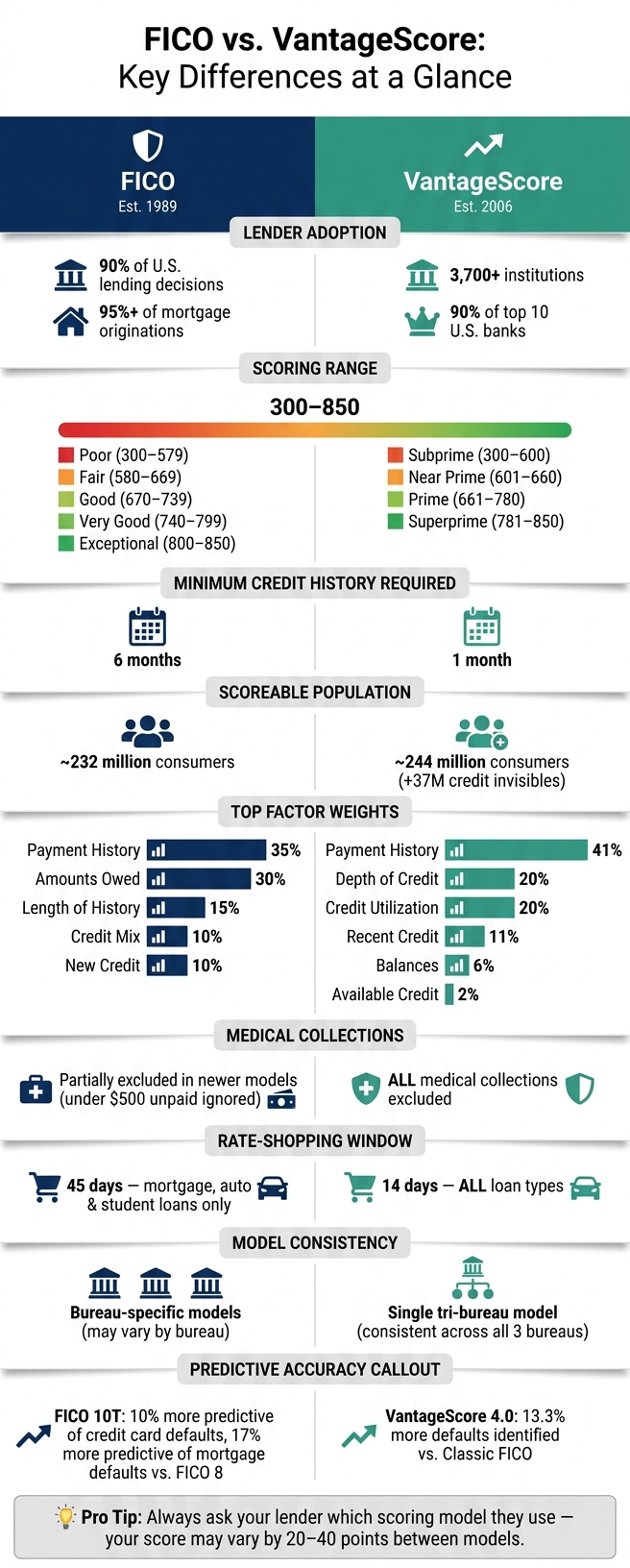

- FICO: Established in 1989, it's used in 90% of U.S. lending decisions. It requires at least six months of credit history and emphasizes payment history (35%) and credit utilization (30%). FICO's newer models, like FICO 10T, analyze trends over time for added accuracy.

- VantageScore: Created in 2006 by the three major credit bureaus, it requires just one month of credit history, making it more accessible to new borrowers. It weighs payment history even more heavily (41%) and excludes all medical collections.

Both models aim to predict the likelihood of a borrower falling behind on payments, but their scoring methods and lender preferences vary. Knowing which model your lender uses can help you better prepare for applications.

Quick Comparison

| Feature | FICO | VantageScore |

|---|---|---|

| Lender Adoption | 90% of lending decisions | Used by 3,700+ institutions |

| Minimum History | 6 months | 1 month |

| Medical Collections | Partially ignored in newer models | Fully excluded |

| Rate-Shopping Window | 45 days (mortgage, auto, student loans) | 14 days (all loan types) |

| Scoring Range | 300–850 | 300–850 |

To maintain a strong score, focus on paying bills on time, keeping balances low, and avoiding frequent new credit applications. Whether it's FICO or VantageScore, good habits will keep you on the right track.

FICO vs VantageScore: Key Differences at a Glance

FICO® vs. VantageScore®: Differences Explained

sbb-itb-5d40823

1. FICO

FICO has been a cornerstone of U.S. credit scoring since its launch in 1989. According to FICO's 2024 Annual Report, 90% of top U.S. lenders rely on FICO scores when making lending decisions. It’s also the go-to model for over 95% of U.S. mortgage originations, with more than 12 billion FICO scores sold annually to lenders across the country [6].

Scoring Ranges and Categories

FICO scores range from 300 to 850, with higher numbers indicating lower credit risk. Here's how lenders typically interpret these scores:

| FICO Score Range | Classification | What It Means for Borrowers |

|---|---|---|

| 800–850 | Exceptional | Access to the best rates and near-automatic approvals |

| 740–799 | Very Good | Competitive rates and approval for most products |

| 670–739 | Good | Standard access with moderate rate markups |

| 580–669 | Fair | Higher rates; often requires secured credit products |

| 300–579 | Poor | Limited options, often with high-APR subprime products |

Data Requirements and Eligibility

To calculate a FICO score, your credit file must meet two key criteria:

- At least one account must be open for six months.

- At least one account must have been reported to a credit bureau in the last six months [6][11].

If your credit history doesn’t meet these requirements, lenders may not be able to assess your creditworthiness. To address this, you could consider opening secured vs. unsecured credit cards or becoming an authorized user on someone else’s account to start building your credit profile [9].

FICO doesn’t factor in personal details like income, employment history, gender, marital status, or salary when calculating scores [7][8].

Factor Weights and Model Design

FICO evaluates your creditworthiness using five main factors:

| Factor | Weight | What's Being Measured |

|---|---|---|

| Payment History | 35% | Consistency of on-time payments, as well as delinquencies, collections, or bankruptcies |

| Amounts Owed | 30% | Credit utilization on revolving accounts |

| Length of Credit History | 15% | Age of accounts, including both the oldest and average account age |

| Credit Mix | 10% | Variety of credit types (e.g., credit cards, loans, mortgages) |

| New Credit | 10% | Recent hard inquiries and newly opened accounts |

For example, a single 30-day late payment on a strong credit profile (e.g., a 780 score) could drop the score by 90–110 points. On the other hand, a hard inquiry usually reduces a score by fewer than 5 points [9][11].

Behavioral Differences and Lender Usage

FICO continues to refine its models to better predict credit behavior. The newer FICO 10T model, for instance, doesn’t just evaluate whether you pay on time - it also looks at how you manage credit over time. By analyzing 24 months of balance trends, it differentiates between:

- Transactors: Those who pay off their balances in full each month.

- Revolvers: Those who carry balances from month to month.

This model has been shown to be 10% more predictive of credit card defaults and 17% more predictive of mortgage defaults compared to the older FICO 8 model [6]. Starting in March 2026, the Federal Housing Finance Agency (FHFA) will require Fannie Mae and Freddie Mac to adopt FICO 10T for mortgage underwriting, with full implementation expected by the end of 2026 [6].

To maintain a healthy FICO score, aim to:

- Keep credit utilization under 30% (with under 10% being ideal).

- Hold onto older accounts to boost your credit history.

- Submit rate-shopping applications within a 14-day window to minimize the impact of hard inquiries [6][9][10].

Next, we’ll explore how VantageScore takes a different approach to credit scoring.

2. VantageScore

While FICO has long been the go-to for credit scoring, VantageScore offers a fresh approach with some distinct advantages. Developed through a partnership between the three major credit bureaus - Equifax, Experian, and TransUnion - VantageScore uses a unified tri-bureau model. This structure ensures consistency in scores across all three agencies. Its adoption has grown rapidly: in 2024, usage jumped by 55%, with 42 billion scores issued. Today, over 3,700 institutions, including 90% of the top 10 U.S. banks, rely on VantageScore for various lending decisions [3][14].

Scoring Ranges and Categories

VantageScore models 3.0 and 4.0 share the same 300–850 scoring range as FICO, but their categories differ slightly. Instead of FICO's five tiers, VantageScore organizes scores into four categories:

| VantageScore Range | Category |

|---|---|

| 781–850 | Superprime |

| 661–780 | Prime |

| 601–660 | Near Prime |

| 300–600 | Subprime |

One key difference is the broader "Prime" range in VantageScore, which spans 661 to 780. For instance, a score of 675 is considered "Good" under FICO but lands squarely in the "Prime" category with VantageScore. This could impact lending rates and approval thresholds.

Data Requirements and Eligibility

VantageScore stands out for its ability to generate a score with just one month of credit history and one reported account within the last 24 months [2][14]. This is a much lower threshold than FICO's six-month minimum and stricter recency requirements. Because of this, VantageScore 4.0 can score an additional 37 million "credit invisibles" - people who typically wouldn't qualify for a FICO score [6].

The model also factors in alternative data like rent, utility, and telecom payments when reported to credit bureaus. Additionally, it treats Buy Now, Pay Later (BNPL) accounts as installment loans. On the collections front, VantageScore is more lenient: it ignores paid collection accounts and excludes all medical collections, regardless of the amount owed [6][12][3].

Factor Weights and Model Design

VantageScore 4.0 prioritizes payment history more heavily than FICO - 41% versus 35%. On the other hand, it places less emphasis on credit utilization, assigning it 20% compared to FICO's 30%. The model also includes factors that FICO doesn't track separately, such as Balances (6%) and Available Credit (2%) [3][13][14].

| Factor | VantageScore 4.0 Weight |

|---|---|

| Payment History | 41% |

| Depth of Credit | 20% |

| Credit Utilization | 20% |

| Recent Credit | 11% |

| Balances | 6% |

| Available Credit | 2% |

These differences in weighting highlight how VantageScore evaluates credit behavior in a unique way.

Behavioral Differences

VantageScore 4.0 adds another layer of precision by analyzing 24 months of balance behavior. For example, consistently paying more than the minimum on credit cards can positively impact your score over time [16][12]. The model also uses machine learning to assess "thin" or dormant credit files, improving score predictability by 10% for these profiles [15].

When it comes to hard inquiries, VantageScore deduplicates all inquiries within a 14-day window, regardless of credit type - including credit cards. By contrast, FICO applies a longer 45-day deduplication period, but only for mortgage, auto, and student loan inquiries [2][12].

Lender Usage and Implications

VantageScore's evolving methodology is reshaping how lenders evaluate borrowers. A major milestone came in July 2025, when the Federal Housing Finance Agency (FHFA) approved VantageScore 4.0 for conventional mortgages sold to Fannie Mae and Freddie Mac. This ended FICO's exclusive hold on that market [14]. For borrowers, this means that even if their FICO score isn't up to par, they might still qualify for a mortgage under VantageScore.

Jonathan Ernest, Assistant Professor of Economics at Case Western Reserve University, explained the impact:

"Now, a few more people who are on the margin move from being denied that loan at a favorable rate to receiving the loan." [14]

If you're applying for a mortgage, it's worth checking which scoring model your lender uses. Your score could vary significantly, and that difference might just tip the scales in your favor.

Pros and Cons

The comparison below breaks down the key differences between FICO and VantageScore, highlighting how each impacts lender decisions and consumer credit considerations. Both models offer distinct benefits and limitations, which can influence their suitability depending on your credit profile and the type of application.

| Feature | FICO | VantageScore |

|---|---|---|

| Lender Adoption | Used in 90% of lending decisions [18] | Used by 3,700+ institutions, including top 10 U.S. banks [14] |

| Minimum Credit History | Requires 6 months of credit history [12] | Requires just 1 month of credit history [2] |

| Scoreable Population | ~232 million consumers [3] | ~244 million consumers [3] |

| Medical Collections | Newer models reduce the weight of collections and ignore unpaid collections under $500 [1] | Ignores all medical collections entirely [5] |

| Rate-Shopping Window | 45 days for mortgages, auto, and student loans [14] | 14 days for all loan types [14] |

| Model Consistency | Bureau-specific models [1] | Single tri-bureau model across all three agencies [1] |

| Predictive Accuracy | FICO Score 10 T detects 18% more defaulters in mortgage origination [14] | VantageScore 4.0 identifies 13.3% more defaults than Classic FICO [17] |

Key Insights

FICO has a long-standing reputation in the lending industry, particularly for mortgage and auto loans. Its 45-day rate-shopping window offers borrowers a more extended period to compare loan options without negatively affecting their credit score. However, FICO's requirement of at least six months of credit history can be a challenge for individuals just starting to build credit.

VantageScore, on the other hand, focuses on accessibility. It allows scoring for consumers with as little as one month of credit history, covering approximately 12 million more people than FICO [3]. Additionally, its approach to medical collections is more consumer-friendly, as it excludes all medical collections - paid or unpaid - while FICO only partially addresses this issue in its newer models.

When it comes to predictive accuracy, both models claim advancements. FICO Score 10 T is noted for detecting 18% more defaulters in mortgage originations compared to its Classic model [14]. VantageScore 4.0, however, claims to identify 13.3% more defaults across all loan types than Classic FICO [17].

Jim Wehmann, former President of Scores at FICO, emphasized FICO's edge in improvement:

"FICO Score 10 T's improvement over Classic FICO was shown to be five times better than VantageScore 4.0's improvement." [14]

Ultimately, neither model is a one-size-fits-all solution. Each is designed with different priorities, and understanding these distinctions can help you decide which score aligns best with your credit situation and financial goals.

Conclusion

FICO and VantageScore take different approaches to assessing creditworthiness. While FICO remains the primary choice for most U.S. lenders, VantageScore is gaining traction. Understanding these differences can help you navigate your financial decisions more effectively.

One key takeaway for borrowers is to ask lenders which scoring model they use before applying for significant loans. For instance, mortgage lenders often stick to older FICO versions (like FICO 2, 4, or 5), whereas credit card issuers may pull a VantageScore. Keep in mind, the score you see through free credit monitoring tools might differ from your lender's version by as much as 20 to 40 points [6].

Matt Schulz, Chief Credit Analyst at LendingTree, emphasizes the importance of consistent habits:

"If you do these things consistently for years - paying bills on time, keeping balances low, and avoiding frequent applications - your credit is going to be just fine." [4]

To improve both FICO and VantageScore, focus on paying bills on time, keeping your credit utilization under 30%, and avoiding multiple new accounts in a short period. For VantageScore specifically, paying off old collection accounts can lead to immediate improvements, even if older FICO models take longer to reflect those changes [14]. Ultimately, practicing good credit habits will help maintain a strong score, no matter the model.

FAQs

Why is my FICO score different from my VantageScore?

FICO and VantageScore use distinct methods to assess your credit report, which can cause differences in your credit score. For example, VantageScore only needs one month of credit history to calculate a score, whereas FICO usually requires at least six months. Moreover, the two models prioritize factors like recent credit activity and missed payments differently, which ultimately influences the score you receive.

Which credit score does my lender actually use?

Lenders often rely on either a FICO score or a VantageScore, as both are commonly used in credit evaluations. The choice between the two depends on the lender's specific requirements and preferences. To be ready for any lender's assessment, it’s wise to keep an eye on both types of scores.

How can I build credit if I don’t have 6 months of history?

If you’re starting with less than six months of credit history, there are still ways to begin building your credit. Options include becoming an authorized user on someone else’s credit card, applying for a secured credit card, or taking out a credit-builder loan. These methods can help you establish a credit profile, even when your history is limited.