How Real-Time Payments (RTP) Differ from ACH for Fraud Recovery

Real-Time Payments (RTP) and Automated Clearing House (ACH) systems handle fraud recovery in fundamentally different ways. The key differences are:

- Speed: RTP processes transactions instantly, while ACH takes 1–3 business days.

- Reversibility: RTP transactions are final and cannot be reversed, whereas ACH allows reversals under specific conditions with consumer protections extending up to 60 days or more.

- Fraud Prevention: RTP prioritizes pre-transaction fraud prevention due to its instant settlement, while ACH benefits from a longer processing window to detect and address suspicious activity.

- Cost: RTP transactions are cheaper at $0.045 each, compared to ACH’s $0.26–$0.50 per transaction.

Quick Comparison:

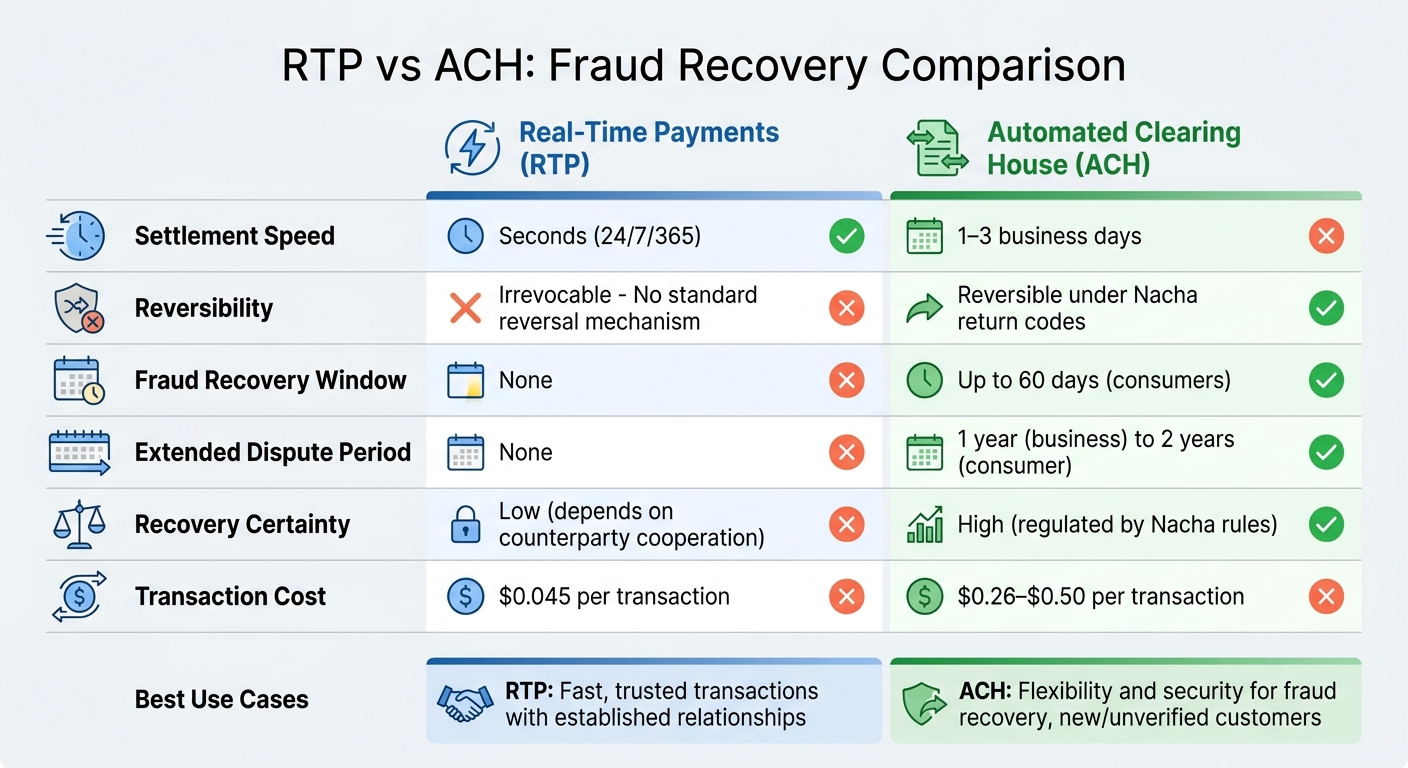

| Feature | Real-Time Payments (RTP) | Automated Clearing House (ACH) |

|---|---|---|

| Settlement Speed | Seconds (24/7/365) | 1–3 business days |

| Reversibility | Irrevocable | Reversible under Nacha rules |

| Fraud Recovery Window | None | Up to 60 days (consumers) |

| Cost per Transaction | $0.045 | $0.26–$0.50 |

In short, RTP is ideal for fast, trusted transactions, while ACH offers more flexibility and security for fraud recovery. Your choice depends on balancing speed with risk tolerance.

RTP vs ACH Fraud Recovery Comparison Chart

1. Real-Time Payments (RTP)

Fraud Detection

Real-Time Payments demand fraud detection to happen instantly, as settlements occur within seconds and cannot be reversed. This is a significant departure from traditional systems, which often review suspicious transactions after they’ve been completed [7][3]. To combat fraud, financial institutions pause transactions in real time while detection systems analyze behavioral data, such as typing patterns, mouse movements, and device handling, to identify unusual activity. With the RTP network now covering 65% of U.S. demand deposit accounts, this proactive approach has become essential [7].

The credit-push model used in RTP eliminates unauthorized debit fraud by preventing "pull" debits. However, it introduces risks like Authorized Push Payment (APP) fraud, where individuals are tricked into willingly sending money. Social engineering tactics can exploit the irreversible nature of these payments, making prevention critical [7].

This focus on immediate detection highlights the challenges of recovering funds after a transaction is complete.

Fraud Recovery Timelines

One of RTP's defining features is the finality of transactions. Once a payment is processed, it cannot be automatically reversed. A sending bank may request the return of an incorrect payment, but the receiving bank is under no obligation to comply [4].

Consumer Protections

Given the irrevocable nature of RTP transactions, consumer protection efforts prioritize prevention over post-transaction remedies. Banks implement safeguards such as multi-factor authentication, dual approvals, and identity verification before authorizing payments. Additionally, many institutions restrict RTP access to commercial clients or require customers to enroll specifically, creating an extra layer of security against fraud [3][4][6].

When disputes arise, they are typically resolved directly between the involved parties or through a "Request for Return of Funds" message. However, the receiving bank is not legally required to return the funds [4][6].

"If you can keep bad actors out of your system from the jump, they won't be able to exploit your real-time payment methods."

AI-Driven Tools

AI-driven tools are playing a key role in strengthening pre-authorization defenses for RTP. These tools analyze data at lightning speed to detect anomalies based on historical patterns [7]. Techniques like tokenization protect sensitive data, while balance checks ensure funds are available before a transaction proceeds [4]. This technology supports a "friction-right" approach, where multi-factor authentication is applied only to high-risk transactions, maintaining a balance between security and a smooth user experience [7].

sbb-itb-5d40823

2. Automated Clearing House (ACH)

Fraud Detection

ACH fraud detection benefits from its one-to-three-day batch processing window, which provides a crucial opportunity to identify suspicious activity before transactions are finalized [3]. During this time, banks conduct identity verification, perform balance checks to avoid "Insufficient Funds" returns, and rely on Know Your Customer (KYC) protocols to flag potentially fraudulent transactions [4].

The batch processing system allows both the sender and receiver to catch errors or unauthorized activity and request reversals before settlement. Many modern platforms now use machine learning to enhance fraud detection during onboarding and transactions, minimizing the need for manual reviews. However, ACH's limitation to business days and banking hours can delay fraud detection over weekends and holidays, unlike RTP's continuous availability [6].

"The added time that it takes ACH payments to process allows the paying party more time to recognize if there's a problem with the transaction, providing the opportunity to request a reversal."

- Sara Seguin, Global Head of Product Marketing and Strategic Advisory, Alloy [6]

This extended processing period allows ACH to implement flexible and reversible fraud recovery measures.

Fraud Recovery Timelines

ACH stands out from RTP with its built-in reversibility, which makes fraud recovery more feasible. ACH transactions can be reversed for reasons such as insufficient funds (R01) or closed accounts (R02), with standard returns processed within two banking days [4]. For unauthorized transactions, consumers have up to 60 calendar days to initiate a return [4][2].

Recovery windows extend even further for specific cases: businesses can file claims for up to one year, while consumer accounts have up to two years to address unauthorized transactions [4]. For errors like duplicate payments or incorrect recipients, reversals must be initiated within 24 hours of discovery and no later than five banking days after settlement [6]. Starting April 1, 2025, Receiving Depository Financial Institutions (RDFIs) will need to respond to "Request for Return" status messages within 10 banking days [5].

Consumer Protections

ACH provides strong consumer protections, offering a safeguard against unauthorized or incorrect transactions. This "safety net" allows consumers to dispute unauthorized transfers under Nacha rules, with unauthorized returns (e.g., Code R10) permitted within 60 calendar days of the transaction. For consumer accounts, additional protections extend the window to two years for filing claims [4].

The batch processing system gives financial institutions ample time to detect fraud and process reversals [1]. Tokenization helps protect sensitive banking information, while real-time webhooks notify businesses immediately of returns. Unlike RTP's near-instant settlement, which leaves no room for reversals, ACH's multi-day review period ensures a more secure process [4][2].

To further enhance security, ACH platforms are increasingly incorporating advanced AI tools to identify and prevent fraudulent activity.

AI-Driven Tools

AI tools play a key role in ACH fraud prevention by analyzing patterns within the batch processing window. These systems leverage machine learning to review transaction histories, monitor IP addresses, and detect unusual changes to personally identifiable information (PII). If suspicious activity is flagged, accounts can be frozen or payments rejected before settlement, taking advantage of ACH's one-to-three-day processing period [6].

Payment APIs now offer real-time webhooks and micro-deposit validation, particularly for high-value transfers. Businesses are encouraged to adopt multi-factor authentication (MFA) and tiered access controls to enhance security. For example, new users might first need to establish a history of successful standard ACH transactions before gaining access to faster options like Same Day ACH [4]. With an average transaction cost between $0.26 and $0.50, businesses can afford to implement multiple fraud prevention measures without significantly affecting costs [1].

Tech Talk: The Road to Real Time Payments

Advantages and Disadvantages

Choosing between RTP and ACH for fraud recovery requires weighing their distinct trade-offs. RTP offers instant, always-available settlement, but its transactions are final - recovery relies entirely on the recipient's willingness to cooperate[3][6].

On the other hand, ACH settles within one to three business days and allows for reversals under Nacha return codes. These include a 60-day window for consumer claims and up to two years for certain disputes[8][9]. The table below highlights the key differences between the two payment systems.

| Feature | Real-Time Payments (RTP) | Automated Clearing House (ACH) |

|---|---|---|

| Settlement Speed | Seconds (24/7/365)[3][5] | 1–3 business days[3][6] |

| Reversibility | Irrevocable; no standard reversal mechanism[3][6] | Reversible under Nacha return codes[8][6] |

| Unauthorized Return Window | None[6] | 60 calendar days (consumers)[8][9] |

| Extended Dispute Period | None | 1 year (business) to 2 years (consumer)[8][9] |

| Recovery Certainty | Low (depends on counterparty cooperation)[6] | High (regulated by Nacha rules)[8][6] |

| Transaction Cost | $0.045 per transaction[1] | $0.26–$0.50 per transaction[1] |

"Real-time payments aren't about moving everything faster. They're about choosing where speed actually creates leverage."

This comparison highlights the importance of aligning payment methods with risk tolerance and operational needs. ACH provides a safety net with its reversal options, making it an appealing choice for businesses prioritizing fraud protection and cost efficiency. In contrast, RTP shines in scenarios where speed is critical and fraud risk is minimal, such as payroll or pre-authorized payments.

"With faster payment rails comes faster fraud. And just like with all the other new technologies... fraudsters will continue to adapt and figure out new ways to exploit these new technologies."

- Sara Seguin, Global Head of Product Marketing and Strategic Advisory, Alloy[6]

Conclusion

Fraud recovery strategies differ significantly between ACH and RTP systems. ACH payments offer a built-in safety net with features like return codes and extended dispute windows - up to 60 days for consumers and, in some cases, as long as two years. On the other hand, RTP transactions are final, meaning any recovery hinges on the recipient voluntarily returning the funds[9].

When working with high-risk scenarios, such as new vendors or unverified customers, ACH’s reversibility provides an added layer of protection. Conversely, RTP's speed makes it an excellent choice for transactions involving trusted, long-established relationships. A smart approach might include tiered access: requiring new users to complete successful ACH transactions before granting them RTP privileges. To further reduce risk, implement strong pre-payment controls like multi-factor authentication and dual approvals, especially since RTP transactions cannot be reversed. AI-powered tools can also play a key role by offering real-time monitoring and dispute analysis, potentially identifying red flags before they escalate.

Selecting the right payment method comes down to understanding your risk tolerance and operational needs. Tailoring your approach to align with these factors is key to managing fraud effectively.

FAQs

What should I do if I send an RTP payment to the wrong person?

If you accidentally send an RTP payment to the wrong recipient, it’s crucial to act fast. Since RTP transactions are final and irreversible once processed, time is of the essence. Reach out to your bank or payment provider right away to report the mistake and ask for assistance. Keep in mind, recovering the funds often relies on the recipient’s willingness to cooperate and any security measures in place before the transaction.

To avoid similar mistakes in the future, implement robust approval processes and thorough fraud checks before initiating payments. These steps can help reduce the risk of errors and ensure smoother transactions.

How do ACH return codes work for fraud and disputes?

ACH return codes are like little messages that explain why an ACH transaction didn’t go through or was challenged - kind of like credit card chargebacks. There are about 70 different codes, each pointing to a specific problem. For example, R01 means there weren’t enough funds in the account. These codes also come with set timeframes for action, making it easier for banks to handle fraud or unauthorized transactions. They ensure disputes are resolved quickly and in line with NACHA’s rules.

When should a business use RTP vs ACH to reduce fraud risk?

Real-Time Payments (RTP) offer a clear advantage over ACH when reducing fraud risk is a top concern. With RTP, transactions are final, processed instantly, and available 24/7, which significantly lowers the chances of chargebacks or fraudulent reversals. On the other hand, ACH payments are batch-processed, take longer to settle, and can be reversed under specific conditions - making them more vulnerable to fraud. For situations where speed and transaction finality are essential, RTP stands out as the smarter option.