The Hidden Economics of Interchange Fees in 2026

Every time you use a credit or debit card, merchants pay a hidden cost known as interchange fees. These fees, which are set by card networks like Visa and Mastercard, are charged to the merchant's bank and passed along to the bank that issued your card. In 2026, interchange fees remain a major expense for businesses, making up 70–90% of their payment processing costs. With U.S. transaction fees hitting $198.25 billion in 2025, these charges are driving up consumer prices as merchants pass the costs along.

Key takeaways:

- Interchange fees fund fraud protection, rewards programs, and banking infrastructure but often lead to higher prices for consumers.

- On average, merchants pay 2.35% per transaction for credit cards, with premium cards costing even more.

- Regulations, like the Illinois Interchange Fee Prohibition Act, aim to limit these fees but face federal pushback.

- Debit cards offer lower fees (capped at $0.21 + 0.05%) under U.S. law, but premium credit cards can exceed 3.5%.

- AI tools, like DidIBuyIt, help merchants and consumers spot errors and recover overcharges.

Interchange fees have far-reaching effects on merchants, consumers, and the economy. Understanding these fees and exploring cost-saving strategies - like using regulated debit cards or adopting transparent pricing models - can help reduce their impact.

Credit Card Processing Fees Explained: Interchange Fees, Network Fees & Processor Markups

sbb-itb-5d40823

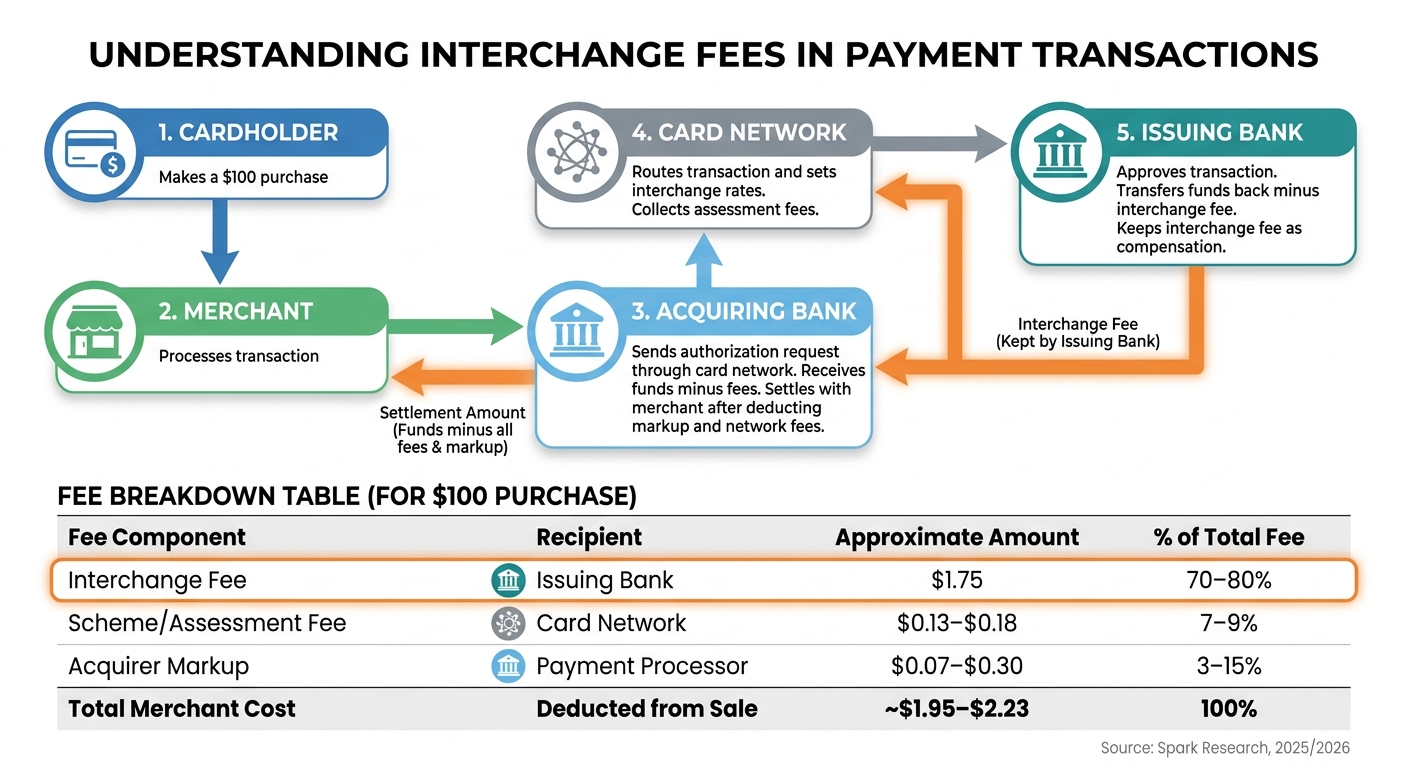

How Interchange Fees Work in Payment Transactions

How Interchange Fees Flow Through Payment Transactions

Interchange fees flow through several key players in the payment ecosystem: the cardholder, merchant, issuing bank, acquiring bank, and card network [10].

What Issuing and Acquiring Banks Do

When a customer makes a purchase, the acquiring bank (the merchant's bank) sends an authorization request through the card network to the issuing bank (the cardholder's bank). If the transaction is approved, the issuing bank transfers the funds back to the acquiring bank, deducting the interchange fee. The acquiring bank then settles the payment with the merchant after subtracting its own markup and network fees [10][11].

The issuing bank keeps the interchange fee as compensation for taking on risks like fraud and credit defaults, as well as for funding rewards programs [9][10][11]. On the other hand, the acquiring bank, which manages transaction routing and settlement, pays this fee on behalf of the merchant [10][11]. Card networks like Visa and Mastercard act as the infrastructure for these transactions, setting interchange rates and collecting separate assessment fees for their services [10][6].

"Interchange is not just revenue. It's also one of the main economic forces that shapes how card programs get built." – Ricky Graziosi [9]

Here’s a simple breakdown of how a $100 purchase might be divided:

| Fee Component | Recipient | Approximate Amount | % of Total Fee |

|---|---|---|---|

| Interchange Fee | Issuing Bank | $1.75 | 70–80% |

| Scheme/Assessment Fee | Card Network | $0.13–$0.18 | 7–9% |

| Acquirer Markup | Payment Processor | $0.07–$0.30 | 3–15% |

| Total Merchant Cost | Deducted from Sale | ~$1.95–$2.23 | 100% |

(Source: Spark Research, 2025/2026) [10]

Interchange fees can vary widely depending on the type of card used.

Credit Card vs. Debit Card Interchange Fees

The difference in fees becomes clear when comparing credit and debit card transactions. Credit card fees are notably higher, as they account for the credit risk taken on by banks and the costs of rewards programs like cashback or travel perks [13][14]. On average, Visa credit transactions carry a fee of 1.97%, while Mastercard averages 1.79% [12]. Premium rewards cards can push fees even higher, ranging from 2.5% to over 3.5% [13][15].

Debit cards are governed by different rules. Thanks to the Durbin Amendment, regulated debit cards from large banks (those with over $10 billion in assets) are capped at approximately $0.21 + 0.05% per transaction [1][15]. A Federal Reserve proposal could lower this cap further to $0.144 + 4 basis points by 2026 [1].

The way a transaction occurs also affects fees. Card-present transactions - where the card is physically swiped, inserted, or tapped - tend to have lower fees due to reduced fraud risk. In contrast, card-not-present transactions, such as online or phone orders, come with higher fees [13][15]. The merchant's industry also matters: low-risk businesses like grocery stores typically face lower fees, while higher-risk sectors like travel agencies are charged more [14][15].

These fee structures influence how costs are distributed across the payment ecosystem.

Who Actually Pays Interchange Fees

While the acquiring bank technically pays the interchange fee, merchants ultimately shoulder the cost. They often adjust their pricing, implement minimum transaction amounts, or add surcharges to offset these expenses [10][11][16]. This means that even consumers who pay with cash or debit cards indirectly subsidize the rewards programs enjoyed by credit card users [16][10].

This dynamic creates growing financial pressure on merchants, a key issue in the evolving payment landscape. Experts describe the current situation as a "double squeeze." Issuing banks face tighter profit margins due to new regulations and fee caps, while the fees paid to networks like Visa and Mastercard have risen by 30% in unit costs over the last five years [6].

"Interchange is getting the attention. Network fees are getting the revenue." – Steven Leitman, Managing Partner, Consulting Resource Group [6]

Interchange Fee Regulations in 2026

The world of interchange fees became even more complex in 2026, thanks to new federal regulations. In April of that year, the Office of the Comptroller of the Currency (OCC) stepped in to block state-level restrictions, significantly altering the policy landscape. This move came as swipe fees in 2025 had reached nearly $200 billion [19].

The OCC's April 2026 Rule Explained

On April 29, 2026, the OCC released two major actions that reshaped interchange fee rules. The first, an Interim Final Rule, reclassified interchange fees as "non-interest charges", protecting them under the National Bank Act. The second, an Interim Final Order, overruled the Illinois Interchange Fee Prohibition Act (IFPA), which sought to ban fees on taxes and tips starting July 1, 2026 [17][18]. Both measures went into effect on June 30, 2026 - just in time to prevent the Illinois law from taking hold.

The OCC justified its actions by arguing that state-specific fee restrictions would lead to conflicting standards that national banks and payment networks, such as Visa and Mastercard, couldn't effectively manage [21][22]. These regulations also safeguard banks' ability to use transaction data for fraud prevention and compliance purposes [17].

"Interchange fees are a core banking function, and state limits on those fees necessarily interfere with national bank powers, regardless of who establishes or pays the fees."

– Office of the Comptroller of the Currency [17]

While banks protect their fee revenue, consumers often struggle with transaction issues; if a merchant refuses a refund, cardholders may need to exercise their dispute rights through these same institutions.

The Illinois law would have imposed a $1,000 penalty per transaction for violations, and similar legislation had been proposed in other states [18][6]. Unsurprisingly, the OCC's intervention drew sharp criticism. Doug Kantor from the National Association of Convenience Stores remarked, "The OCC is taking advocating for big Wall Street banks to a whole new level" [20].

This federal move has broader implications, influencing international markets and shaping how merchants and consumers respond.

What Happened When Other Markets Capped Fees

Looking at other countries, fee caps have often led to unintended outcomes. In Australia, for example, restrictions on interchange fees caused annual card fees to rise by over 50% and cut rewards value per dollar spent by half. Similarly, in the U.S., a Federal Reserve Bank of Richmond study revealed that 98.8% of merchants either maintained or increased prices after the Durbin Amendment capped debit card fees [24]. Banks also suffered revenue losses of around $6.5 billion annually, leading to the elimination of free checking accounts and leaving about one million Americans without banking services [24].

In the European Union, interchange caps reduced rewards programs and increased fees for premium cards. However, merchants continued to price goods based on overall operating costs, rather than passing savings from fee reductions to consumers [23][24].

These examples demonstrate a phenomenon often referred to as the "waterbed effect" - when regulators lower costs on one side of the payment system, fees tend to rise elsewhere. For instance, card networks have offset capped interchange fees by increasing "scheme fees" - charges for infrastructure and services. Over the past five years, these network fees have risen by about 30%, effectively neutralizing the intended benefits for merchants [6].

How Consumers and Merchants Respond to Fee Regulations

Regulatory shifts have forced all players in the payment ecosystem to adapt. Banks have sought federal protection, sometimes filing lawsuits to block state-level restrictions they argue would require costly system overhauls [17][19]. For example, excluding taxes and tips from interchange calculations would demand significant technical changes.

Merchants, on the other hand, continue to push for state laws that exclude non-revenue portions of transactions from fee assessments. Under the Illinois IFPA, a $50 restaurant bill with $4.08 in tax and an $8 tip would have excluded about 24% of the transaction value from interchange fees [6]. Rob Karr of the Illinois Retail Merchants Association criticized the OCC's actions, stating that they "prioritize the bottom line of banks and credit card companies over meaningful relief for businesses and consumers" [19].

The legal landscape remains uncertain. Following the Supreme Court's Loper Bright decision, courts no longer automatically defer to agency interpretations, like those from the OCC. As a result, these rules face heightened judicial scrutiny [17]. The 7th Circuit Court of Appeals is currently reviewing the Illinois case, with a decision expected by mid-June 2026 that could set a precedent for similar state laws [19].

These developments highlight the complex ripple effects of fee regulations on consumers, merchants, and the broader economy.

What Interchange Fees Pay For and What They Cost

Interchange fees play a dual role: they fund the payment infrastructure while also introducing hidden costs that affect the economy.

How Interchange Fees Support Rewards and Security

These fees serve as compensation for the issuing banks, covering the expenses and risks tied to offering credit. This includes the interest-free period cardholders enjoy before paying off their balances [25][2]. Additionally, interchange fees finance fraud prevention systems and identity verification processes that uphold zero-liability policies [25][10]. They also fund critical payment processes like authorization, clearing, and settlement, as well as compliance with security standards such as PCI DSS, 3D Secure, and tokenization [6][10].

Beyond security, these fees are what make rewards programs - like cashback, travel points, and airline miles - possible, particularly for premium cardholders [25][8]. They also support the administrative systems that handle payment disputes and chargebacks [25]. Lastly, banks rely on these fees to guarantee settlement, ensuring merchants receive their funds even if a cardholder defaults on payment [10].

"Interchange fees aren't arbitrary, and they aren't designed to punish merchants. They're the mechanism that balances risk, rewards, and trust across the card ecosystem."

– Bernard Prevost, Payments Expert [25]

The Rewards Problem: Winners and Losers

One of the biggest criticisms of interchange fees lies in how they redistribute costs. Cash users and those with basic credit cards indirectly subsidize the rewards enjoyed by premium cardholders [26]. Since merchants typically factor interchange fees - averaging around 2.35% [2] and exceeding 2.5% for premium cards [8] - into their retail prices, everyone pays more, regardless of how they pay.

As Plasma explains:

"The 'rewards paradox' creates a hidden wealth transfer, as merchants often raise retail prices for all customers to cover the costs of the rewards earned by premium credit card users."

– Plasma [26]

This system creates an economic imbalance. Paying cash for groceries or other essentials could mean you're helping fund someone else's airline miles or cashback perks. This dynamic disproportionately benefits high-income consumers who qualify for premium cards, while low-income consumers and those who rely on cash bear the brunt of higher prices. Merchants, in turn, are forced to adjust their pricing strategies to account for these costs.

How Merchants Manage Interchange Costs

For most merchants, interchange fees are treated as a standard cost of doing business, typically spread across all customers. These fees make up 70% to 90% of total payment processing expenses [2]. Businesses with slim profit margins - like grocery stores (1–2%) and restaurants (3–5%) - are particularly affected. To cope, they often raise prices or add surcharges to cover these costs. On the other hand, businesses with higher profit margins (above 40%) are better positioned to absorb these fees, allowing them to maintain a smoother checkout experience.

These cost pressures highlight the need for creative solutions, including AI-driven tools for dispute resolution, which will be explored in the next section.

AI Tools for Managing Interchange-Related Costs

Interchange fees are a growing challenge for both consumers and merchants, but AI-powered platforms are stepping in to help. These tools focus on spotting overcharges, simplifying disputes, and recovering lost funds. A standout in this space is DidIBuyIt, which uses AI to transform interchange fee headaches into manageable issues. While these platforms can’t eliminate fees, they make it much easier to address errors and recover unnecessary charges.

Finding and Fixing Wrong Charges

AI tools excel at combing through transaction histories to uncover billing mistakes that often slip by unnoticed. For instance, DidIBuyIt has a database of over 50,000 transaction descriptors, making it easier for users to identify those puzzling charges on their statements [28]. The platform’s AI can detect issues like duplicate charges, unauthorized fees, or incorrect amounts - problems that frequently arise from interchange fee processing.

For merchants, the stakes are even higher. DidIBuyIt’s reconciliation tool recalculates interchange fees using official rate tables from Visa and Mastercard [30]. If it finds discrepancies, such as tier misclassification or incorrect cross-border flags, it flags an "overcharge variance" for correction. Even minor errors can add up to substantial losses. Beyond detection, the platform simplifies the dispute process, helping merchants recover funds more efficiently.

Making Dispute Resolution and Chargebacks Easier

Disputing charges used to mean hours of digging through records and endless paperwork. AI has changed that. In May 2026, DidIBuyIt users recovered $3.2 million, thanks to its automated approach to dispute resolution [29].

The AI selects the correct network reason code for each transaction - a crucial step, as 60% to 80% of chargebacks fail due to incorrect codes or missing evidence [31]. It also generates dispute documents complete with evidence checklists and follow-up scripts [29]. Take Sarah M., for example. After a canceled Adobe subscription kept charging her, she used DidIBuyIt to recover $599. The platform identified her email timestamp as key evidence, and her bank reversed the charge in just six days [29][31].

Given the strict 120-day dispute window across all networks [29], speed is critical. DidIBuyIt integrates with major payment networks, ensuring users can act quickly no matter their payment method.

Working with Visa, Mastercard, Amex, and PayPal

The best AI platforms work seamlessly across various payment networks. DidIBuyIt supports Visa, Mastercard, Amex, Discover, PayPal, Apple Pay, and Google Pay [29], offering users a unified platform for managing disputes across different payment methods. This is vital because each network has its own rules, deadlines, and evidence requirements.

The platform also provides real-time data analysis across all payment providers, helping merchants pinpoint which network offers the lowest fees or highest success rates for specific transactions. For disputes, DidIBuyIt unifies workflows, enabling merchants to handle the entire process - from intake to resolution - within a single system. Additionally, tools like Visa’s Order Insight, which shares transaction details with banks to prevent "friendly fraud", can resolve potential disputes before they escalate into chargebacks [30].

"The true cost of payments is acceptance cost per successful order after two invisible drags: fee overcharges that creep into blended pricing, and chargeback fallout." – Amrit Mohanty of Optimus [30]

How to Reduce Your Interchange Fee Burden

Interchange fees can take a big bite out of profits for merchants and raise costs for consumers. However, there are steps you can take to ease the strain. By fine-tuning fee structures, payment methods, and transaction practices, businesses can save more than they might realize.

Picking the Best Payment Methods

Not all cards are created equal when it comes to processing fees. For instance, regulated debit cards have some of the lowest rates - just 0.05% + $0.21. On the other hand, premium rewards cards, like Visa Signature, can cost as much as 2.30% + $0.10 for online transactions [8]. For merchants, encouraging customers to use debit cards can lead to noticeable savings. Even something as simple as asking, "Debit or credit?" at checkout can make a difference. Offering small perks, like a $0.50 discount for debit use, can also steer customers toward the lower-cost option [27][34].

From a consumer's perspective, rewards cards may seem appealing because of their perks, but they come with higher fees for merchants. These costs often get passed on to all customers through higher prices. If you see businesses offering different prices for cash and card payments, opting to pay cash can save you money and help the merchant avoid processing fees [8][34].

Once your payment methods are optimized, it's time to look at how transactions are processed.

Tracking and Improving Your Transactions

One easy way for merchants to cut interchange fees is by settling transactions daily. Delaying batch settlements can push transactions into higher-cost categories, known as "downgrades" [27][34]. Automating 24-hour batching is a simple fix that prevents this issue.

Additionally, using fraud prevention tools like Address Verification Service (AVS) and Card Verification Value (CVV) for online or keyed-in transactions not only reduces fraud risk but can also qualify you for lower interchange rates [27].

For B2B businesses, providing enhanced transaction data - like Level 2 or Level 3 details - can bring down interchange fees by as much as 0.3% to 1% [34]. For example, the Star Tribune in Minneapolis saved 60% on 4.6% of their transactions by including details like invoice numbers and tax amounts in their processing [33]. If your business works with other businesses or government entities, this is worth exploring.

Once your processing is streamlined, the next step is understanding and managing your fees.

Reading Your Processing Statements

Many merchants overlook their processing statements, missing opportunities to save. Start by calculating your effective rate: divide your total monthly fees by your total card volume [27]. This gives you a quick snapshot of whether your fees are competitive.

Next, check your pricing model. Interchange-Plus pricing is often more transparent, separating the interchange cost from the processor's markup. If you're on a Tiered or Flat Rate model, there's a good chance you're overpaying.

"I have looked at thousands of merchant statements. The pattern is always the same: businesses on interchange plus pay less. Period." – Grant Denmark, Founder, Sleft Payments [8]

For example, a business processing $50,000 monthly could save around $6,180 annually by switching from a 2.6% flat rate to Interchange-Plus pricing [8]. You can also request a downgrade report from your processor to pinpoint transactions that are being pushed into higher-cost tiers [27].

Finally, focus on negotiating the processor's markup - the "plus" part of Interchange-Plus pricing. The table below outlines competitive benchmarks for 2026:

| Monthly Volume | Competitive Markup | Overpriced |

|---|---|---|

| Under $10,000 | 0.25% + $0.10 | 0.75%+ |

| $10,000 - $25,000 | 0.20% + $0.10 | 0.60%+ |

| $25,000 - $50,000 | 0.15% + $0.08 | 0.50%+ |

| Over $100,000 | 0.05% + $0.05 | 0.30%+ |

Be vigilant about fees that seem vague or unnecessary. Charges like PCI non-compliance fees, "regulatory" fees, or terminal insurance fees are often just extra profit for processors. If a fee can't be clearly explained, push back [27]. Every adjustment you make can directly boost your bottom line.

What's Next for Interchange Fees

Interchange fees are undergoing significant changes. Card networks are shifting from fixed-rate structures to dynamic pricing models that adjust in real time based on factors like transaction data quality, security measures, and fraud risk. At the same time, regulators in the U.S. and other regions are introducing new rules and caps, forcing merchants and issuers to adapt. Let’s dive into how real-time authentication is shaping these changes.

New Pricing Models Based on Authentication

Interchange fees are no longer a one-size-fits-all deal. Networks such as Visa and Mastercard are moving toward pricing models influenced by authentication and security. For example, Visa’s Digital Commerce Authentication Program (DCAP) introduces fees of 0.015% for domestic transactions and 0.035% for cross-border ones, starting April 18, 2026 [5].

Visa’s Commercial Enhanced Data Program (CEDP), launched in January 2026, takes this concept further by validating transaction data in real time. Transactions with verified invoice details can enjoy reduced fees - 15 basis points lower than traditional Level 3 rates. On the flip side, unverified data could lead to fees increasing by as much as 75 basis points [35]. Dean M. Leavitt, Founder and CEO of Boost Payment Solutions, summed it up well:

"This is all about validating the data and making sure that it's accurate and real so that the supplier can enjoy the lower interchange rate" [35].

For merchants, this means clean and accurate data isn’t just a technical detail - it’s a way to control costs. Those who fail to update their systems to handle real-time validation could face rising fees over time [35]. These changes are reshaping merchant expenses and, by extension, consumer prices, making it vital for businesses to stay ahead.

How Different Regions Handle Interchange Fees

The approach to interchange fees varies widely across regions. Since 2015, the European Union has capped fees at predictable rates - 0.20% for debit and 0.30% for credit [1]. While this stability has been a relief for merchants, debates continue over whether these caps stifle innovation and rewards programs.

In the United Kingdom, post-Brexit cross-border transactions between the UK and the European Economic Area now incur higher rates - 1.15% for debit and 1.50% for credit - with regulators currently reviewing these increases [1]. Meanwhile, Canada has implemented a small-business relief program, lowering average credit interchange fees to about 0.95% for eligible merchants [1].

The U.S. is also weighing changes to its debit fee structure. Proposed updates to Regulation II could reduce the maximum regulated debit fee from $0.21 + 5 basis points to $0.144 + 4 basis points, along with a $0.013 fraud adjustment [1]. If approved, this would ease the cost burden on merchants. However, international businesses face added complexity - while a transaction might cost 0.30% in the EU, it could climb to 2.35% in the U.S. [36].

Finding the Right Balance Between Rules and Competition

Policymakers face the challenge of balancing regulation with market forces. In the U.S., a $200 billion settlement involving Visa, Mastercard, and merchants is awaiting final approval as of April 2026. If approved, it would reduce average credit interchange fees by 10 basis points over five years and cap standard consumer card rates at 1.25% for eight years [36][3]. The settlement also proposes changes to the "honor-all-cards" rule, potentially allowing merchants to decline high-fee premium cards like Visa Infinite or Chase Sapphire Reserve while still accepting standard cards from the same network [36].

However, some argue that regulation alone won’t solve the problem. Eric Cohen, Founder and CEO of Merchant Advocate, emphasizes the need for clarity:

"Businesses are not asking for zero interchange. They are asking for predictability, clarity and consistency" [7].

He also points out:

"The 'interchange wars' are not really about winning or losing a lawsuit. They are about whether the payments ecosystem can evolve into one that businesses can understand, anticipate and rely on" [7].

Meanwhile, industry players are finding creative ways to work around existing rules. For instance, after the Capital One-Discover merger in 2025, Capital One began routing debit transactions through the Discover network to bypass Durbin Amendment caps. As a result, interchange rates on these cards have soared to 1.10% + $0.16 for card-present transactions - more than 20 times the regulated rate [5]. This shows how networks can use strategic routing to sidestep regulatory limits.

As these shifts continue - driven by new regulations, legal battles, and network innovations - businesses must stay informed and be ready to adjust their strategies.

Conclusion: What You Need to Know About Interchange Fees in 2026

Interchange fees make up a hefty 70% to 90% of merchant payment processing expenses [3][4]. With U.S. transaction fees projected to hit a staggering $198.25 billion in 2025 [6], understanding these fees is crucial for maintaining profitability and managing personal finances effectively.

The structure of interchange fees continues to shift. For instance, Visa raised Level 2 interchange rates for small business credit cards by 75 basis points on January 24, 2026 [3]. Additionally, network fees have risen by about 30% in recent years [6]. According to Eric Cohen, businesses are looking for fee structures that are easier to predict [7]. To achieve this, companies can adopt interchange-plus pricing, ensure they submit complete Level 3 transaction data, and settle batches within 24 hours to avoid costly downgrades [27][3].

Dispute management is another critical area. Visa alone handled over 106 million disputes globally in 2025 [32]. Advanced tools, like AI-powered platforms, are now available to identify overcharges, create compliant documentation, and efficiently resolve disputes. These tools are becoming essential for navigating the increasingly complex fee landscape. For both consumers and merchants facing incorrect charges across Visa, Mastercard, Amex, or PayPal, services like DidIBuyIt offer encrypted dispute analysis and 24/7 support to help recover funds quickly and securely.

These advancements build on earlier strategies for optimizing payment methods and streamlining transaction processes. With new fee regulations and authentication models shaping the market, staying ahead of rising costs requires proactive management. Regularly auditing statements, using lower-cost options like regulated debit cards, and leveraging automation to uncover hidden fees are all smart practices. In 2026’s ever-evolving payment ecosystem, these steps are essential for keeping costs under control.

FAQs

Why are interchange fees so hard for merchants to predict?

Interchange fees can be tricky to pin down since they're determined by card networks like Visa and Mastercard. These fees hinge on several factors, such as the type of card used, how the transaction is processed, and the level of risk involved. To make matters more complex, they fluctuate often due to shifts in technology, changes in consumer habits, fraud patterns, and regulatory updates. For merchants, the challenge is even greater because they have no direct influence over these fees, making them a moving target in the constantly changing world of payments.

Do lower interchange caps actually reduce prices for shoppers?

Lower interchange caps set for 2026 are anticipated to decrease the costs associated with card transactions. This change could result in lower fees for merchants, which might, in turn, lead to reduced prices for consumers. However, whether shoppers actually see these savings will depend on whether merchants decide to pass along the cost reductions.

How can I spot and recover interchange-related overcharges?

To spot and recover interchange-related overcharges, start by carefully reviewing your processing statements. Look at the detailed interchange fees and compare them to the standard rates set by card networks. Using interchange-plus pricing can make costs more transparent, helping you see exactly what you're paying.

Be on the lookout for transaction data errors or downgrades, as these can lead to higher fees. If you notice any issues, work with your payment processor to correct them. Additionally, incorporating AI tools and performing regular audits can help identify overcharges and fine-tune your fee structure for better cost management.