The Rise of A2A Payments and What Merchants Should Know

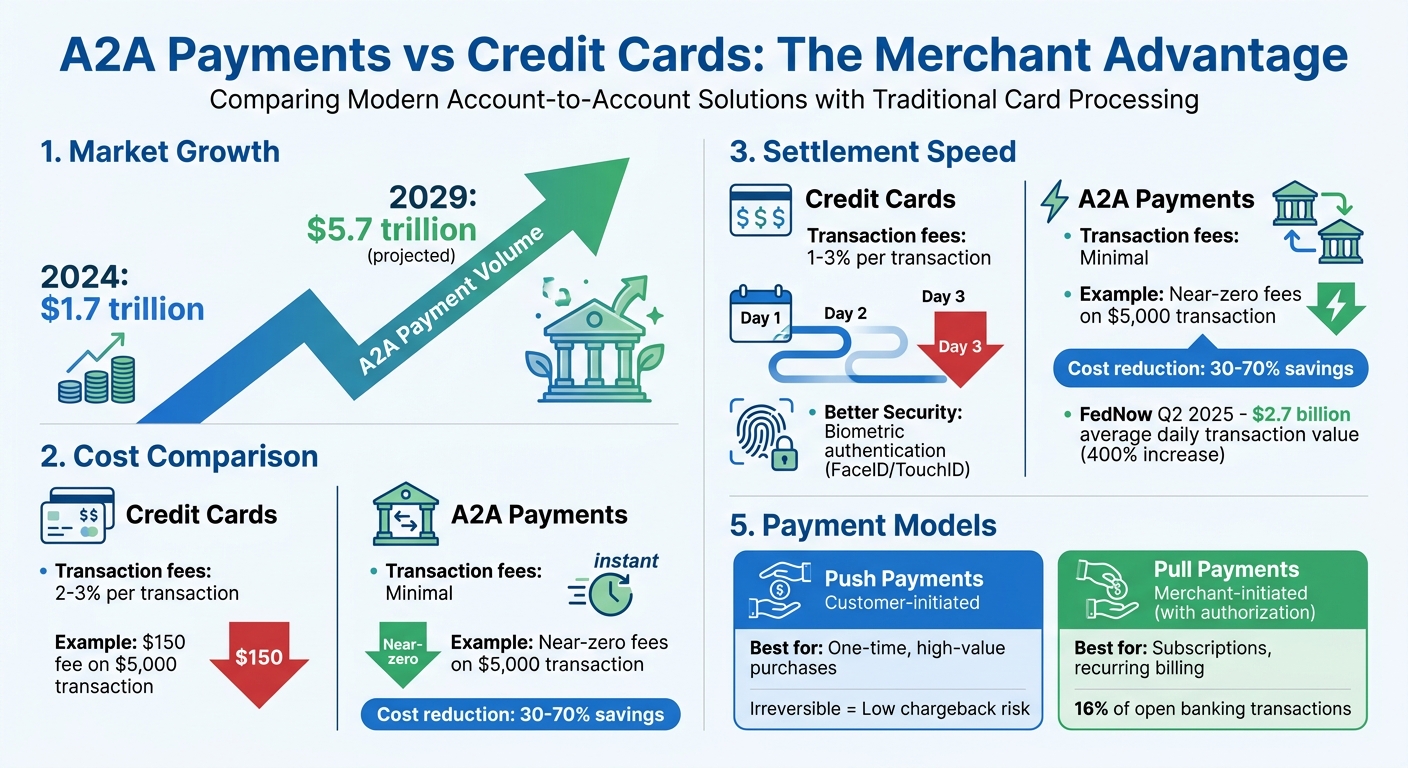

Account-to-Account (A2A) payments are transforming how businesses handle transactions. These direct bank-to-bank transfers bypass card networks, offering faster settlements, lower fees, and a smoother experience for both merchants and customers. With real-time systems like FedNow and RTP in the U.S., A2A payments are gaining traction, projected to grow from $1.7 trillion in 2024 to $5.7 trillion by 2029.

Key Takeaways:

- Cost Savings: A2A payments cut out card fees (2–3%) and reduce processing costs significantly.

- Faster Settlements: Instant or same-day access to funds improves cash flow.

- Improved Customer Experience: Payments are authenticated directly through banking apps, often using biometrics.

- Push and Pull Models: Push payments are customer-initiated, ideal for one-time purchases. Pull payments work well for subscriptions and recurring billing.

Challenges:

- Fraud Prevention: Real-time fraud detection tools are critical as these payments are irreversible.

- Dispute Resolution: Unlike cards, A2A lacks standardized chargeback processes, making AI tools essential for managing disputes.

- Integration Complexity: Aligning A2A systems with existing infrastructure requires careful planning.

Merchants can benefit by integrating A2A payments strategically, focusing on high-value or recurring transactions, and ensuring robust security measures. Tools like AI-powered dispute platforms and real-time fraud detection can address key challenges, making A2A payments a practical and efficient option for businesses.

A2A Payments vs Credit Cards: Cost Savings and Settlement Speed Comparison

How A2A Payments Work - The Briefing | On The Wire

sbb-itb-5d40823

Benefits of A2A Payments for Merchants

Switching to Account-to-Account (A2A) payments brings several advantages, including reduced costs, faster access to funds, and a smoother checkout process. These benefits not only lower expenses but also improve efficiency and customer satisfaction.

Lower Transaction Costs

Processing payments with credit cards often comes with hefty fees - interchange fees, scheme fees, and gateway charges typically add up to 2–3% per transaction. A2A payments cut out these middlemen by securely transferring money directly from the customer's bank to the merchant's bank via APIs.

For example, on a $5,000 transaction, A2A fees are minimal compared to the $150 fee a credit card would typically charge. In early 2026, eBay UK teamed up with TrueLayer to introduce "Pay by Bank" at checkout, showcasing how major platforms are adopting this cost-saving solution [1].

Additionally, A2A payments help merchants avoid costs tied to chargebacks and the "passive churn" caused by expired credit cards in recurring billing. Since bank mandates don’t expire like credit cards, merchants save on re-acquisition costs. Faster settlements also improve cash flow, making this method even more appealing.

Faster Payment Settlement

Credit card payments often take 1–3 business days to settle, while A2A payments can process in seconds or hours, offering near-instant liquidity [6]. For example, in Q2 2025, FedNow saw its average daily transaction value skyrocket by over 400% to $2.7 billion, highlighting the growing popularity of instant settlements [2].

This speed provides a major advantage for managing cash flow.

"Real-time A2A payments are typically irrevocable... This provides certainty and immediate settlement for merchants, making this payment option highly attractive from a cash flow and risk perspective."

- Raluca Constantinescu, Domain Lead Editor at The Paypers [2]

Immediate payment reconciliation also reduces administrative work, helping businesses operate more efficiently. Even government agencies are adopting this model. By March 2026, HM Revenue & Customs (HMRC) in the UK processed over £2.3 billion in tax payments via "Pay by Bank", a 64% increase compared to the previous year [1].

Better Customer Experience

A2A payments don’t just save money and time - they also simplify the customer experience. Instead of entering long card details, customers authenticate payments directly through their banking app, often using biometrics like FaceID or TouchID [5]. The process is faster and more intuitive than traditional methods like 3D Secure challenges, and payments are confirmed instantly [7].

This direct bank authentication also improves approval rates by bypassing card issuer risk assessments [5]. Merchants can even pass on their savings by offering discounts or loyalty rewards for choosing "Pay by Bank" at checkout [7]. In the UK, awareness of "Pay by Bank" options has reached an impressive 90%, signaling growing trust in this payment method [1].

Push vs. Pull A2A Payment Models

A2A payments operate through two main models: push and pull. Choosing the right model for your business can impact costs, cash flow, and the overall customer experience.

Push payments are initiated by the customer. In this model, the buyer logs into their banking app, authenticates using biometrics like FaceID or TouchID, and transfers money directly to the merchant's account. This approach is ideal for one-time purchases - especially high-value items like electronics, furniture, or professional services - where avoiding traditional card processing fees can make a big difference. Since push payments are typically irreversible, merchants benefit from immediate financial certainty and minimal risk of chargebacks.

On the other hand, pull payments place the initiation process in the hands of the merchant. After a customer provides prior authorization - often through a mandate or Variable Recurring Payment (VRP) consent - the merchant can initiate payments as needed. This model is well-suited for recurring payments such as subscriptions or utility bills. For example, in November 2025, Visa facilitated its first commercial VRP transaction in the UK, enabling a real-time energy bill payment from Kroo Bank to the utility provider Utilita [1]. Currently, VRPs account for about 16% of open banking transactions [1], gaining popularity due to their ability to combine flexible payment amounts with instant settlement, making them a strong fit for usage-based billing.

Each model has its strengths and challenges. Push payments give customers full control but rely on their timely action, which can result in missed payments. Pull payments, by contrast, automate the process, providing predictable cash flow and reducing manual effort. However, they carry a higher risk of disputes, as charges can be reversed if not canceled in time.

"Pay by Bank and broader real-time A2A payments represent a structural reconfiguration of UK payments infrastructure. They reduce systemic costs, improve liquidity velocity, and create programmable payment capabilities"

- Marcus Hickman, Founder of Davies Hickman [1]

To make the most of these models, merchants often use a hybrid strategy. For instance, they may start new customers on card payments and later transition repeat buyers to A2A payment systems to improve cost efficiency [9].

How to Implement A2A Payments

To take full advantage of the cost savings, speed, and improved customer experience offered by A2A payments, you need to align the system with your business model and ensure it meets security standards.

Define Your Business Model Needs

Start by identifying where A2A payments can make the biggest impact on your operations. For high-ticket transactions, the cost savings are particularly noticeable, making this method a great fit for industries dealing with large payments. Similarly, businesses with recurring subscriptions - like utilities, insurance, or memberships - can benefit from avoiding issues like expired cards or failed renewals. If you're in high-volume e-commerce, even small reductions in per-transaction fees can lead to substantial savings. For instance, Pay-by-Bank solutions can cut processing costs by 30% to 70% compared to credit cards[6].

However, keep in mind that A2A payments don’t support automated chargebacks, so it’s important to review and adjust your refund policies accordingly[5]. Once your business needs are clear, you can move on to selecting the most suitable payment rails.

Choose the Right Payment Rails

The choice of payment rails depends on how quickly you need funds to settle. For non-urgent, bulk transactions, ACH remains a reliable and affordable option, costing around $0.50 per transaction with settlement times of one to three business days[3]. On the other hand, instant payment solutions like RTP and FedNow are better for situations where speed is critical. These real-time networks, while slightly more expensive than ACH, are still far cheaper than credit card fees, which typically average around 3%[3].

Real-time rails are ideal for scenarios like gig economy payouts, insurance claims, or high-value e-commerce purchases where customers expect immediate confirmation. Adoption is growing rapidly - over 40% of companies with revenues exceeding $100 million already use RTP, and nearly 70% plan to adopt RTP or FedNow by 2027[11]. Additionally, global benchmarks like the EU’s Instant Payments Regulation, which mandates euro transfers within 10 seconds, highlight the increasing demand for real-time solutions[5].

Ensure Compliance and Security

After selecting your payment rails, focus on securing and streamlining your processes. Compliance and security are non-negotiable. For example, the Consumer Financial Protection Bureau’s proposed "Personal Financial Data Rights" rule, introduced in October 2023, ensures consumers have the right to share financial data securely[12]. For ACH payments, follow Nacha’s strict rules on authentication and data handling[12].

Use Strong Customer Authentication methods, such as biometrics (e.g., FaceID or fingerprint scanning), combined with OAuth 2.0 protocols, to verify users. Implement tokenization to replace sensitive account data with unique identifiers, reducing the risk of breaches[12]. Modern API-based account verification tools can confirm accounts in just seven seconds, compared to the days required by traditional micro-deposits[3].

Fraud prevention is equally important. Real-time fraud detection tools, like Plaid Signal, can help mitigate risks associated with ACH payments[3]. With friendly fraud now accounting for 70% of all fraud cases, according to Mastercard[10], continuous monitoring is essential. Partner with payment providers that prioritize security and offer consistent uptime[12]. Keep in mind that real-time A2A transfers are typically irrevocable, so robust fraud prevention measures are critical[6].

AI for A2A Transaction Dispute Resolution

A2A payments simplify transactions, but resolving disputes remains a tough hurdle for merchants. One of the biggest issues is the lack of effective dispute resolution mechanisms. Unlike credit cards, which have built-in chargeback processes, A2A transactions often lead to prolonged standoffs between banks - sometimes dragging on for months [10]. Roenen Ben-Ami, Co-Founder and Chief Risk Officer at Justt, highlights the problem:

"The lack of standardized dispute resolution mechanisms frequently results in bank vs bank standoffs, frustrating attempts at resolution." [10]

This is where AI-powered tools like DidIBuyIt step in. By automating evidence collection, these platforms make dispute resolution more efficient. With friendly fraud now accounting for 70% of all fraud cases and nearly 40% of European cardholders admitting to filing false disputes [10], having a structured approach is more important than ever.

AI-Powered Dispute Analysis

AI tools bring precision to dispute resolution by analyzing transaction patterns, histories, and supporting evidence to assess the likelihood of a favorable outcome. This is particularly valuable given that many A2A payment systems don’t allow merchants to submit their own evidence [10]. Advanced platforms even use "win-prediction scoring" to prioritize disputes worth pursuing, boasting win rates of up to 85% - about three times better than manual methods [16][17].

For instance, in early 2026, GitHub Sponsors adopted Stripe's AI-powered Smart Disputes to handle chargebacks. Before using AI, they rarely contested disputes due to the time and effort involved. With AI automating evidence compilation and submission, the team cut dispute-related work by 20 hours per month and significantly boosted recaptured revenue [13]. Beyond analysis, these tools also create documentation tailored for bank review, speeding up the resolution process.

Bank-Ready Documentation

Platforms like DidIBuyIt create structured, bank-ready documentation that simplifies processing. The AI gathers transaction details, deliverables, acceptance criteria, and dispute history, then uses large language models (LLMs) to produce detailed reasoning for resolution [18]. PayPal, for example, reported in May 2026 that its AI-powered dispute system reduced resolution times by 80%. By automating repetitive tasks and equipping human agents with AI-generated insights, the platform mitigates chargeback impacts and improves efficiency [14].

Guided Recovery Processes

AI doesn’t stop at documentation - it also streamlines fund recovery with guided processes. These tools offer step-by-step instructions for recovering funds, automating evidence collection, ensuring secure data handling, and providing real-time tracking. This guided approach is especially valuable since A2A payments lack the automated representment process found in card systems [5].

DidIBuyIt enhances this process with encrypted data management, 24/7 customer support, and real-time success tracking throughout disputes. By automating evidence collection and reusing documentation, merchants save time and boost their chances of success [13]. The platform also monitors "Notifications of Fraud" (NOF) from banks, enabling early reviews and proactive refunds for suspicious transactions. This helps merchants avoid formal dispute fees and maintain their reputation [15][17]. These capabilities make A2A payments even more appealing by reducing costs and streamlining operations for merchants.

Challenges and Solutions for A2A Adoption

While A2A payments bring clear benefits, they face significant hurdles, particularly with older systems designed for batch processing rather than the real-time demands of A2A platforms like FedNow [4]. Oscar Herrera from GridGain sums it up:

"The harder job is running pay-by-bank flows in real time: fraud checks, routing, reconciliation, and failover, all without ripping out the core systems already in place." [4]

Another challenge is the fragmented nature of regional payment schemes - such as Pix in Brazil, UPI in India, and iDEAL in the Netherlands - requiring merchants to navigate multiple regional integrations [2][19]. The lack of standardized dispute processes adds complexity, and with Authorized Push Payment fraud expected to reach $7.6 billion by 2028 across six key markets, merchants need proactive strategies to address these issues [2]. Tackling trust, integration, and fraud prevention is critical to overcoming these obstacles.

Building User Trust

Encouraging customers to embrace A2A payments means focusing on education and transparency. For example, in the UK, 90% of consumers now recognize the "Pay by Bank" term, but recognition alone doesn’t guarantee trust [1]. Since A2A transfers are irreversible - unlike card chargebacks - clear communication about the process is essential.

One way to build trust is by showcasing successful implementations. When eBay UK partnered with TrueLayer in 2026 to offer "Pay by Bank" at checkout, millions of users were introduced to the technology in a familiar context [1]. Similarly, HM Revenue & Customs processed over $2.3 billion in tax payments via Pay by Bank by March 2026, reflecting a 64% year-over-year increase and demonstrating how institutional adoption can normalize the method [1]. Merchants should highlight bank-level security, explain that no card details are stored, and use Verification of Payee services to reassure customers their funds are going to the right place [2][8].

Managing Integration Complexities

Integrating A2A payments doesn’t require a complete system overhaul. Instead, many merchants are opting for real-time layers that connect legacy systems to modern A2A payment rails [4]. For instance, a major global bank used GridGain's in-memory compute platform in 2025–2026 to link its mainframe with the STET instant-payments environment. This allowed the bank to handle ISO-to-COBOL transformations within strict timing requirements without altering its core infrastructure [4].

Payment orchestration layers and prebuilt APIs simplify the process further, enabling merchants to manage multiple A2A schemes through a single integration [19][8]. Choosing providers that offer end-to-end solutions for collection, reconciliation, and settlement can eliminate manual accounting delays. A phased rollout - starting with repeat customers before expanding to new buyers - can also help streamline adoption [1].

Preventing Fraud

Fraud prevention is critical for A2A payments, as these transactions settle instantly. This means fraud detection must happen in real time, before the payment is completed, rather than through post-transaction batch reviews [4]. Advanced systems now use machine learning to analyze transactions in just 10–20 milliseconds, processing up to 25,000 transactions per second [4]. For example, a leading financial analytics firm utilized GridGain to achieve real-time fraud detection within the payment window [4].

To further secure A2A payments, merchants should implement strong, multi-factor authentication through banking apps [8]. Name-matching services like Verification of Payee can prevent funds from being sent to the wrong recipient - a requirement under the EU’s Instant Payments Regulation by late 2025 [2]. Educating users about phishing and other social engineering risks is also essential, as these systems are frequent targets for such attacks.

Conclusion

A2A payments are transforming how merchants handle transactions, with rapid global adoption positioning them as a key payment option for the future. They offer merchants the chance to cut processing costs compared to credit cards, access funds instantly, and reduce exposure to chargebacks [6]. These benefits make A2A payments especially appealing for high-value purchases, B2B invoices, and recurring billing scenarios.

To make the most of A2A payments, merchants should take a strategic, step-by-step approach to integration. Start by pinpointing where A2A payments can provide the greatest value - whether that’s eliminating interchange fees on big-ticket items or simplifying subscription payments through Variable Recurring Payments. Offering A2A alongside traditional card payments ensures customers have options while helping merchants optimize costs [6]. Collaborating with experienced payment processors can ease the complexity of bank integrations, and implementing verification services can prevent errors like misdirected payments.

Building customer trust is essential, and this starts with measures like real-time fraud detection and strong authentication through banking apps. Features such as name-matching verification and advanced authentication methods help avoid errors and identify potential issues before irreversible transfers take place.

Finally, merchants must address the unique challenges of disputes in A2A payments. Unlike traditional card networks, A2A lacks established dispute frameworks, making tools like DidIBuyIt invaluable. These AI-powered platforms assist merchants by analyzing disputes, creating bank-ready documentation, and guiding recovery processes. By leveraging these tools and adopting robust integration strategies, merchants can unlock the full potential of A2A payments - reducing costs, speeding up cash flow, and staying competitive in a world that’s increasingly leaning toward real-time payments.

FAQs

Which A2A rail should I use - ACH, RTP, or FedNow?

The best account-to-account (A2A) rail depends on what your business prioritizes - whether it’s speed, cost, or availability.

- ACH: A budget-friendly option for non-urgent payments, typically settling within 1–3 business days. Perfect for situations where time isn’t critical.

- RTP: Designed for instant settlement, making it ideal for immediate transactions. It also reduces the risk of chargebacks, which is a big plus for many businesses.

- FedNow: As a newer system, it enables real-time settlement across the U.S. banking network. It's expected to become an important player in the instant payments space.

Each of these options serves different needs, so the choice depends on what aligns best with your payment strategy.

How do refunds and disputes work with A2A if there are no chargebacks?

When it comes to A2A payments, handling refunds and disputes operates quite differently since chargebacks aren’t an option. Instead, disputes are usually settled directly between the bank accounts involved. This often means manual intervention is needed to sort things out.

For merchants, having solid verification and reconciliation processes in place is crucial to address potential errors or fraud effectively. In some cases, open banking systems may shift more responsibility onto customers. However, certain banks take steps to offer refunds as a way to maintain customer trust.

Providing proactive and responsive customer service plays a key role in ensuring disputes are resolved smoothly and efficiently.

What controls do I need to prevent fraud on real-time A2A payments?

To combat fraud in real-time A2A payments, it's essential to have safeguards that can identify and address threats instantly. This means using AI-powered fraud detection tools that provide real-time risk scoring, ensuring robust customer identity verification, and employing flexible models capable of adapting to changing scam tactics. Pairing continuous monitoring with AI-driven insights significantly improves the ability to spot and stop scams, including account takeovers, as they happen.